First Quarter M&A Activity Rose On The Strength Of Three Deals

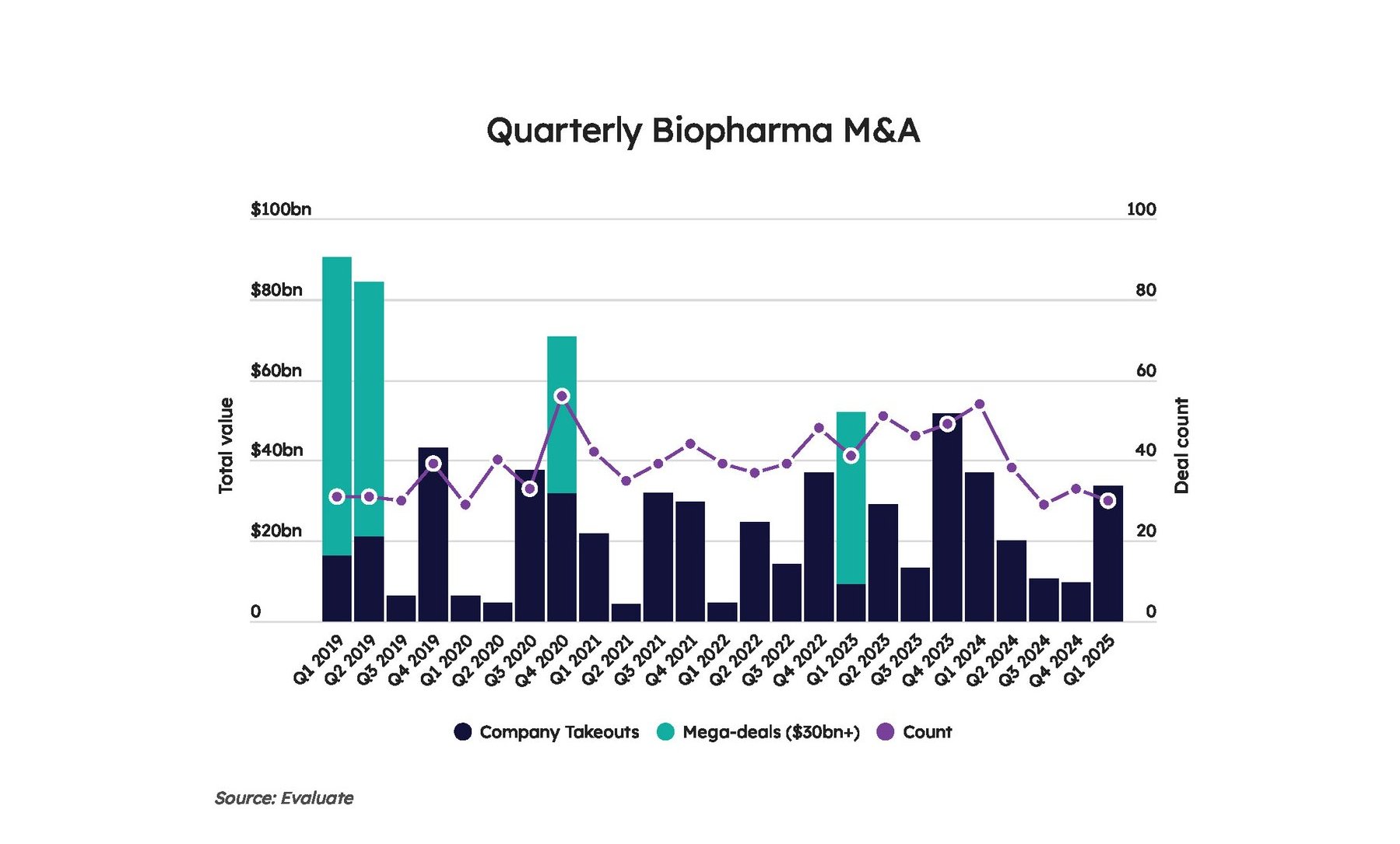

The biopharma sector made acquisitions with total potential value of $33.6bn during Q1, up substantially from the $9.5bn of Q4 2024, according to data from Evaluate.

