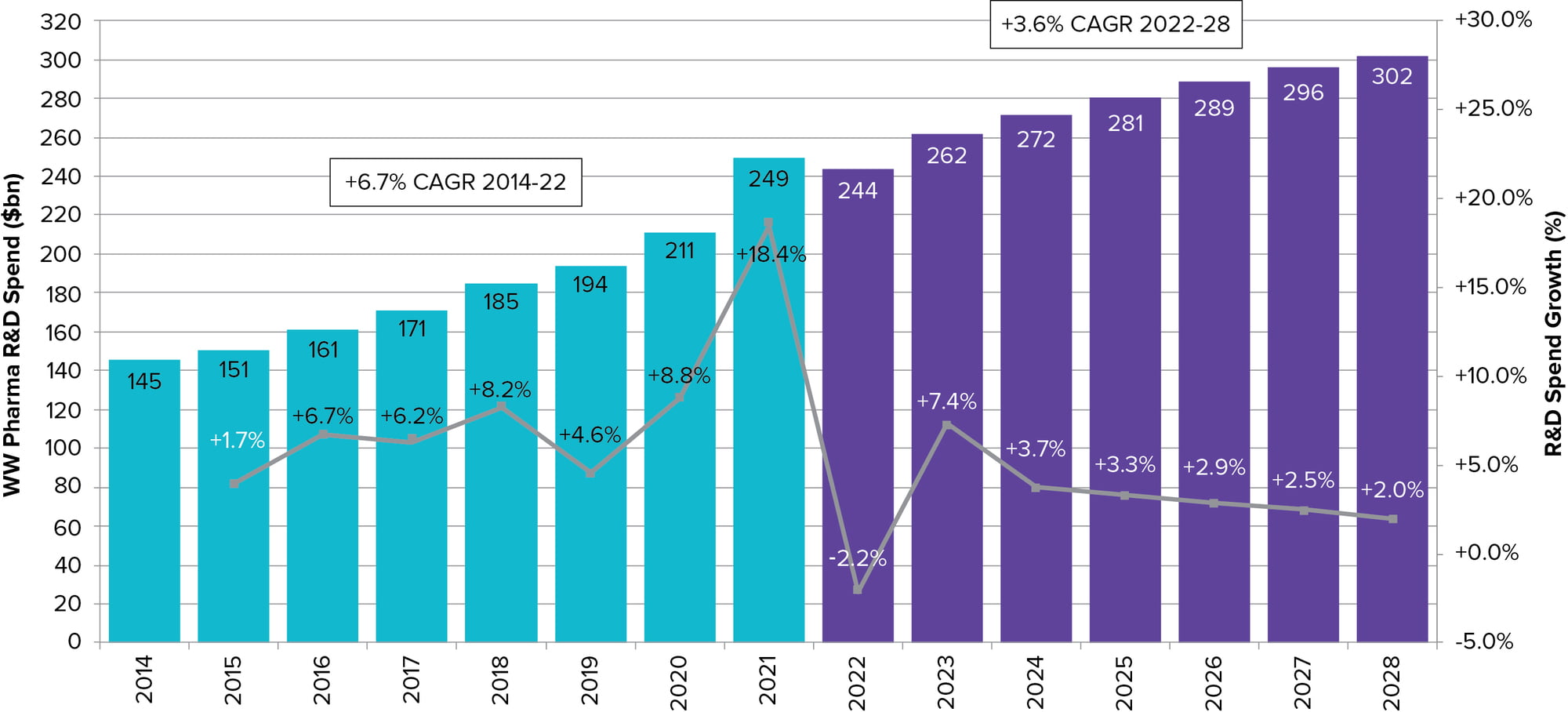

Worldwide R&D Spend

Is a return to growth on the cards?

Biopharma’s research and development spending is set to return to growth after the post-pandemic pullback of 2022. A more moderate rate of acceleration is predicted for the coming years, however, compared to the pre-Covid-19 years, a trend that is hard to explain. Note that these figures are not adjusted for inflation.

Possible explanations include a tighter focus on R&D productivity in an era of relatively high inflation and cost of capital; anticipated efficiencies as artificial intelligence becomes more widespread; or the long-term effects of a biotech bear market which has caused some serious slimming down of pipelines at the small end of the sector.

In reality, however, this last factor is unlikely to have had much of an impact on this sector-wide view. Top-level trends are driven by the spending decisions made at the very largest drug developers, whose budgets dwarf investments being made by smaller groups. To illustrate this point, the combined 2028 R&D bill for the top 10 companies in this report accounts for 37% of the $302bn total projected R&D spend that year.

WW Product Revenues ($bn)

Today's NPV ($bn)

Product

Company

Phase (Current)

Indication

2028

Sotatercept

Merck & Co

Phase III

Pulmonary arterial hypertension

2.6

11.6

Datopotamab Deruxtecan

Daiichi Sankyo + AstraZeneca

Lung cancer

11.5

CagriSema

Novo Nordisk

Obesity

1.9

10.3

Donanemab

Eli Lilly

Alzheimer's

2.1

8.8

KarXT

Karuna Therapeutics + Zai Lab

Schizophrenia

2.8

8.4

mRNA-1647

Moderna

Cytomegalovirus mRNA vaccine

1.5

7.1

Iptacopan

Novartis

Autoimmune diseases (incl. rare kidney disease)

1.1

6.2

Resmetirom (MGL-3196)

Madrigal Pharmaceuticals

Filed

NASH

2.2

6.0

Aficamten

Cytokinetics

Cardiomyopathy

1.7

4.4

Tiragolumab

Roche + Chugai Pharmaceutical

Cancer Immunotherapy

1.0

4.8

Top 10

19.4

79.1

Figure 8. Top 10 Most Valuable R&D Projects (Ranked by Net Present Value)

Source: Evaluate Omnium®, July 2023

Most of the sector’s highly valued R&D projects are late-stage assets owned by large developers, which have the resources to back large research programmes. While some like donanemab and cagrisema are internally generated projects, others have been bought in for considerable sums of money.

Merck & Co paid $11.5bn to access sotatercept, via its acquisition of Acceleron, while AstraZeneca handed Daiichi Sankyo $1bn in up-front fees to license certain rights to datopotamab. As such, expectations are high for deals to emerge for assets that remain in

the hands of smaller companies, like Karuna’s schizophrenia project, KarXT, and Madrigal’s resmetirom. The latter is one of the first agents to have shown real promise in NASH.

Some of these projects still have much to prove. Roche’s anti-TIGIT MAb tiragolumab, for example, which has disappointed in the clinic though some still harbour hopes that the anti-cancer mechanism will prove its worth.

The net present value of these agents is computed by Evaluate Omnium from sellside forecasts.

The combined 2028 R&D bill for the top 10 companies in this report accounts for 37% of the $302bn total projected R&D spend that year.