Big Drugs for Big Diseases

Obesity & inflammation are driving high growth and give us a reinvigorated top 10 – but there is still that patent cliff to contend with.

Obesity, inflammation drive higher pharma sales growth

Source: Evaluate Pharma© (May 2024)

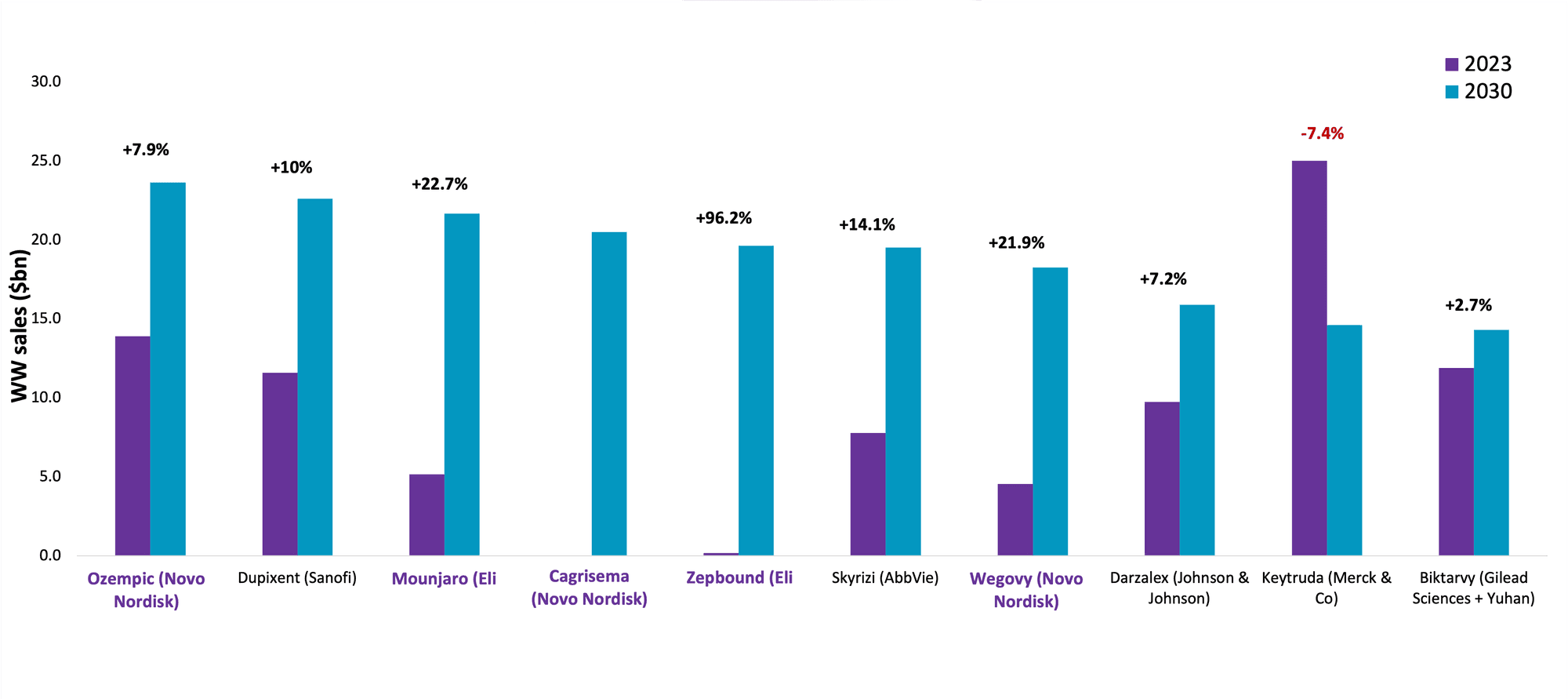

Novo Nordisk and Eli Lilly’s respective obesity/diabetes duos, Wegovy/Ozempic and Mounjaro/Zepbound, plus inflammatory disease blockbusters Dupixent - from Sanofi - and AbbVie’s Skyrizi, will help drive annual worldwide prescription drug sales growth to almost 7.7% over the next five years. That’s two percentage points over 2023’s forecasts, and significantly outpaces five-year CAGR since 2000. (See World Preview 2023). In 2030, total pharma sales will top $1.7 trillion.

