The Top Players & Drugs in 2028

It’s tight at the top and there are new faces in the top 10

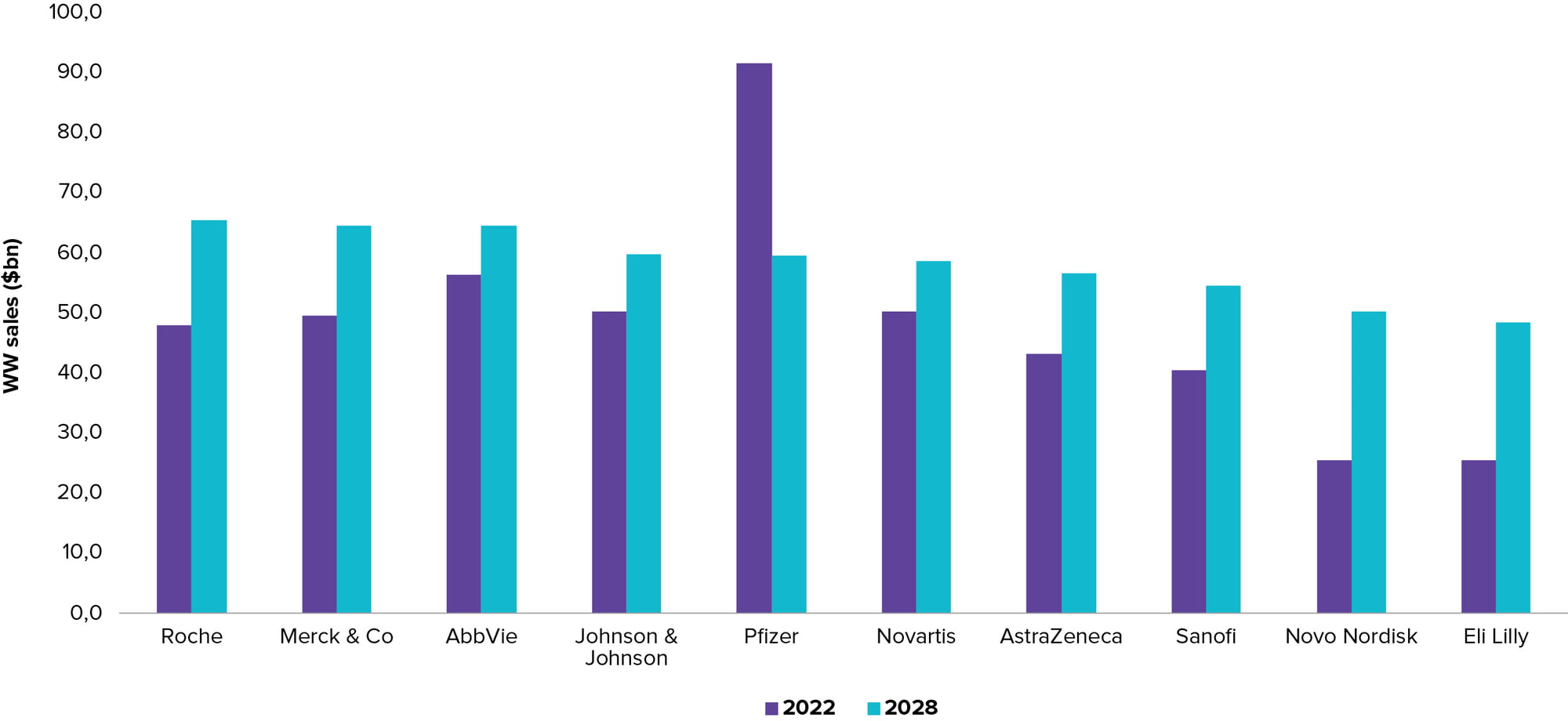

It is for the reasons mentioned previously – biotech products’ high prices and longevity – that many of the biggest biological players sit amongst the world’s largest drug makers. Roche comes out on top in 2028 when the sector is ranked on prescription drug sales.

The Swiss developer helped trigger the cancer antibody revolution with products like Herceptin and Avastin, and its future growth will be driven by a new suite of monoclonals: Tecentriq for cancer, Ocrevus for MS and the eye-disease treatment Vabysmo. Roche also boasts the leading non-oncology bispecific, Hemlibra, sold for haemophilia.

This broad estate means that, based on current projections, the Swiss giant will keep Merck & Co from the top spot in 2028. With little between the top three companies’ sales forecasts that year, however, the order of names on the podium is far from finalised.

This analysis also finds two new entrants into the top 10: Novo Nordisk and Eli Lilly. The Danish firm is currently enjoying a leading position in the successful incretin class, which includes drugs sold for type 2 diabetes and, increasingly, obesity. But Lilly is catching up.

With little between the top three companies’ sales forecasts that year, however, the order of names on the podium is far from finalised.

The GLP-1 agonist semaglutide, which is sold under various brand names, lies behind Novo Nordisk’s growth prospects. Lilly’s Mounjaro, which hits GIP as well as GLP-1, arrived on the market in May 2022, with massive demand creating one of biopharma’s most successful drug launches.

The huge sales these agents are seen generating will help Novo and Lilly push Bristol Myers Squibb and GSK from the top 10 by 2028, Evaluate Pharma predicts.

