Q3 Shows Ongoing Venture Fundraising Challenges In Tough Financial Market

VC data from Evaluate show quarter-over-quarter drops in the number of biopharma companies raising private cash and in the amount of money raised as investors ride out public market troubles.

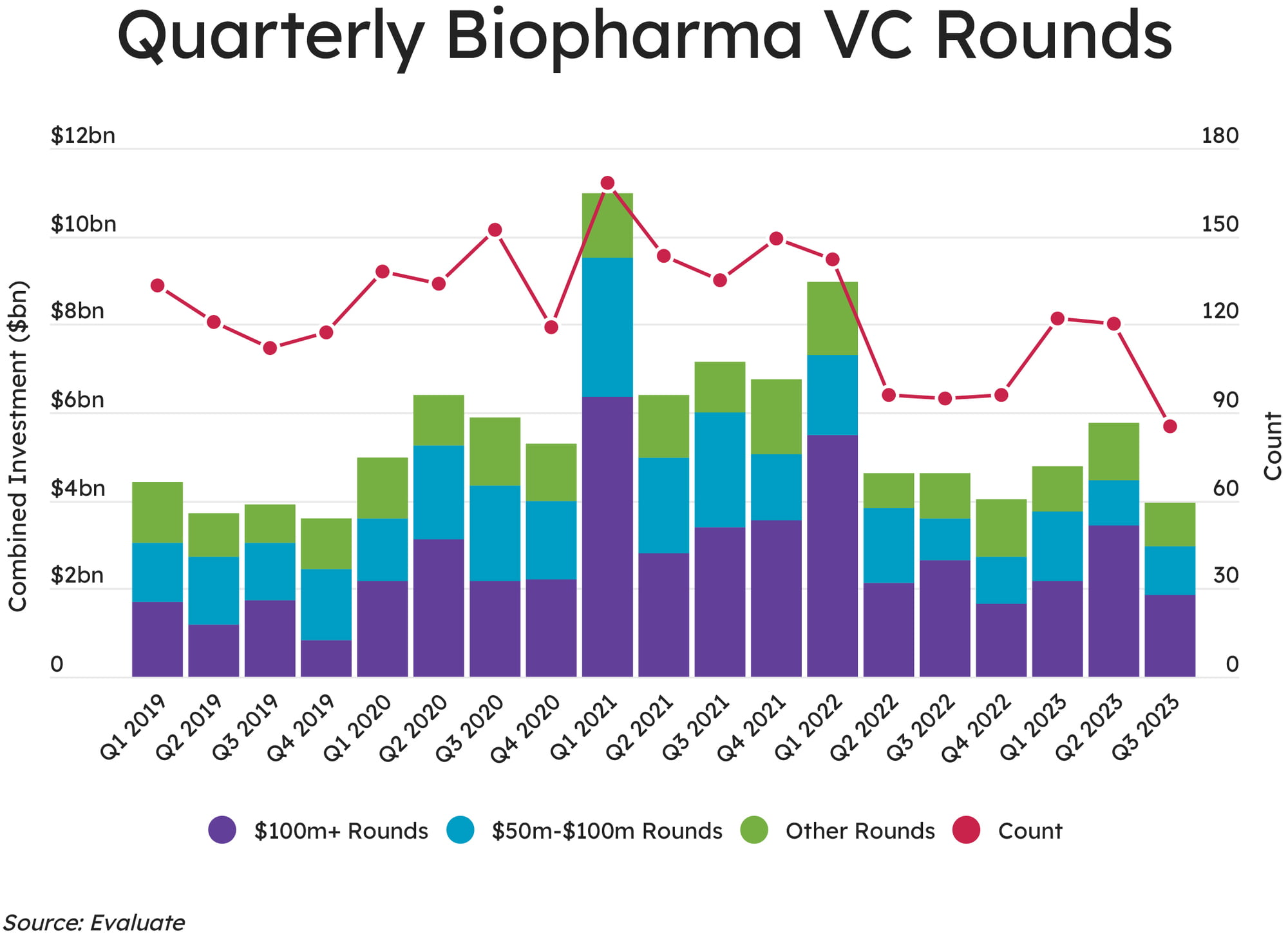

Biopharmaceutical companies raised $3.95bn in venture capital globally during the third quarter of 2023, but firms raising small and large rounds brought in far less cash during the quarter compared to Q1 and Q2, according to Evaluate’s latest set of VC funding data. Even some of the largest venture rounds during Q3 reflected the ongoing challenge of raising money at a time when start-ups’ public company peers are struggling to maintain their valuations and many private firms are unable to go public.