Five metabolic diseases drugs will by then scoop in over $100 billion combined, dominating the top ten drug ranking. Those are Novo’s Ozempic (semaglutide) and Lilly’s Mounjaro (tirzepatide) in diabetes, analogs Wegovy and Zepbound for obesity, plus Novo’s follow-on combination Cagrisema (semaglutide and cagrilintide). More than one billion people worldwide – including 50% of all US adults – are classified as obese. These treatments not only help reduce weight but are also shown to cut the risk of related conditions including heart, liver and kidney disease. So $100 billion may not be the ceiling.

Note: Cagrisema is not yet approved

Other “big drugs for big diseases” feature prominently in 2030’s top ten. This marks pharma’s shift away from drugs for rare diseases and cancer in favour of products that can more quickly fill post-patent-expiry gaps, of which there are more to come.

Ozempic pushes Sanofi/Regeneron’s Dupixent (dupilumab) into second, but the pipeline-in-product will still sell over $22 billion in 2030 as it collects approvals beyond asthma, eczema and most recently, eosinophilic esophagitis. The drug’s average annual growth of almost 10% banks an anticipated approval in chronic obstructive pulmonary disease: recent Phase 3 data showed the IL-4/IL-13 inhibitor significantly reduces exacerbations and improves lung function in some COPD patients.

Sixth-placed Skyrizi (risankizumab) will grow by over 14% annually on average over the period to reach $19.5 billion in sales for sponsor AbbVie by 2030. The IL-23 antibody, already approved for plaque psoriasis, psoriatic arthritis and Crohn’s disease, is chasing a further win in ulcerative colitis, an inflammatory bowel disease. With sales of once-giant Humira falling steeply as biosimilars deepen their hold, AbbVie is leaning heavily on Skyrizi and JAK inhibitor Rinvoq (upadacitinib), together expected to account for over 40% of AbbVie’s 2030 revenue.

Replicating the outsized success of pipelines-in-a-product like Dupixent and Skyrizi will be tough, due to competition and disease segmentation. Auto-immune diseases including psoriasis are increasingly crowded, commanding high promotional spend. Developers now seek differentiation through biomarker-led patient stratification, slicing the market into smaller parts.

Johnson & Johnson’s Darzalex (daratumumab) is the largest of the two oncology top-ten candidates, just ahead of Merck’s genericising checkpoint inhibitor Keytruda (pembrolizumab). Keytruda’s key patent expires in 2028, like that of Bristol Myers Squibb’s Opdivo, which has fallen out of the 2030 top ten as a result. J&J’s anti-CD38 antibody is anticipated to sell close to $16 billion across its over half-dozen approvals for multiple myeloma (as part of several treatment combinations and for different disease stages). It only just outsizes Keytruda, whose annual sales will by then have shrunk by over 40% to $14.6 billion.

Skyrizi and Rinvoq are expected to account for nearly 50% of AbbVie’s 2030 revenues.

