M&A Activity During Q2 Declined In Volume And Valuation

Following a pair of $10bn+ deals in Q4 2023 and a $16.5bn takeout in Q1, the second quarter saw no acquisition priced as high as $5bn. Aggregate deal volume and values dropped from Q1.

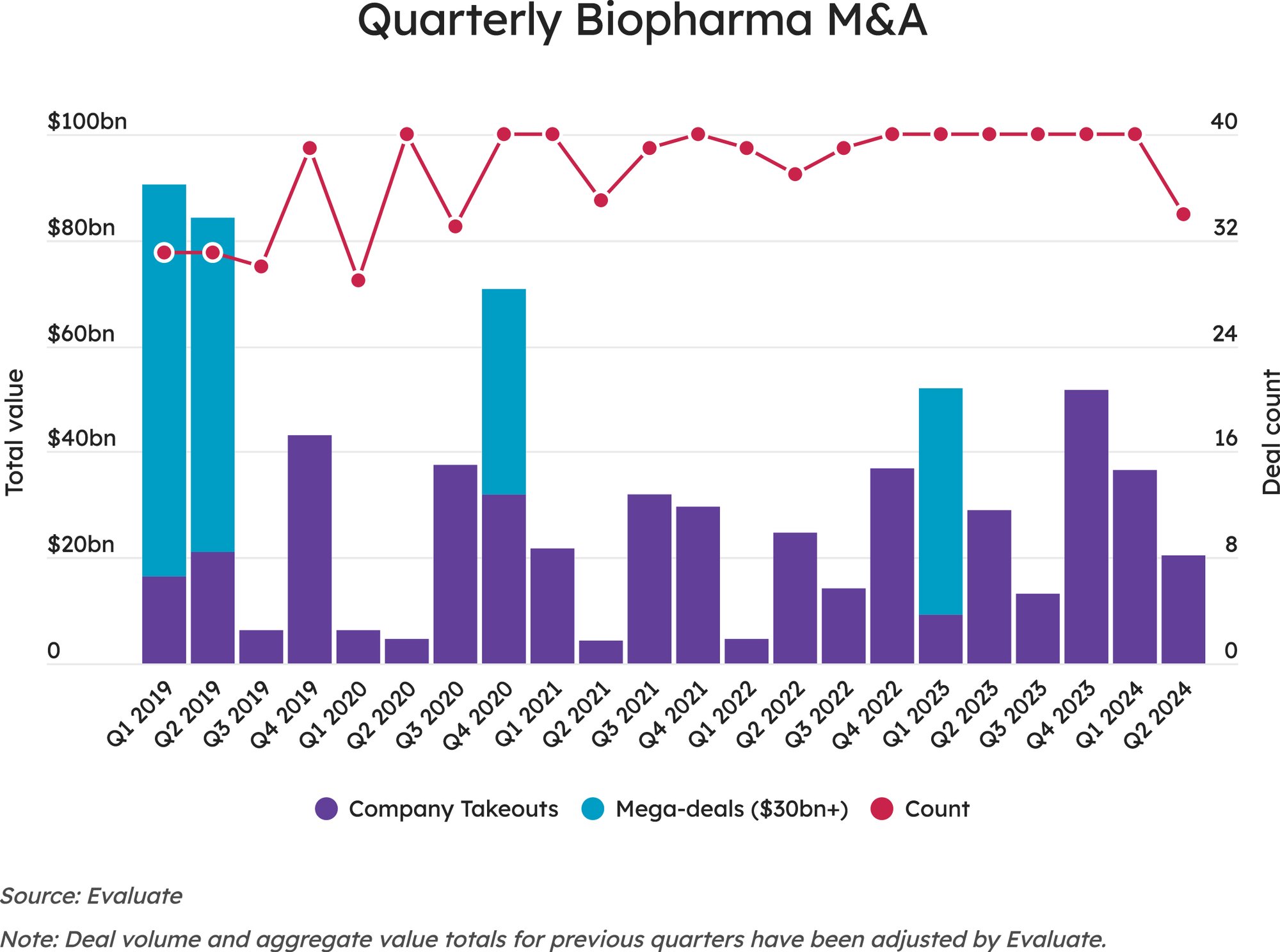

After a strong start to biopharma merger-and-acquisition activity in the first quarter of 2024, transactions declined notably in the second quarter, according to data provided by Evaluate. The second quarter saw 34 M&A transactions, down from 59 during the first quarter, while the aggregate dollar value of those deals came in just below $20.4bn.

The aggregate dollar total declined 44% from the adjusted Q1 total of nearly $36.6bn, although the number of acquisitions with upfront value of $1bn or higher actually increased to eight, from seven the previous quarter. Total upfront value from M&A deals during Q2 was slightly more than $16.4bn, down substantially by 55% from the nearly $36.5bn in upfront spending seen during Q1 of 2024.

