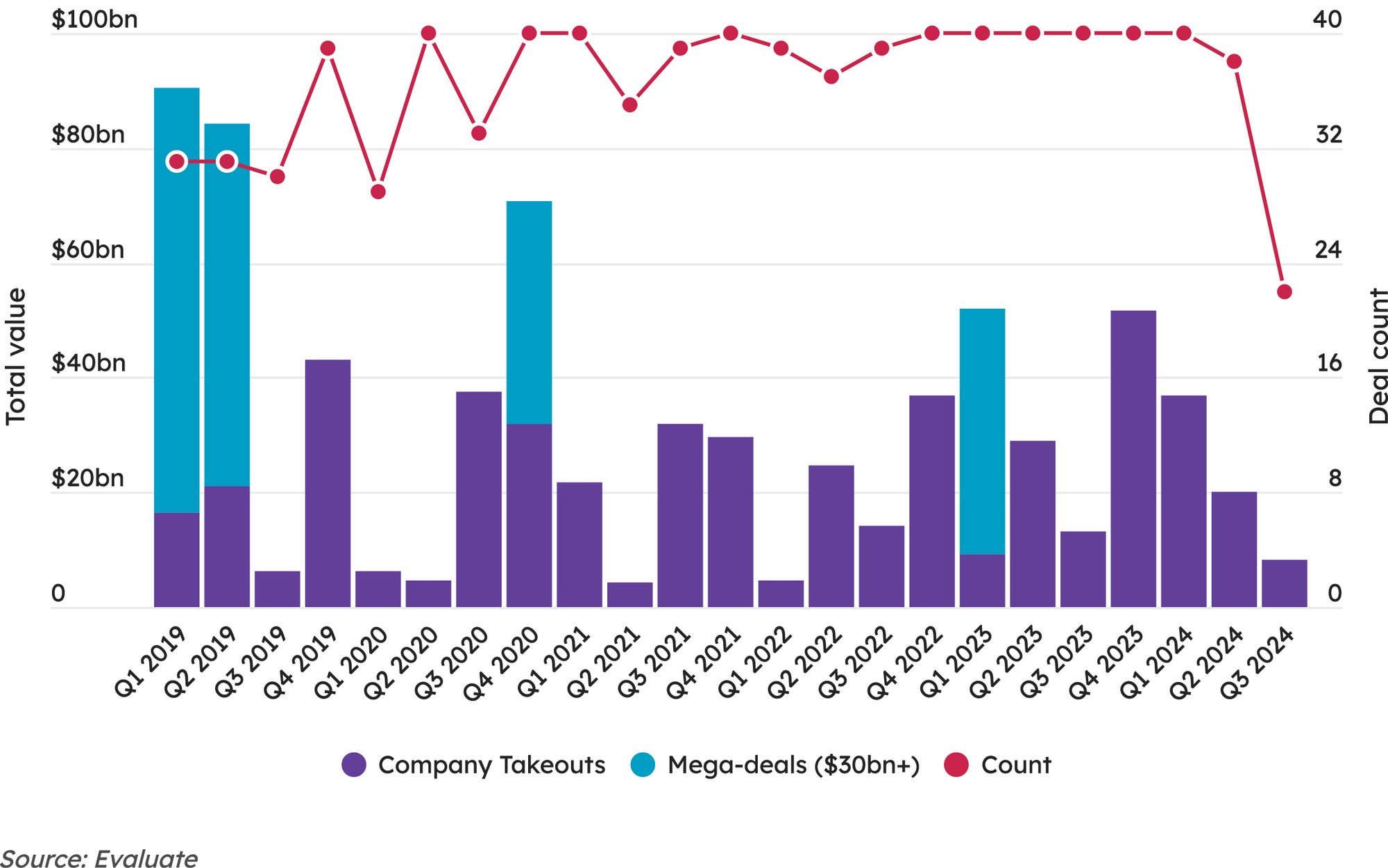

The biopharma industry posted 22 mergers and acquisitions during the third quarter, according to Evaluate, for a total of $8.2bn. Those tallies marked a second consecutive quarter of decline.

Merger-and-acquisition activity in the biopharmaceutical sector fell off sharply during the third quarter, a second consecutive quarter of decline after the busy and high-spending Q4 2023 and Q1 2024, Evaluate data reveal. Deal volume and total deal value were down sequentially, while the quarter’s largest deal was notably smaller than the biggest recorded during Q2.

Last year’s acquisition activity finished with a bang with a pair of $10bn-plus deals in the final month of 2023, and this year’s first quarter produced Novo Nordisk A/S’s $16.5bn takeout of Catalent, Inc. But M&A in the second quarter totalled just over $20bn, spread across 38 transactions, with Vertex Pharmaceuticals Incorporated’s $4.9bn purchase of Alpine Immune Sciences Inc. the largest deal during those three months.

Maybe it was just the summer heat that created an even more relaxed pace, but Q3 2024 saw a total of 22 M&A deals valued at slightly more than $8.24bn. (See chart.) That anaemic total-dollar figure was the lowest M&A expenditure recorded for a full quarter since the roughly $4.6bn reported during the first quarter of 2022. The past quarter was only the fourth during the 2020s that saw less than $10bn of biopharma M&A activity.

The 22 total M&A deals in Q3, while in line with some recent quarterly totals, tied Q1 2020 for the lowest total this decade. The fourth quarter of 2023, with 49 deals, and the first quarter of 2024, with 54, yielded totals exponentially higher than Q3, which also declined 37% from the 38 deals made in Q2 2024.

This occurred in an environment where large pharma firms have significant capital to deploy, but financial market conditions remain tough for smaller companies, which could make takeout targets available to buy at non-peak prices. It is difficult to project what this means about overall sector M&A attitudes following a first half of 2024 in which deal volume increased, but valuations decreased compared to the first six months of 2023.