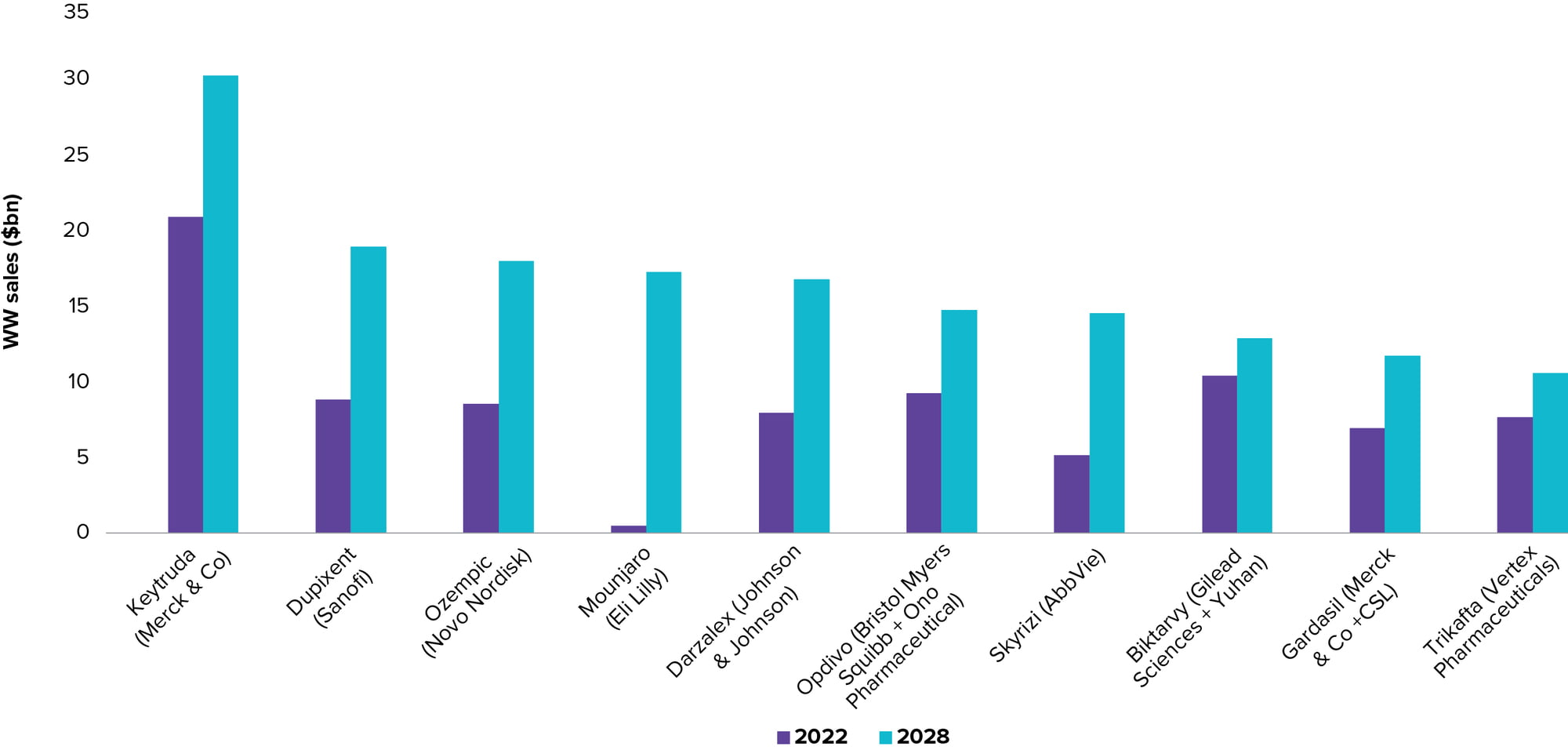

Merck & Co’s Keytruda is projected to become the world’s top-selling drug in 2023, a status that the anti-PD-1 antibody is seen retaining until the end of this decade. This forecast does not include numbers being attached to a subcutaneous formulation that Merck has in phase 3 development; 2028 sales forecasts for that project currently sit at $2.4bn.

This class of anti-cancer checkpoint inhibitor, which also includes Bristol Myers Squibb’s Opdivo, Roche’s Tecentriq and AstraZeneca’s Imfinzi, is a big driver of the sector’s top line. After topping $40bn last year, sales generated by the anti-PD-(L)1 mechanism are seen hitting $71bn by 2028.

Incretins are also seen contributing billions of new sales in the coming years. Both Ozempic and Mounjaro have consistently beat analysts’ revenue expectations, and a lot more data are due in potentially large new settings like the liver disease non-alcoholic steatohepatitis, or NASH.

It should be noted that this analysis understates the size of Novo’s semaglutide franchise. Sold as Ozempic in type 2 diabetes, the drug is also marketed in obesity as Wegovy; there is also an oral formulation for diabetes, called Rybelsus. Combining 2028 forecast sales for the three brands gives $33bn, outstripping even Keytruda.

Separately, Gardasil is a new entrant to this top 10 list versus the previous edition of the World Preview. Merck & Co is experiencing growing demand in less developed regions for the product, an HPV vaccine which protects against cervical cancer.

After topping $40bn last year, sales generated by the anti-PD-(L)1 mechanism are seen hitting $71bn by 2028.