Biotech IPOs Get Bigger, But Not Necessarily Better

The first $1bn quarter since 2021 suggests that biotech’s IPO window is opening once more. But times remain tough, and many recently listed groups have seen their valuations fall.

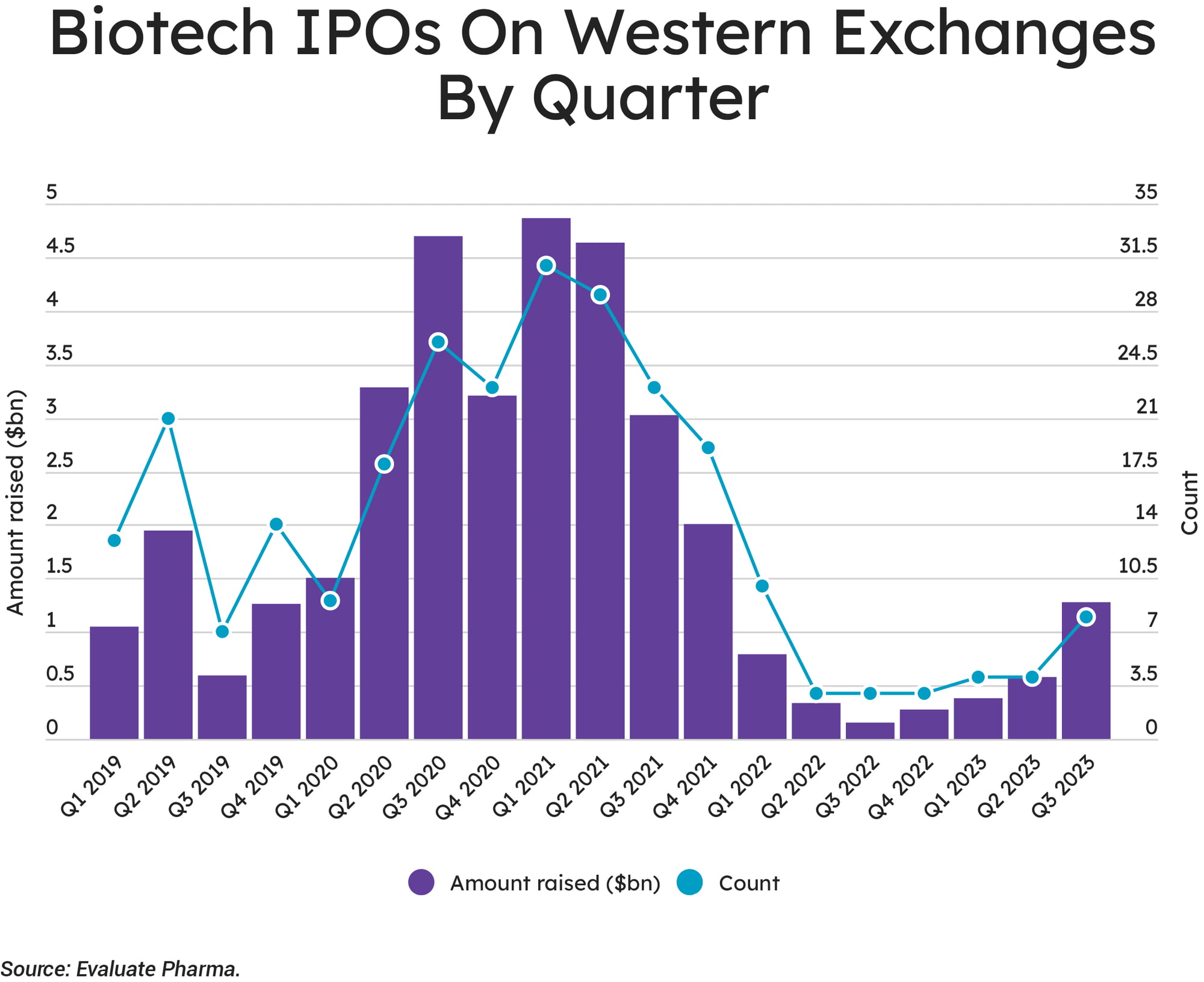

Biopharma is going public again. That is the unmistakable trend throughout the year so far – indeed it has been clear since the spring of 2022. And the third quarter has seen the most cash raised by floating biotech companies since the end of 2021, totalling $1.3bn.

This is a rosy picture until you look at how these companies have done on the stock markets since their IPOs. The eight companies that went public in the third quarter have lost 29% of their value on average, though even this is an improvement on those that floated in the second quarter. And all the action is in the US, with precisely zero biopharma IPOs occurring in Europe in 2023.