The lack of initial public offerings in 2022 and 2023 relative to the boom year of 2021 has hit venture capital investors hard, because they need to reserve cash to support their portfolio companies that must wait for better IPO conditions before they go public or are acquired. This has made it harder for VC investors to back new start-ups or support large pre-IPO financings. As a result, Evaluate tallied 85 venture capital financings in Q3, down from 122 in Q1 and 120 in Q2.

The $3.95bn raised included $1.86bn in VC mega-rounds of $100m or more, $1.1bn in financings in the $50m-$100m range and $0.99bn in rounds totalling less than $50m. By contrast, Q2 mega-rounds added up to almost twice as much as the Q3 total at $3.45bn. Financings in the under-$50m category dropped about 20% from the Q2 total of $1.27bn, while the $50m-$100m segment lifted slightly from $1.03bn.

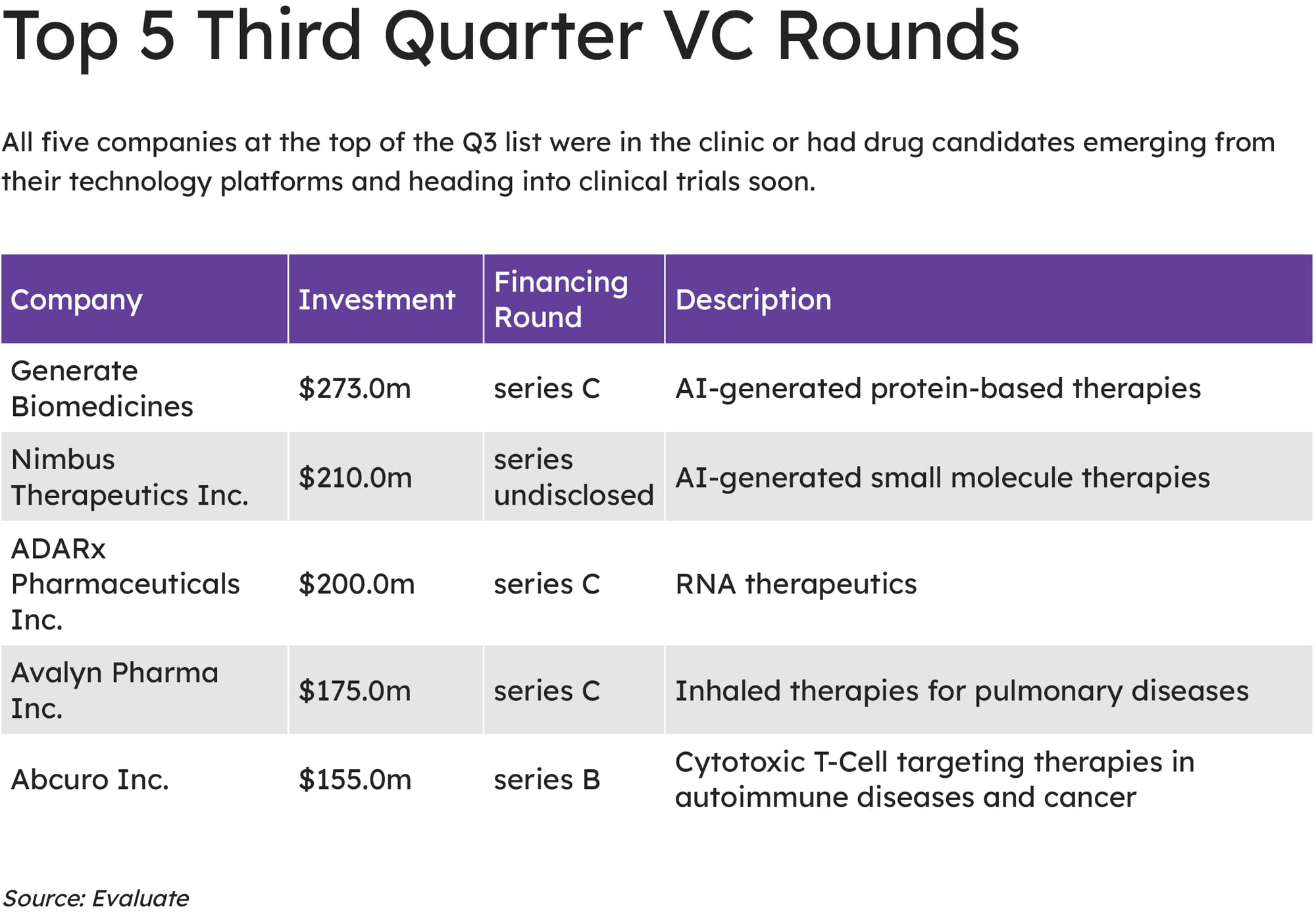

Generate Biomedicines topped the list of Q3 fundraisers with a $273m series C round, which it will use to take more drug candidates from its artificial intelligence-enabled drug discovery platform into clinical development. The company already has a monoclonal antibody against the SARS-CoV-2 virus in the clinic. Even so, its series C round was almost $100m smaller than its $370m series B round in November 2021, reflecting the reality that many private companies have faced in 2023 – having to raise less cash in current VC rounds than in prior financings to stay afloat.

ADARx Pharmaceuticals, Inc., which landed at no. 3 on the list of top 5 fundraisers in Q3, employed another strategy earlier this year that has become common for private companies under current financial market conditions – extending a prior funding round rather than raising a new, smaller round. ADARx extended a $75m series B it raised in September 2021 by $46m when it completed a series B-1 financing in January 2023. That funding kept the RNA therapeutics specialist going while it went on to raise a $200m series C it revealed in August.

Avalyn Pharma, Inc. garnered $62m in series A funding in May 2017 but brought in just $35.5m in series B cash in April 2020, although that was in the early days of the COVID-19 pandemic when biopharma valuations had not been boosted yet by the industry’s response to the global health crisis. The company bounced back in a big way in Q3 of this year, earning the no. 4 spot in the top 5 VC financings list with a $175m series C round to fund mid-stage clinical trials for its inhaled idiopathic pulmonary fibrosis drug candidates.

