Pipeline Captures CNS Revival

Obesity entries dominate 2030’s most valuable pipeline products, though oncology will remain the biggest category.

Obesity entries dominate 2030’s most valuable pipeline products, though oncology will remain the biggest category

The top ten most valuable pipeline candidates by net present value are projected to collect almost $65 billion in 2030 sales. Three of the top four address obesity and its sequellae – Novo’s chart-topping CagriSema, which combines Wegovy’s active ingredient with an amylin analogue, and Lilly’s oral GLP-1 hopeful orforglipron and “triple-G” drug retatrutide, which hits GLP-1, GIP and the glucagon receptor (GCGR).

Three CNS drugs also feature in the top ten, reflecting significant scientific progress and investor interest in this large under-served category. Bristol Myers Squibb’s schizophrenia therapy KarXT, acquired via its $14 billion acquisition of Karuna in December 2023, combines muscarinic M1/M4 receptor agonist xanomeline with antagonist trospium to create a more tolerable – thus effective – therapy. These aren’t new mechanisms, but their intelligent combination lowers risk in a notoriously difficult area. The drug was filed in November 2023 for schizophrenia and Alzheimer’s related psychosis and has a September 2024 PDUFA; if approved it would provide a novel therapeutic mechanism for almost three million people in US with schizophrenia.

Lilly’s donanemab, an anti-amyloid-beta antibody, could bring similar relief to some patients with early-stage Alzheimer’s and their families. An FDA advisory committee in June 2024 voted strongly in favour of approval, which will likely follow before year-end. It hasn’t been an entirely smooth ride for the drug: it was rejected in January 2023 for accelerated approval, following the controversial expedited approval in 2021 of Biogen’s Aduhelm which has since discontinued. Peak sales for donanemab are expected to reach just over $5 billion, tempered by safety concerns, diagnostic challenges, and questions over which patients are most likely to benefit. Biogen/Eisai’s front-runner Leqembi (lecanemab) sold less than $20 million in the first quarter of 2024.

Vertex’s VX-548, a selective sodium channel inhibitor for moderate-to-acute pain, reported positive Phase 3 results in January 2024, setting up an anticipated mid-year filing for what could become the first new, non-opioid drug class for acute pain in over twenty years. Evaluate forecasts nearly $3 billion in 2030 sales, which may not be the peak.

Another Vertex drug, VX-121 or the “vanza triple” for cystic fibrosis, was filed in early May with a priority review voucher that could unlock approval within six months. The once daily treatment combines cystic fibrosis transmembrane conductance regulator (CFTR) protein corrector vanzacaftor, similar-acting tezacaftor (already marketed) and CFTR potentiator deutivacaftor, which is a tweaked version of another marketed drug, ivacaftor (Kalydeco). Vertex will owe lower royalties on this combination than it does on existing twice-daily Trikafta, which explains the rush to market. With over $7.5 billion in forecast 2030 sales, the “vanza triple” also tops Evaluate’s list of most valuable pipeline orphan drugs. (See Orphan Drug report)

Cagrisema

Novo Nordisk

Endocrine/GI

20.2

80.0

Orforglipron

Eli Lilly

8.3

34.0

Retatrutide

5.0

32.3

VX-121 (Vanza Triple)

