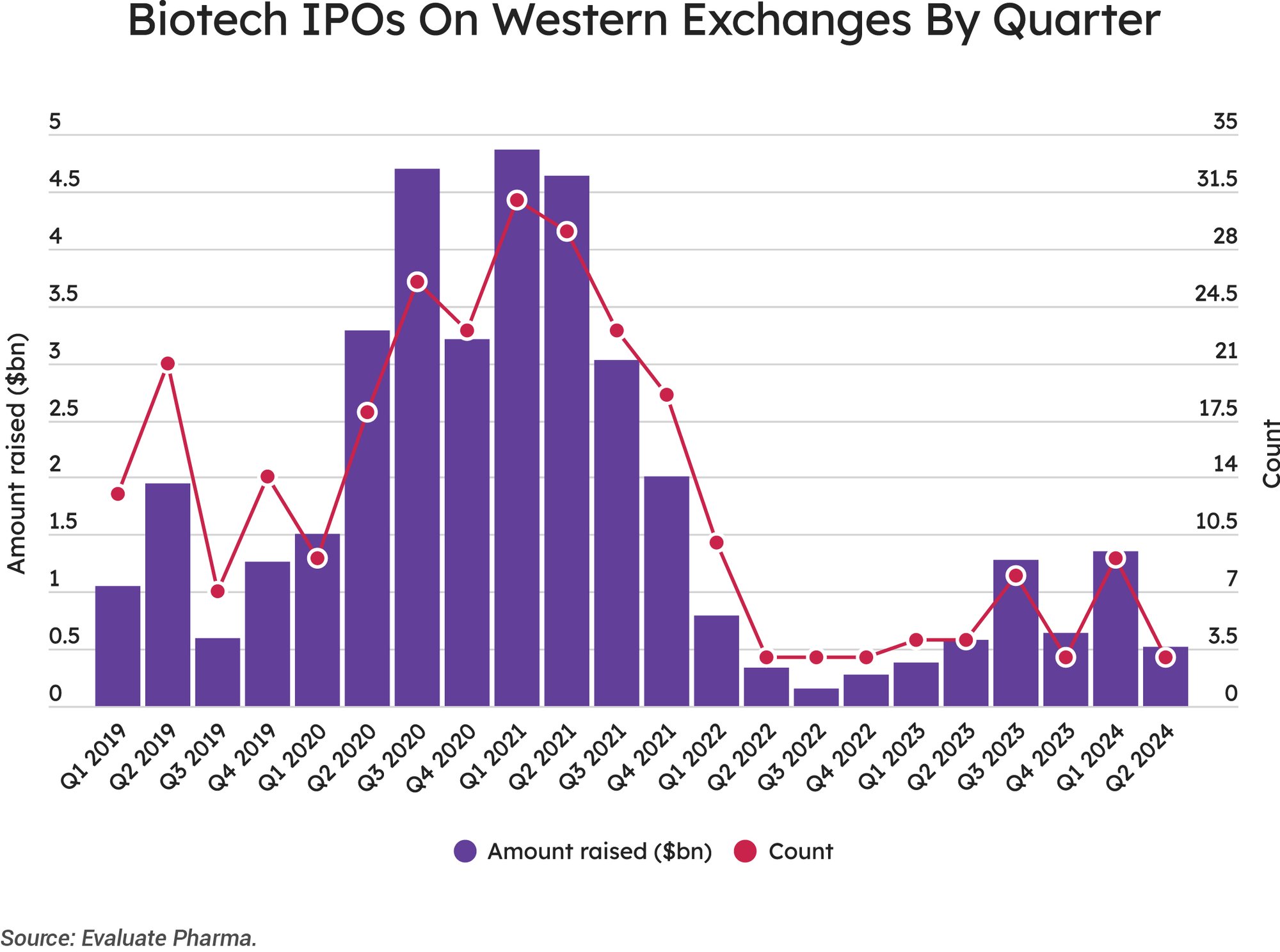

IPOs Collapse In The Second Quarter

Biotechs have had a difficult time raising cash through flotations over the past quarter, with one stepping away altogether.

Arguably the defining biotech IPO of the second quarter of 2024 was the one that didn’t happen. In June, radiopharmaceuticals developer Telix Pharmaceuticals Ltd. yanked its NASDAQ filing at the last minute, saying potential investors were not willing to pay the price it sought.