Similarly, Abcuro, Inc. had about a 2.5-year gap between its $42m series A-1 financing in early 2021 and its $155m series B round in August, giving it the fifth-largest VC financing of Q3. The proceeds will fund ongoing and planned clinical trials for its rare disease and oncology programs.

The outlier within the top 5 is Nimbus Therapeutics, Inc., which raised $210m in September to fund its early clinical-stage programs despite already having billions of dollars on its balance sheet. Q3’s no. 2 fundraiser brought in the new capital on top of receiving $4bn up front in December 2022 when it sold a late clinical-stage TYK2 inhibitor to Takeda Pharmaceutical Co. Ltd. However, the latest financing may have been a crossover round intended to bring in new investors that could give Nimbus the cache it needs to pursue an IPO in the near term.

Evaluate’s review of Q3 venture capital financings focused on companies with named drug candidates in their pipelines, but looking at firms that raised VC cash to fund technology platforms that have yet to generate publicly disclosed therapeutic candidates would add a $200m series B mega-round raised by Genesis Therapeutics – a company using its artificial intelligence platform to generate novel small molecules – as well as a $109m series B round for preclinical-stage Alltrna, which is using AI to develop transfer RNA (tRNA) medicines.

Overall, Evaluate tallied $14.5bn in venture capital financings for the first three quarters of 2023 versus $22.2bn for all four quarters of 2022 and $31.3bn in 2021. By contrast, analysts at Stifel, based on data from CapitalIQ that includes technology platform companies, said in a 1 October report that based on VC fundraising through Q3, the annualised total for 2023 is about $36bn, which is down 28% from $50bn in 2022 and 58% below the record-setting sum of $70bn in 2021, but on par with the $37bn raised in 2020.

“Venture investors are stretching out their dollars in light of the weaker investment environment,” Stifel’s analysts noted. However, they pointed out that September fundraising suggests a potential turnaround, with the second-highest monthly total for 2023 after a prior surge in June.

Even so, fundraising by biopharma-focused VC firms has slowed, so it remains to be seen if these venture funders have the cash needed to support an increased level of investment in drug developers in Q4. “Venture funds raised $400m in August and $570m in September,” Stifel noted. “The pace is well below what was seen in 2021 and 2022.”