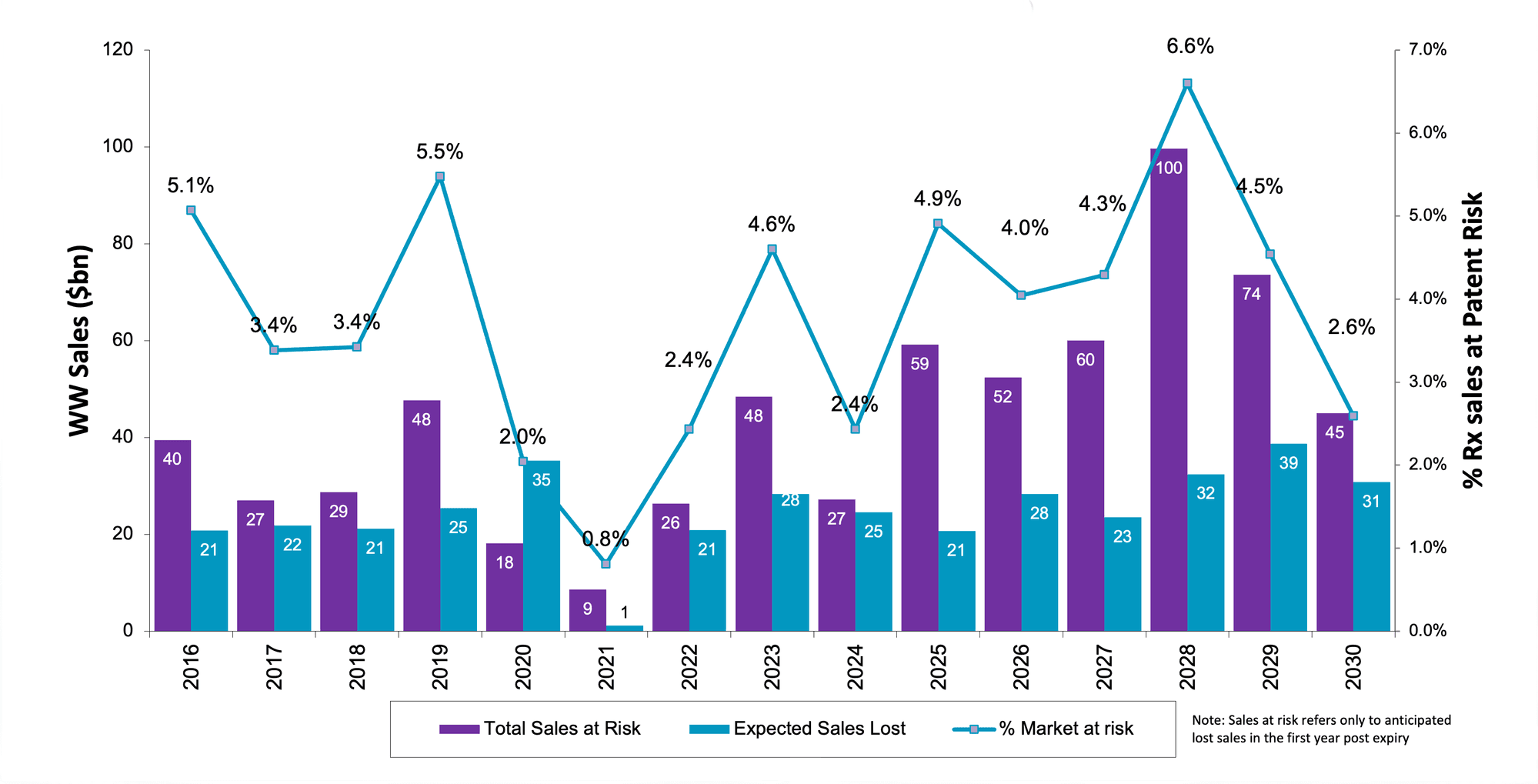

Pharma’s steepest post-expiry sales drops are yet to come. The high point in terms of worldwide sales at risk – $100 billion, or 6.6% of total sales – will be in about four years, with Keytruda, Opdivo, BMS/Pfizer’s clot-buster Eliquis (apixaban), Pfizer’s breast cancer drug Ibrance (palbociclib) and Lilly’s Trulicity (dulaglutide) for diabetes all due to lose protection in 2027-8. Last year, those drugs together sold almost $58 billion.

By 2030, that sales exposure will have halved.

Note: Sales at risk refers only to anticipated lost sales in the first year post expiry

By company, Merck and BMS are prominent, with JNJ, Novartis and AbbVie’s exposure ramping up more steeply toward the end of the decade, as drugs including J&J’s Stelara (ustekinumab) and Novartis Cosentyx (secukinumab), both sold for autoimmune conditions, reach the end of their protected lives.

