More M&A as Public Markets Remain Flat

Deals provide a lifeline to cash-strapped biotechs and provide Big Pharma with a route to address loss of exclusivity.

Deals provide a lifeline to cash-strapped biotechs and provide Big Pharma with a route to address loss of exclusivity

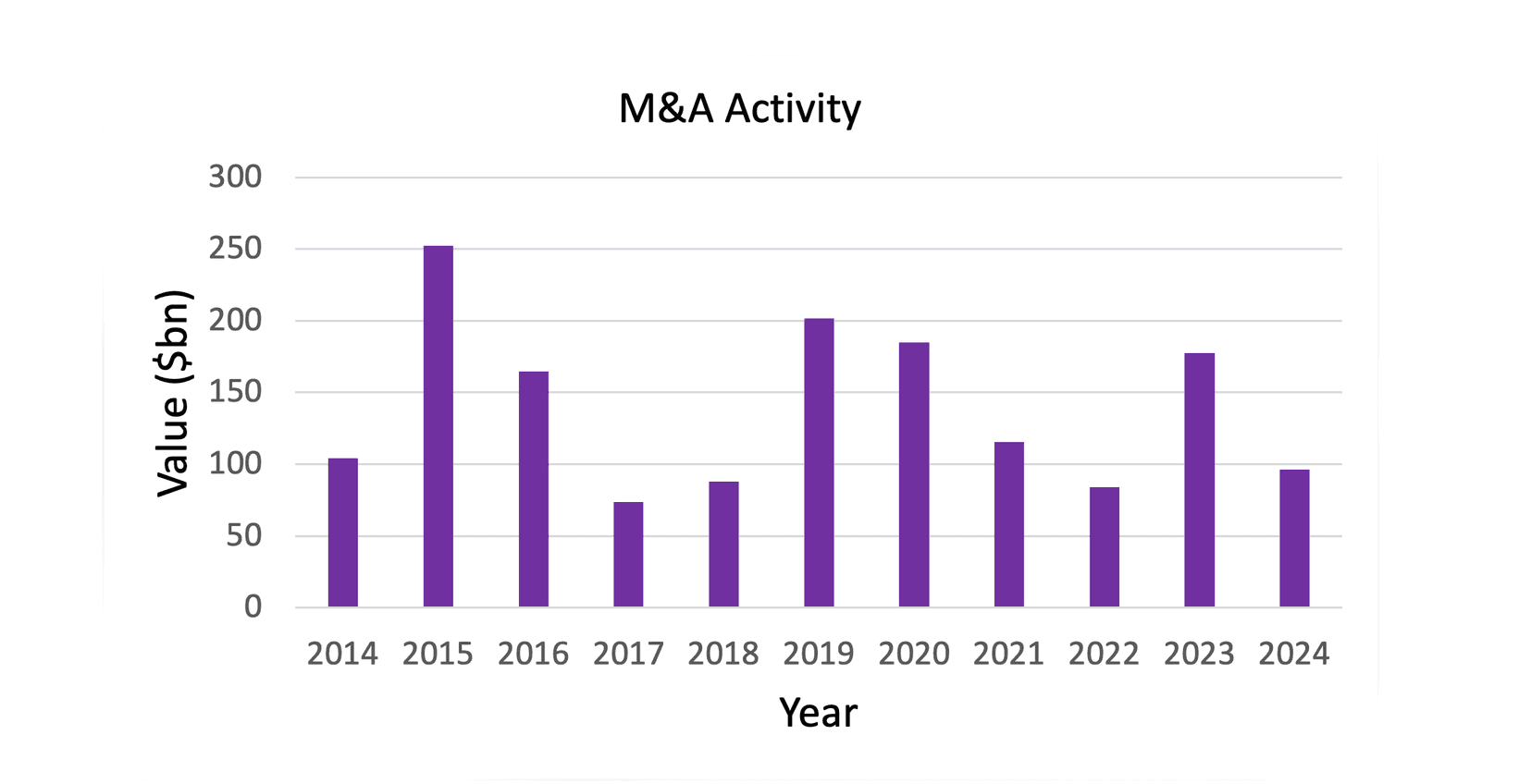

“The first half of 2024 saw close to $100 billion worth of Big Pharma M&A, putting this year on track to surpass 2023 – itself one of the top-three strongest M&A years in two decades. The biggest product-focused deals so far this year? Bristol’s CNS-focused Karuna buy, and AbbVie’s acquisition of ADC company Immunogen, both with on- or close to- market products. (Figures below include Novo Nordisk’s proposed $16.5 billion deal for CDMO Catalent, which remains under FTC review.)

More M&A is likely as patents expire, obesity/diabetes drug revenues pile up and as innovation continues to flourish: cutting edge science emerges more often from academia or biotech than from Big Pharma. Smaller, bolt-on acquisitions - like Merck’s acquisitions of Harpoon or Abceutics, or Novartis’ purchase of auto-immune focused Calypso in early 2024 - are increasingly popular as they’re easier to integrate and less likely to fall foul of a still-hawkish Federal Trade Commission.

Deals of any size have become a lifeline for biotechs, struggling in a longer-than-usual down-cycle during which public markets have remained stubbornly shut.

This year has seen fewer than a dozen biotech IPOs, with many trading below their list price. CNS-focused Rapport Therapeutics, which went public in June, is a notable exception. Many other companies have filed IPO documentation, but the outlook is uncertain – Australian radiopharmaceutical company Telix withdrew a planned Nasdaq listing in mid-June.

M&A is really the only reliable exit option for investors and has turned Big Pharma into a very important friend to biotech and its backers. Venture capitalists are eking out support for portfolio companies that pharma hasn’t bought, but the money’s running short. Raising new funds is much tougher, too, since many of VCs’ own limited partner investors have seen paltry returns.