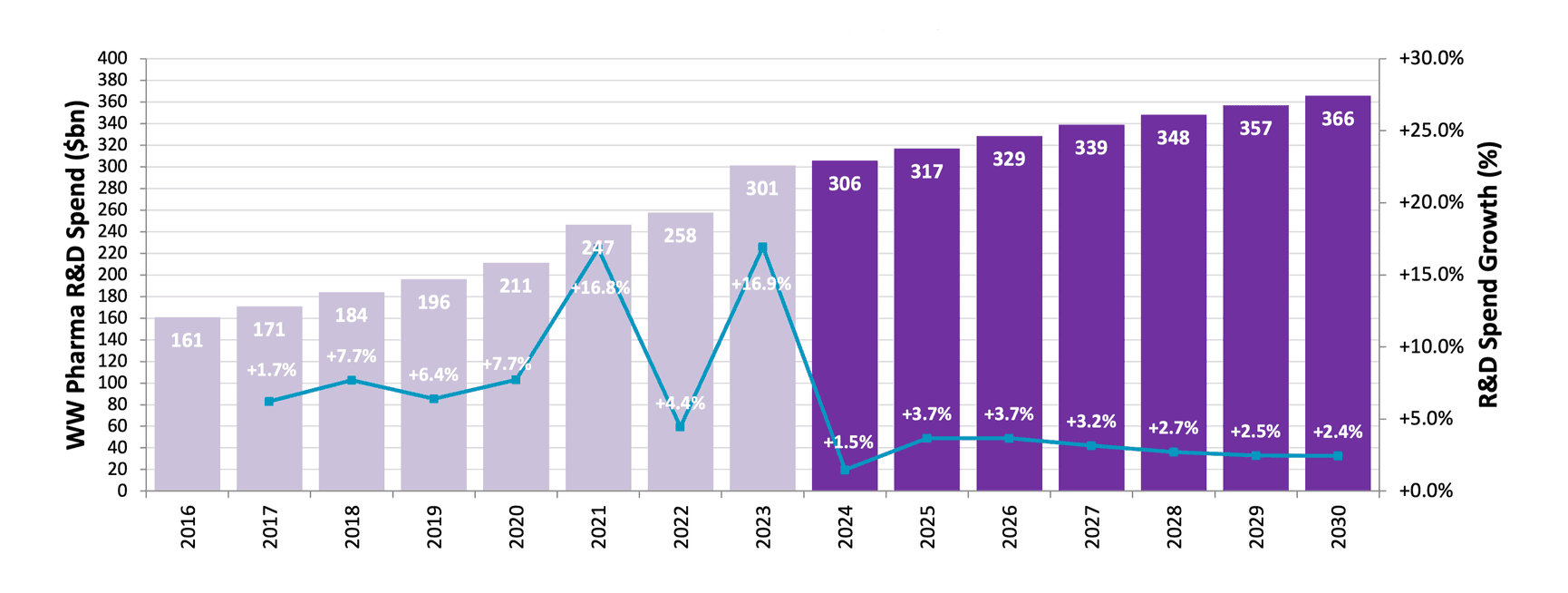

Pharma R&D Spend Grows More Slowly

Risk-averse pharma displays cautious R&D spending amid continued regulatory and geopolitical uncertainty.

Source: Evaluate Pharma© (May 2024)

Risk-averse pharma displays cautious R&D spending amid continued regulatory and geopolitical uncertainty

Pharma R&D spend is forecast to grow significantly more slowly in the second half of the decade than it did in the first: CAGR of over 9% in 2016-2023 shrinks to below 3% between 2023-2030. Combined R&D spend of over $300 billion in 2024 (27% of sales) falls to 21% of sales in 2030.

Why? Various factors may be in play. Many pharma are streamlining pipelines and operations as commercial pressures continue to build. M&A may be playing a relatively greater role given some pharmas’ need to replace genericising blockbusters. AI promises to boost R&D and operational efficiency, though it’s too early to quantify to what extent. Forecasts of the technology’s impact may be somewhat optimistic.

Geopolitical tensions also add uncertainty to spending plans. The US Biosecure Act seeks to bar biopharma firms from contracting with Chinese players such as Wuxi AppTec and Wuxi Biologics, key CDMO partners. The act hasn’t yet made it into law, but industry association BIO recently U-turned to join the government in backing it and experts predict that it will eventually pass.

Continued macroeconomic malaise adds to a more general “risk-off” attitude among investors, helping explain the lacklustre performance so far this year of the XBI, a basket of US-listed biotech stocks.

Inflation Reduction Act Beds In

Then there’s the Inflation Reduction Act. Pharma C-suites are less vocal about it these days, even though aspects of the Act – including the unequal treatment of small molecules and biologics – remain controversial. Battles could re-ignite as the IRA provisions roll out, and forecasts may change as the true shape of the law is revealed. It is difficult to gauge whether – or how much – IRA is influencing pharma’s choice of modality and/or indication.

Price negotiations are underway for products including clot-busters Eliquis (BMS) and Xarelto (JNJ) and diabetes meds Jardiance (Lilly/Boehringer Ingelheim) and Januvia (Merck). They will come into effect in January 2026. At the start of 2025, Medicare will select up to 15 more drugs for negotiations.

Novo’s semaglutide – the active ingredient in Ozempic and Wegovy – is expected to fall into IRA’s crosshairs by the end of the decade; it was first launched in 2017. Ozempic and Wegovy sales will be combined to determine when the Medicare cost threshold is reached. Novo is banking on Cagrisema to have by then been approved as an even more effective alternative.

Medicare doesn’t, by law, cover drugs for obesity. But the picture may change if these treatments continue to show benefits across related conditions including cardiovascular and kidney disease, of liver fibrosis (Lilly recently reported promising Phase 2 results for tirzepatide in metabolic dysfunction-associated steatohepatitis (MASH)). Wider approvals could turn GLP-1 drugs into one of the most impactful health interventions since the statins. But they will also squeeze already limited health budgets, leaving less room for the flurry of newer modalities in other areas – including much rarer diseases. (See Orphan Drugs report).

US Elections May Influence Pharma FortunesA Trump win in the US presidential elections in November 2024 may boost stock markets and, with it, the biotech sector, according to Tim Opler, managing director at investment bank Stifel. It could also take some of the sting out of IRA’s implementation. But drug pricing pressure will remain whoever is in the White House. Flourishing biopharma innovation plus ageing populations make that almost certain.

IRA price curbs are unlikely to radically change obesity company rankings or sales forecasts for now, since most sales are in the private market.