By 2030, Dupixent, Skyrizi and Darzalex will each have spent over a decade on the US market; the oldest, Darzalex, will be 15. This brings them into the penumbra of the Inflation Reduction Act, which stipulates price negotiations on 13-year-old biologics costing Medicare more than $200 million per year. Life-cycle management strategies thus become even more important. Dupixent’s subcutaneous version, Faspro, was launched in 2020 with an added ingredient, hyaluronidase, that enhances the drug’s absorption from subcutaneous tissue into the blood. Merck is trying something similar with its subcutaneous Keytruda (MK-3475), which features in Evaluate’s top ten most valuable pipeline drugs in 2030 (see below).

Drug sponsors hope that combining their treatments with hyaluronidase may protect from Medicare’s price negotiation claws: Medicare counts all drugs with the same active ingredient as the same product for the purposes of the $200 million cost threshold, regardless of formulation or delivery route. That protection is far from a sure bet, though.

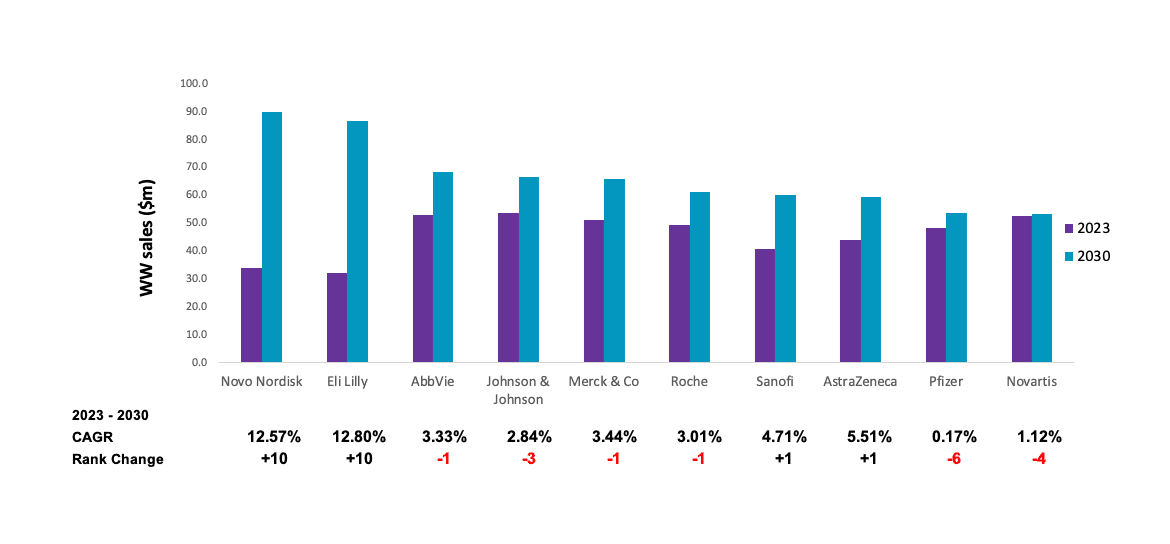

The GLP-1 agonists will catapult Novo and Lilly to the very top of the company league. Sales of each will grow by over 12% on an average annual basis, overshadowing even AstraZeneca’s anticipated 5%+ growth rate. This is a turn of the tables: neither company had made the top ten at all until their ninth and tenth places last year. (See World Preview 2023). Before that, Novo was categorised as mid-sized. Eli Lilly’s market capitalisation at the end of 2020 was less than half that of Johnson & Johnson.

Skyrizi helps haul AbbVie into third. Johnson & Johnson and Merck are on similar $60-70 billion 2030 sales trajectories, so there may be some shuffling. Novo and Lilly, too, may trade places as both continue to face supply issues. (Novo’s bid to acquire manufacturer Catalent, currently under Federal Trade Commission (FTC) review, may partially account for Wegovy’s lead over Zepbound in the ranking.) Barring major unforeseens, Novo and Lilly will remain at the top of the pile for the rest of the decade and likely beyond. (See chapter: Wegovy and Zepbound are just the start).