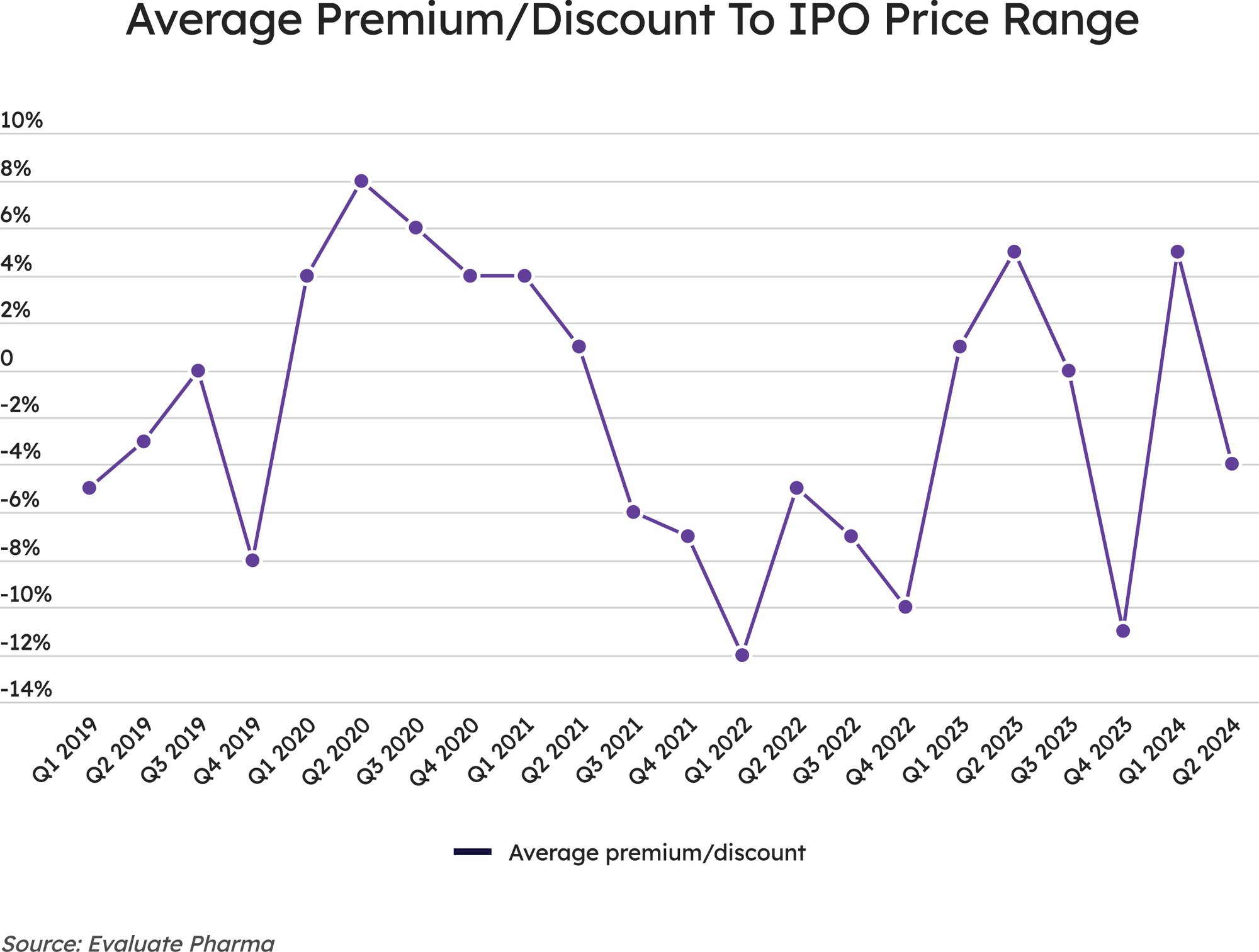

If that weren’t sign enough of a gloomy IPO microclimate, the fact that just three deals did get away this past quarter – and only then by pricing on average more cheaply than they had intended – confirms it. This is somewhat disappointing since the first quarter of this year looked fairly bright, with nine market debuts raising $1.4bn.

KEY TAKEAWAYS

Just three biotechs floated on Western exchanges in Q2 2024.

They raised a total of $516m.

And did so at an average discount of 4% to their pre-announced pricing.

In April, Contineum Therapeutics raised $110m to fund development of assets in the neurological and inflammatory areas. Its lead product is PIPE-307, a muscarinic acetylcholine receptor M1 antagonist in Phase II for relapsing-remitting multiple sclerosis; data could come next year. The agent is partnered with Johnson & Johnson, which plans to take PIPE-307 into Phase II in depression this year. Having a big name on side might have helped reassure investors that Contineum was a safe repository for their cash.

But Contineum had to take a haircut to get its offering off the ground, pricing at the low end of its preannounced range, and closed its first day’s trading down by 4%. Happily its performance has improved since; by the end of the quarter its stock was up by 10%.

LULL

A two-month lull in proceedings was broken by Rapport Therapeutics, which got off to a better start. It offered eight million shares at $17 each, the middle of its proposed range, raising $136m, and sold another 1.06 million shares in a private placement, bringing the total proceeds to $154m. Its stock closed up 22.4% at $20.80 on 7 June, its first day of trading.

Another neurology-focused company, Rapport has three products in Phase I, for epilepsy, neuropathic pain and bipolar disorder. The company did nicely in its first three weeks on the market, its shares having climbed 37% by the end of June.

The biggest IPO of the quarter was that of Alumis, Inc. – but, in a further show of how difficult the atmosphere is at the moment, even that was a disappointment. The company had planned to raise up to $318m, but in the event was only able to sell 13.1 million shares at $16, the bottom of its range, bringing in $210m. After its first day on the market, which was also the last day of the second quarter, Alumis closed down by 17%.

A concurrent private placement of a further 2.5 million shares at the same price took the total Alumis raised to $250m. The group will put the cash towards taking its TYK2 inhibitor, ESK-001, into Phase III studies in moderate-to-severe psoriasis.

The fact that two of the three listing groups had to price their offerings lower than they had planned is a reversal of what was seen last quarter, when the nine IPOs went out at an average 5% premium. This is more evidence that investors are once again being careful with their cash – and it was this circumspection that led Telix to back away from its IPO.

And the situation is particularly dire in Europe. The last biotech to list on a European stock exchange was the French group Aelis Farma, which raised €25m ($27m) through a Euronext IPO in February 2022 – more than two years ago.

The fact that two of the three listing groups had to price their offerings lower than they had planned is a reversal of what was seen last quarter,