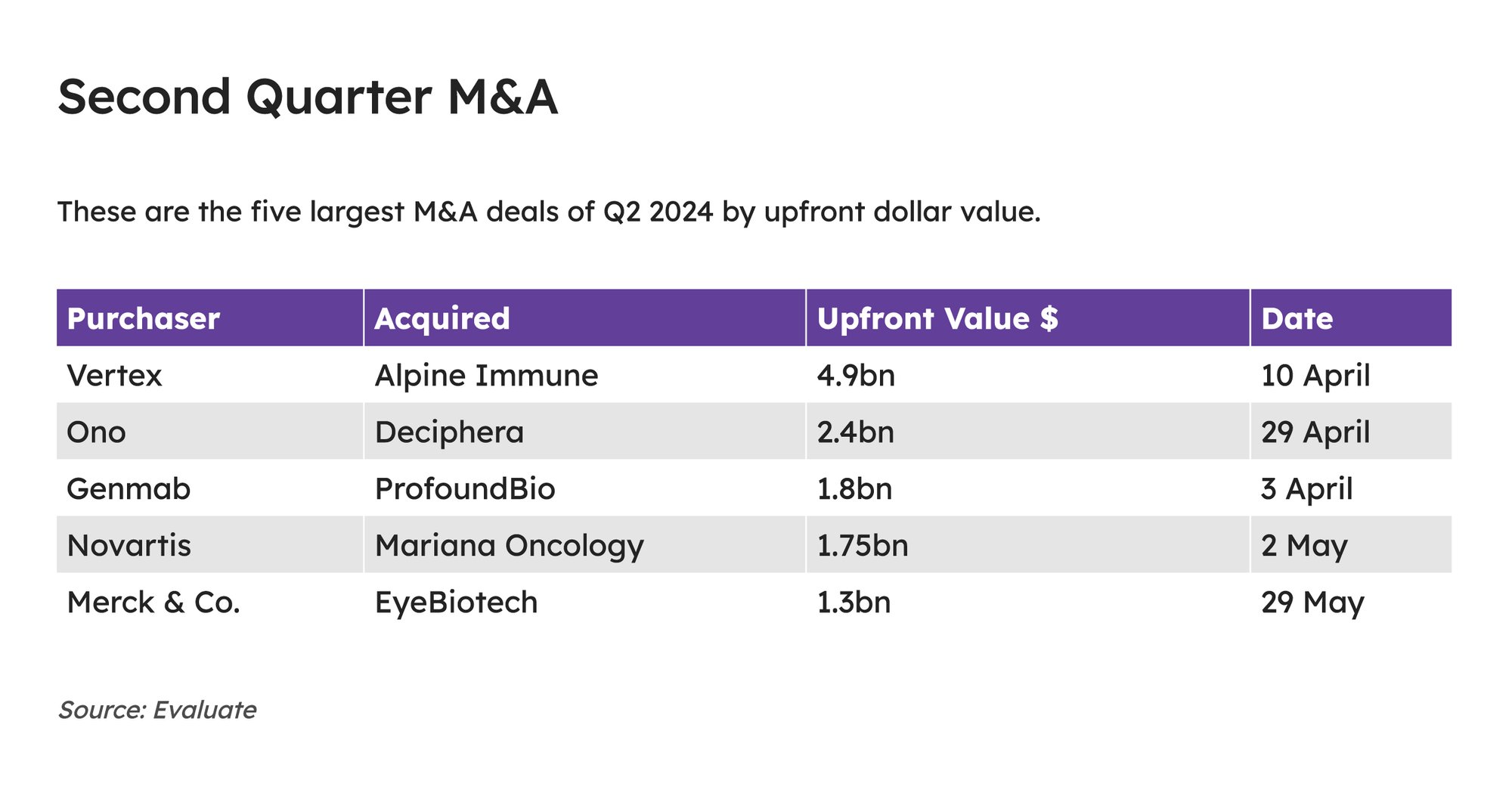

The main reason for the disparity in total value was that Q1’s M&A activity was headlined by Novo Holdings’ product supply-driven acquisition of the contract manufacturing and development organisation Catalent, Inc for $16.5bn, nearly four-times the size of the quarter’s second-largest takeout (Gilead Sciences, Inc., CymaBay Therapeutics, Inc., $4.3bn), while the largest M&A deal of Q2 was Vertex Pharmaceuticals Incorporated’s $4.9bn purchase of Alpine Immune Sciences Inc.

M&A deal volume also declined during the second quarter, down 42% from the first quarter. The 34 deals made for the lowest total recorded in nearly four years – at the height of the COVID-19 pandemic, Q3 2020 saw 33 total M&A transactions.

By contrast, the aggregate value in Q2 2024 was less of a departure from recent activity, continuing a drop-off in value seen since the end of 2023. The nearly $20.4bn in spending recorded during Q2 2024 was lower than Q1 ($36.57bn) and lower than Q2 2023 ($29bn) – but it is not the lowest quarter in recent years, following the pandemic.