Vertex

Respiratory

7.7

30.4

MK-3475 SC

Merck & Co

Oncology

8.0

19.7

Datopotamab Deruxtecan

Daiichi Sankyo

4.4

17.5

MariTide

Amgen

2.1

12.4

VX-548

CNS

2.9

11.0

KarXT

BMS

3.1

10.5

Donanemab

2.5

9.0

Top 10

64

256.8

Total

343

957.1

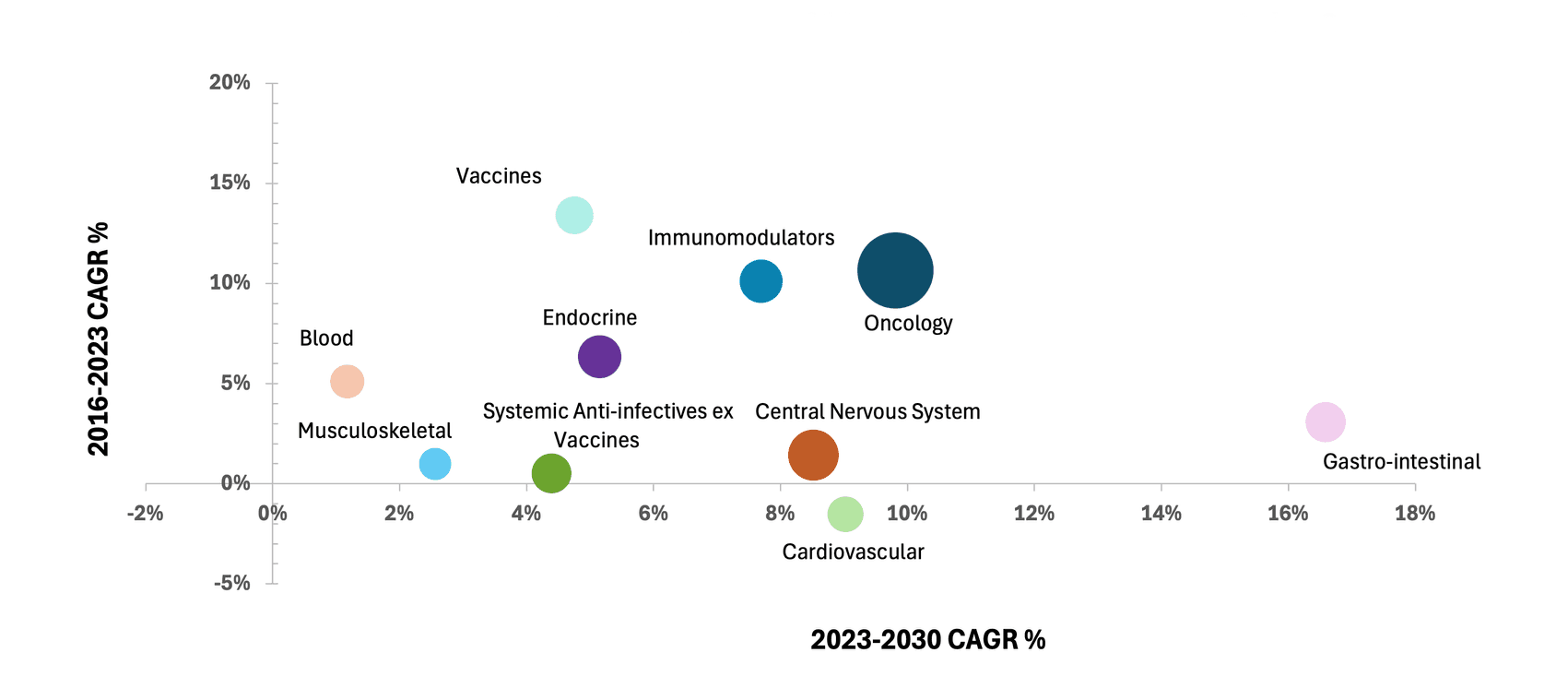

For all the buzz around obesity, oncology will remain the most valuable therapy area in 2030, with over $370 billion in forecast sales across all products. That is more than twice the totals for endocrinology (obesity & diabetes), immunology and resurgent CNS.

Oncology’s 9.8% forecast average annual growth to 2030 has slowed slightly relative to its 2016-2023 CAGR. But it still beats most other categories and is well above total prescription drug sales growth of 7.35%.

Johnson & Johnson will top the company league in oncology by 2030, thanks to Darzalex, followed by AstraZeneca, Merck and Roche.

[excludes Gardasil, a vaccine for HPV infection]

Company

2030 WW Sales ($bn)

Johnson & Johnson

36.8

AstraZeneca

29.5

25.1

Roche

23.9

17.8

Note: Circle size represents 2030 WW sales ($bn). Obesity drugs classified as GI, diabetes drugs as endocrine.

Merck’s subcutaneous version of Keytruda will be one of just two cancer drugs to make the top ten (though its peak sales of just under $13 billion are half those of original Keytruda). Cancer’s relatively poor showing on this list underscores the challenge of finding genuinely new Keytruda-sized therapies: pan-cancer targets are rare, and precision medicines chase ever-narrower mutations.

Source: Evaluate Omnium® (May 2024)