Quarterly Biopharma M&A

Another significant decline from Q2 to Q3 of 2024 was in individual deal valuation. There were seven transactions valued at $1bn or greater up front during the first quarter, which then increased to eight in Q2, but just three deals broke the $1bn mark during the third quarter. This reflects a near-term trend of smaller acquisitions, as the biopharmaceutical sector has not seen a mega-merger valued at $30bn or greater since the first quarter of 2023, when Pfizer Inc. acquired Seagen Inc. for $43bn.

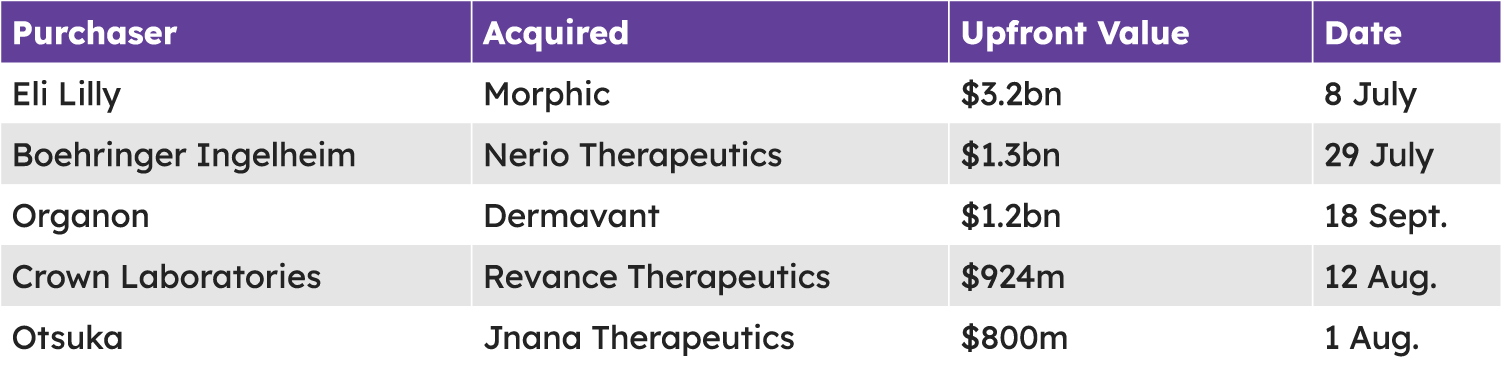

Only one of the three deals valued at $1bn or more up front this quarter was valued above $2bn – the third quarter’s biggest deal by value was Eli Lilly and Company’s $3.2bn takeout of Morphic Therapeutic, Inc. on 8 July, in a bid by the Indianapolis pharma to bolster its gastrointestinal disease portfolio. Morphic’s Phase II MORF-057, an oral alpha-four/ beta-7 (α4β7)-targeting compound being developed for ulcerative colitis and Crohn’s disease, primarily drove the deal.

Lilly/Morphic was the only Q3 acquisition that would have made the first quarter’s list of the five biggest M&A deals.

Beyond that deal, Q3 yielded Boehringer Ingelheim GmbH’s $1.3bn bid for Avalon Bioventures-backed Nerio Therapeutics. The German pharma often points out that its business development strategy is built primarily on partnerships with other companies or academic/institutional research bodies, so BI posting the second-largest takeout of the quarter is an unusual event. In Nerio, BI said it sees an opportunity to bolster its immuno-oncology pipeline with a novel preclinical checkpoint inhibitor that inhibits the protein tyrosine phosphatases N1 and N2 (PTPN1 and PTPN2).

The third quarter of 2023 saw 22 biopharma M&A transactions valued at slightly more than $9.4bn, with both totals down from the second quarter.

The Q3 totals mark the second consecutive quarter of decline in both deal volume and aggregate value, following the hectic activity seen during Q4 2023 and Q1 2024.

The quarter’s largest acquisition was Lilly’s $3.2bn GI disease-focused buyout of Morphic.

The quarter’s third-largest M&A deal was Organon’s 18 September decision to acquire Roivant Sciences’ dermatology-focused subsidiary Dermavant Sciences Inc. for $1.2bn. The transaction added a branded psoriasis drug, Vtama (tapinarof cream 1%), to Organon’s book of business, centred mainly on women’s health and biosimilars.

The Five Largest M&A Deals Of The Third Quarter

The fourth- and fifth-highest valued M&A transactions during Q3 both featured upfront cash of less than $1bn, although Otsuka Holdings Co., Ltd.’s acquisition of Jnana Therapeutics Inc. for $800m up front could ultimately be worth about $1.125bn if development and regulatory milestones are realised. A San Francisco-based drug discovery specialist, Jnana brings its next-generation chemoproteomics platform RAPID to Otsuka, along with Phase II JNT-517, an oral SLC6A19 inhibitor being studied in phenylketonuria.

The fourth-largest deal of Q3 was Crown Laboratories Inc.’s $924m buyout of Revance Therapeutics, Inc., the second transaction among the quarter’s five largest that was centred on dermatology. The deal announced on 12 August brings Crown a portfolio of commercial products including a direct competitor to AbbVie Inc.’s Botox (onabotulinimtoxinA) with Daxxify (daxibotulinumtoxinA), approved by the US Food and Drug Administration to treat glabellar (frown) lines and cervical dystonia. Daxxify also is in Phase II for other aesthetic indications (forehead, lateral canthal and upper facial lines) and for therapeutic indications, including upper limb spasticity after stroke or traumatic brain injury.

Lilly/Morphic was the only Q3 acquisition that would have made the first quarter’s list of the five biggest M&A deals.”