While the total of eight deals with upfront value of $1bn or more increased by one from Q1 2024, a significant difference was seen compared with deal activity in late 2023, when fourth-quarter activity produced two deals valued at more $10bn and four valued at $7bn or higher. By contrast, the larger M&A deals agreed to during Q2 2024 included a cluster of five takeouts valued at between $1.75bn and $1.1bn up front during the month of May. So even though Vertex/Alpine Immune at $4.9bn was small as the largest deal of the quarter, it still dwarfed a majority of the acquisitions recorded during Q2.

The buyers of companies valued at $1bn or higher during Q2 2024 comprised a mix that included large pharma firms like Novartis AG, Merck & Co., Inc. and Johnson & Johnson, Japanese biopharmas Ono Pharmaceutical Company, Ltd. and Asahi Kasei Pharma Corporation, as well as established biotechs such as Biogen, Inc., Vertex and Genmab A/S. Novartis and J&J each recorded its second M&A transaction valued at $1bn or greater during the quarter, after each announced one such deal during the first quarter.

NOVARTIS, J&J CONTINUE 2024 M&A EFFORTS

After Novartis committed $2.91bn in February to acquire Germany’s MorphoSys AG and its Phase III BET inhibitor pelabresib for myelofibrosis, the Swiss pharma made another significant play in the oncology space with its $1.75bn bid on 2 May for Mariana Oncology. Not yet closed, Novartis’s offer for privately held Mariana is intended to increase the pharma’s presence in the burgeoning radiopharmaceutical market following its 2018 acquisition of Endocyte, Inc. The deal also continued a run on radiopharmaceutical firms in recent years, including AstraZeneca PLC’s $2bn acquisition of Fusion Pharmaceuticals Inc. in March.

J&J, which paid $2bn up front for antibody-drug conjugate (ADC) specialist Ambrx, Inc. in January, made another big splash during Q2, agreeing on 28 May to pay $1.25bn to pick up Numab Therapeutics AG’s Phase II-ready bispecific antibody NM26 for atopic dermatitis. Technically, that deal became an M&A transaction rather than an asset sale as Numab is packaging the antibody into a subsidiary called Yellow Jersey Therapeutics, which J&J will absorb.

KEY TAKEAWAYS

Both M&A volume and valuations declined from the first quarter of 2024 to the second quarter, according to data compiled by Evaluate.

Deal volume was the lowest seen in the biopharma sector since the height of the COVID-19 pandemic, while total value declined 42% compared to Q1 activity.

Deep-pocketed players continued with billion-dollar-plus bolt-on deals, however, with eight recorded during the quarter, up from seven in Q1.

The deal was J&J’s second acquisition of the month, following the 16 May takeout of Proteologix for $850m, gaining the privately held biotech’s preclinical PTX128, an antibody targeting both IL-13 and the thymic stromal lymphopoietin (TSLP) pathway, which is thought to offer therapeutic potential in moderate-to-severe AD and asthma.

Meanwhile, Merck offered $1.3m up front on 29 May to acquire Eyebiotech Limited in a deal that ultimately could be worth roughly $3bn to the UK biotech’s shareholders. The New Jersey-headquartered big pharma apparently liked the tri-specific antibody RESTORET (EYE103) enough to place a big bet on a candidate that has shown promise in a Phase Ib/IIa study in patients with diabetic macular oedema and neovascular age-related macular degeneration.

The quarter’s largest deal, Vertex’s purchase of Alpine Immune, was driven by a focus on autoimmune disease, which also served as the driver of Biogen’s 22 May offer for Human Immunology Biosciences, Inc. (HI-Bio). Anti-CD38 candidate felzartamab’s potential in primary membranous nephropathy, where it may be ready to move into Phase III, encouraged Biogen to offer $1.15bn up front plus earnout potential up to $650m for the San Francisco biotech. The deal closed on 2 July.

Genmab, meanwhile, bid $1.8bn on 3 April for Chinese ADC specialist ProfoundBio (Suzhou) Co., Ltd., a deal that closed on 21 May. The latest big deal driven by increasing competition in the cancer ADC field will bring Genmab three clinical-stage ADCs as well as one preclinical candidate for both solid and haematological cancers.

The quarter’s second-largest acquisition by upfront value, Ono’s $2.4bn takeout of Deciphera Pharmaceuticals, Inc., also was driven by cancer, with the Waltham, MA-based firm bringing its Japanese suitor a marketed gastrointestinal stromal tumour product, Qinlock (ripretinib), as well as vimseltinib, a Phase III CSF1R inhibitor that is slated to be filed for US approval this year in tenosynovial giant cell cancer.

Ono’s Japanese peer Asahi Kasei, meanwhile, made a bid valued at approximately $1.1bn on 28 May to purchase Calliditas Therapeutics AB on the strength of its approved kidney drug Tarpeyo (budesonide) as well as pipeline of candidates for orphan indications in renal and hepatic disease.