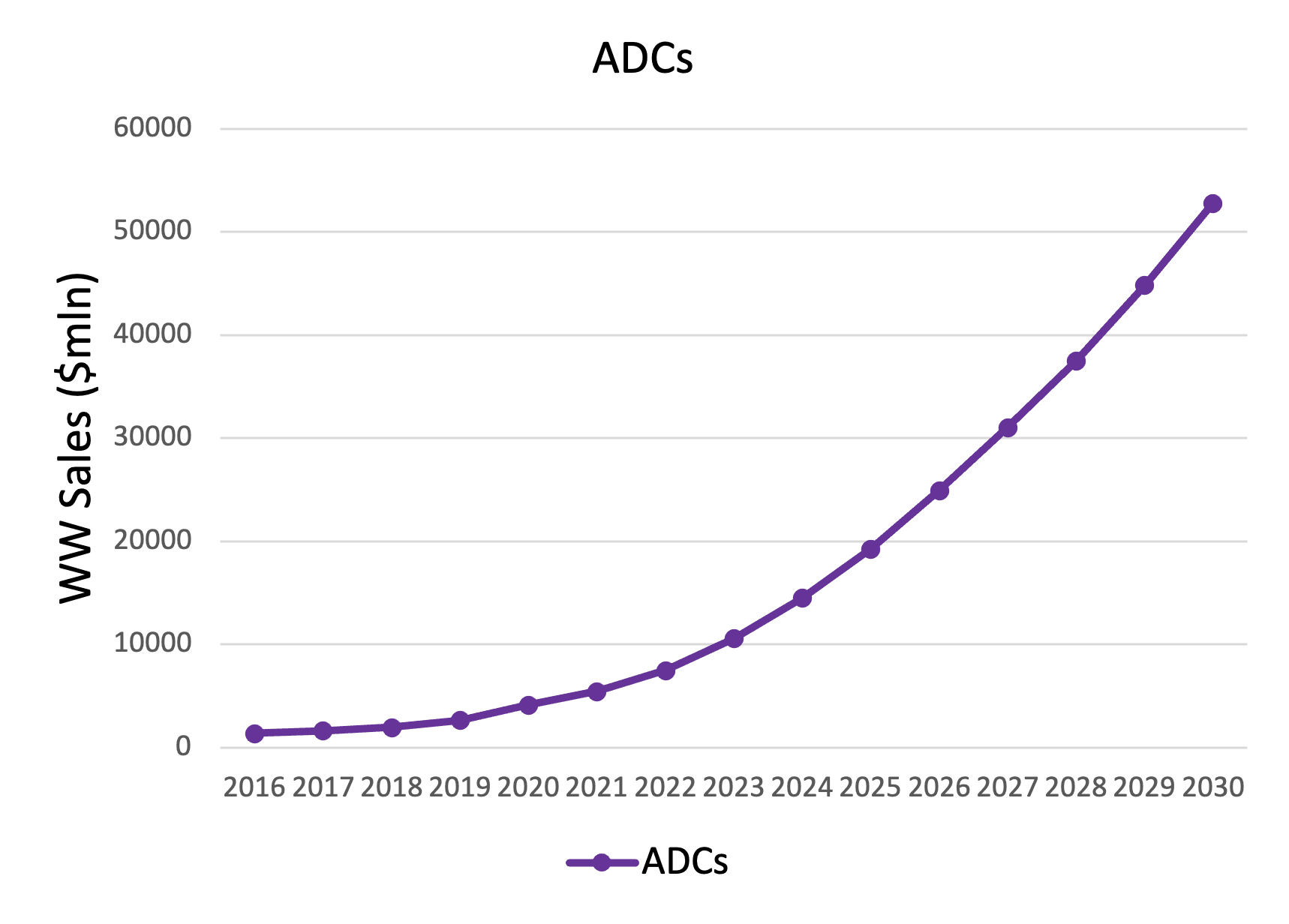

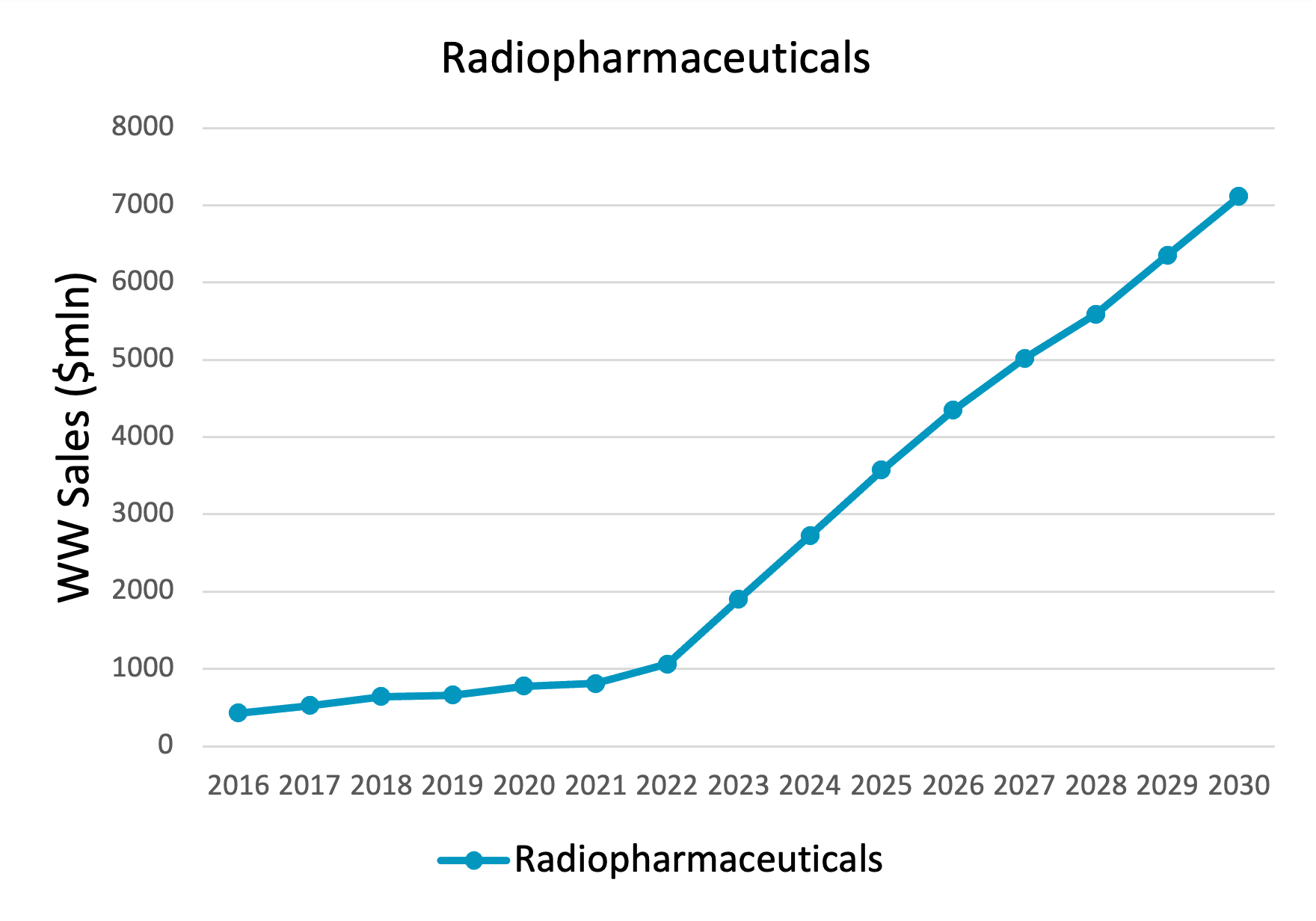

Still, newer modalities like antibody-drug-conjugates (ADCs), bi- or multi-specific antibodies, radiopharmaceuticals and oligonucleotide-based drugs are opening up more targets and targeting mechanisms, offering pipeline-in-a-product opportunities of their own.

The second top ten most valuable cancer pipeline asset is AstraZeneca/Daiichi Sankyo’s ADC datopotamab deruxetecan, under FDA and EU review for lung and breast cancer. This, and the partners’ marketed ADC Enhertu, push AZ to number two and the Japanese group up to number five in the oncology company rankings by 2030, a significant jump from Daiichi’s 2023 ranking outside the top ten. Datopotamab deruxetecan uses an antibody to direct cytotoxic topoisomerase inhibitors to TROP2, highly expressed across several cancers including non-squamous non-small cell lung cancers and hormone receptor positive HER2 negative breast cancer. Top-line overall survival results from a recent Phase 3 trial fell short of statistical significance, but data had already shown a significant improvement in progression-free-survival (PFS). The ADC is also being tested in triple negative breast cancer.

With a dozen ADCs already marketed, this red-hot class has attracted tens of billions worth of deals in the last two years, including Pfizer’s $43 billion acquisition of Seagen and AbbVie’s $10.1 billion Immunogen buy in 2023. ADCs can deliver toxic therapies in a highly targeted fashion offering opportunities to combine existing or new cytotoxics with different antibodies. (See Evaluating ADCs report)

Radiopharmaceuticals conjugate toxic radioactive isotopes to targeting ligands, offering similar innovation potential to ADCs and also attracting growing buyer interest and investment. BMS’ $4.1 billion acquisition of RayzeBio is the biggest recent deal, but Eli Lilly, AstraZeneca and Novartis have also each spent over $1 billion on radiopharma acquisitions within the last six months, respectively buying POINT Biopharma, Fusion and Mariana Oncology. Sales forecasts show a similar upward trajectory to ADCs, albeit at a lower order of magnitude – this is a less mature field.

The rapid growth of non-conventional modalities like radiopharmaceuticals, multi-specific antibodies or cell and gene therapies helps explain why worldwide shares of biotechnology versus small molecule/ conventional drug sales continue to converge toward 50/50.

Source: Evaluate Pharma© (May 2024)