Eight biopharma IPOs raised a total of $1.3bn in Q3 2023

But these eight groups have lost an average of 29% of their value since their debuts

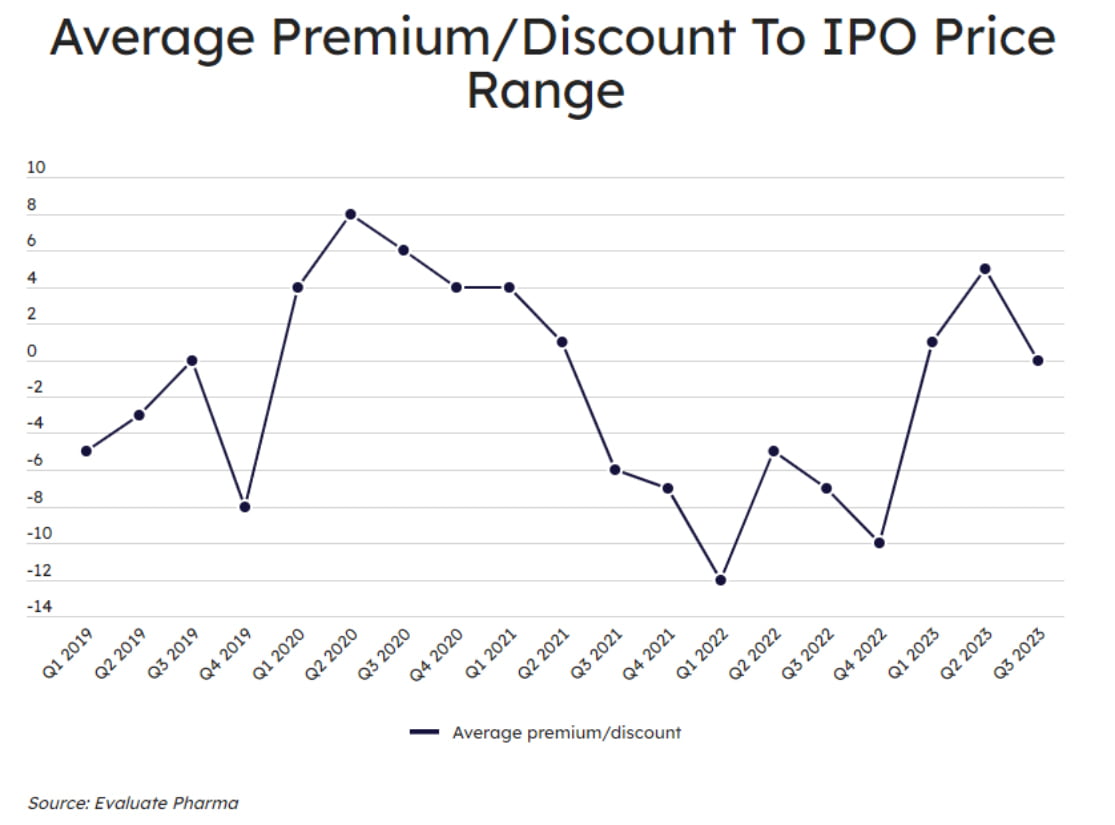

On average, IPOs are no longer priced at a premium

The analyses below track IPOs of biopharma companies on Western stock exchanges; Asian and other markets are excluded. It also excludes large spin-outs such as that of Kenvue Inc. from Johnson & Johnson, so as to concentrate on younger companies seeking growth capital.

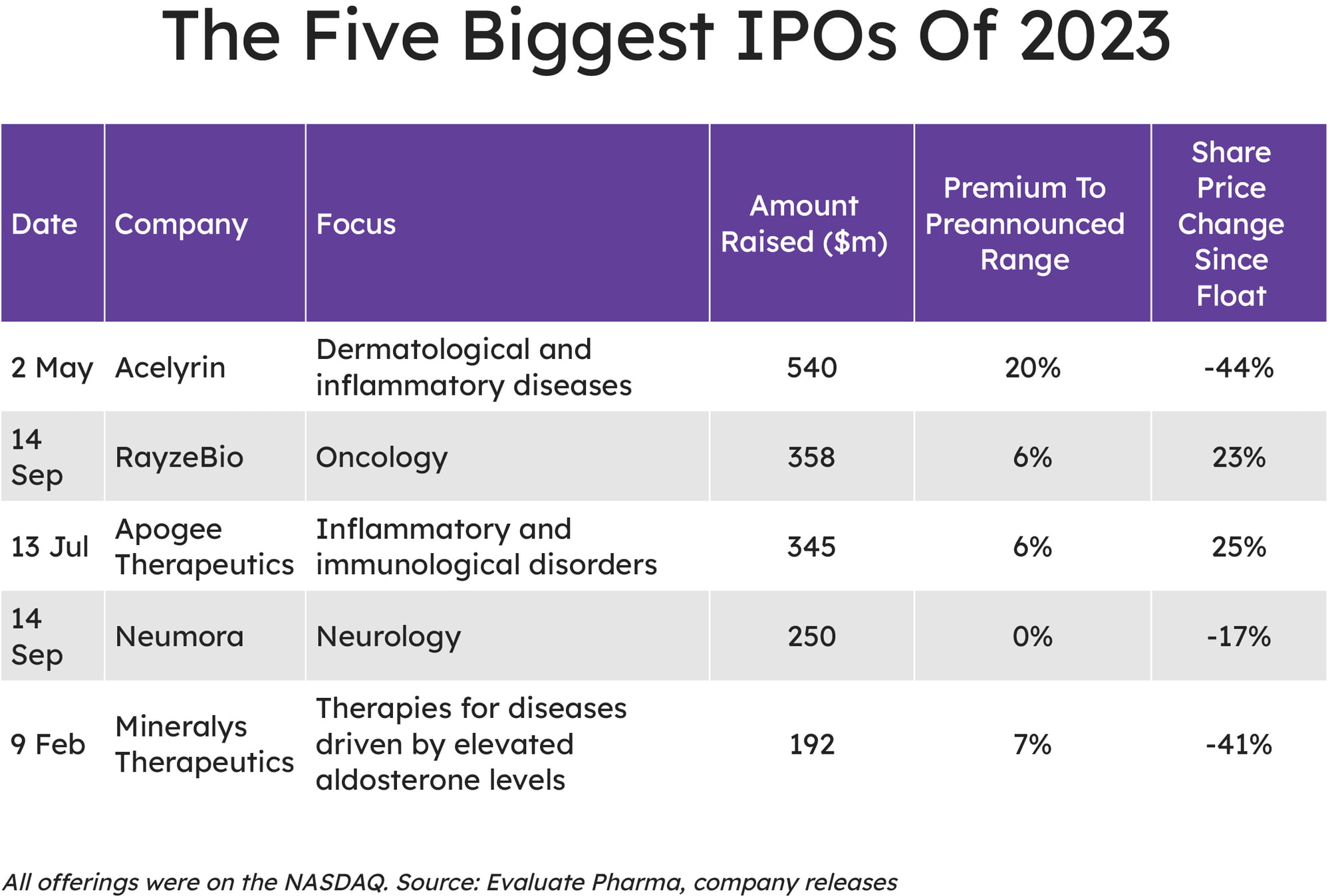

Underlining the resurgence in the third quarter is the emergence of three of the five largest offerings of the year. The fates of these companies, however, have diverged sharply.

Apogee Therapeutics, LLC raised $345m in July in an upsized offering, and was able to price at the top end of its preannounced range. This is despite its most advanced asset, an IL-13 inhibitor known as APG777, having not at that point entered Phase I. Its first human trial started subsequently, in the lead indication of atopic dermatitis. Data are due on 2024, as is the initiation of a Phase II trial, and expectations are clearly high: Apogee’s share price has climbed by 25% since its float.

Also doing nicely is RayzeBio, Inc., whose upsized $358m float also went out at the top of its range. The group develops radiopharmaceuticals, an area that has suddenly become white-hot: witness Genentech, Inc. ’s collaboration with PeptiDream Inc. and Eli Lilly and Company’s purchase of POINT Biopharma Global Inc.

Contrast this with Neumora Therapeutics, Inc.. The group’s once-daily oral kappa opioid receptor antagonist, navacaprant, succeeded in a Phase II trial in major depressive disorder and will move into late-stage trials soon. But neurology is an iffy area, littered with Phase III failures. Investors are skeptical judging by the 17% share price slide Neumora has racked up in just three weeks.

At least Neumora is doing better than Acelyrin, Inc., which floated in Q2. Not only was Acelyrin’s the biggest float of the year, at $540m it ranks as the third largest biotech IPO, on amount raised, since Moderna listed in 2018. Its focus on immunology, a tempting area for investors, helped – but disaster struck last month when its lead product, izokibep, failed in a Phase IIb/III study in the skin disease hidradenitis suppurativa. Acelyrin insisted that it would push on into pivotal studies, but found itself nursing a 44% valuation loss at the end of last quarter.

It is worth noting that, while Acelyrin went out at an astonishing 20% premium to its preannounced range, the groups that floated in the third quarter priced their offerings more conservatively. The macroeconomic reasons for this are clear. In many Western economies, interest rates are expected to stay high, as central banks continue to grapple with persistent inflation. Consequently, the cost of capital remains elevated, and this, along with tighter credit, makes financing more challenging.

The chart below tracks the difference between the initially proposed range and the price at which these new issues floated, and shows that listing companies have tempered their share price expectations, with firms and their bankers having adjusted to the current financial climate.

The mixed performance of the recent debutants makes it hard to judge what might await biotech companies that are planning an IPO. None has stated their intention to float, perhaps wary of the caprices of the public market. Perhaps the success of early-stage groups like Apogee bodes well for the final quarter of 2023. But floating is always a bit of a gamble, and with investors punishing mis-steps heavily, those companies that do go public will have to be very confident.