Merger-and-acquisition activity in the biopharmaceutical sector had almost nowhere to go but up in the first quarter of 2025, following a historically low quarter in terms of total potential deal value in Q4 2024, and it did just that according to data compiled by Evaluate.

By the numbers, the first quarter dwarfs the previous quarter, with a total value of $33.6bn compared to $9.5bn for Q4. At roughly $33.55bn, total potential deal value during Q1 2025 was about 9% lower than the total for Q1 2024, last year’s most productive M&A quarter with total valuation of $36.95bn spread out over 54 deals, also the highest deal-volume quarterly total of 2024.

However, without the three largest deals in Q1, the balance looks similar to that of Q4 – suggesting that without some sizeable outliers, the longer-term trend of smaller, bolt-on M&A trend remains in place for the sector. The biggest deal - Johnson & Johnson’s13 January acquisition of Intra-Cellular for $14.6bn – was the largest biopharma M&A in nearly two years.

Only one other buyout during Q1 brought a price tag of at least $1bn up front, while eight deals reached the $1bn threshold in total potential value, up considerably from three such deals during the last quarter of 2024.

Overall, Q1 2025 yielded 30 deals in which one biopharma firm acquired another, down slightly from the 33 recorded during the previous quarter, but total potential valuation increased by more 300%, thanks not just to J&J/Intra-Cellular but other deals that conferred relatively low upfront cash but promised significant earnout potential.

For example, Mallinckrodt paid just $80m up front to merge with Endo, but with a total potential value of $6.7bn, the transaction would have been the biggest biopharma M&A deal of 2024, Vertex’s $4.9bn buyout of Alpine Immune, by a margin of roughly $1.8bn.

Those two deals plus Novartis’s 11 February agreement to acquire one-time spinout Anthos Therapeutics for $925m up front and total potential value of $3.075bn account for the monetary difference between the M&A activity recorded during Q4 2024 and Q1 2025. For a variety of reasons, mainly the global economic uncertainty of Trump administration policies, economic risk-taking by biopharma companies in terms of M&A is expected to remained constrained for at least the near term.

There were eight Q1 M&A deals with total potential value of $1bn or more, though only one besides J&J/Intra-Cellular included an upfront payment in the billions – GSK’s 13 January acquisition of IDRx for $1.15bn overall, including exactly $1bn in cash. GSK closed the buyout centered on Phase I KIT inhibitor IDRX-42 for gastrointestinal stromal tumors (GIST) on 24 February.

There were eight Q1 M&A deals with total potential value of $1bn or more

Purchaser

Acquired

Upfront Value

Date

Johnson & Johnson

Intra-Cellular

$14.6bn

13 Jan.

GSK

IDRx

$1bn

Novartis

Anthos

$925m

11 Feb.

AstraZeneca

EsoBiotec

$425m

17 Mar.

Taiho

Araris

$400m

While Q4 2024’s total value of roughly $9.5bn made for the lowest quarterly aggregate value in M&A since the first quarter of 2022, the Q1 aggregate value was the highest since the nearly $37bn recorded during the first quarter of 2024, according to Evaluate. It also was the fifth-highest quarterly total during this decade, which could offer rationale for some optimism.

The eight deals during the quarter with total potential value of $1bn or greater comprised total potential value of $31.2bn, or approximately 93% of all biopharma M&A value recorded during Q1. The other deals with total potential value of $1bn or higher were:

As one of three $1bn-plus deals announced on 13 January, at the start of the annual J.P. Morgan Healthcare Conference, which typically coincides with some notable business development activity, Lilly agreed to pay up to $2.5bn for precision oncology firm Scorpion Therapeutics. The deal will bolster Lilly’s breast cancer portfolio with the Phase I/II PI3Kα inhibitor STX-478 and then spin out much of Scorpion’s personnel and remaining pipeline into a new precision cancer outfit in which Lilly will hold a minority stake. Lilly did not disclose what portion of the $2.5bn price tag was upfront cash and how much was tagged to potential earnouts for Scorpion shareholders.

Otsuka’s Taiho Pharmaceutical subsidiary committed $400m up front on 17 March to acquire privately held Araris Biotech, which uses its AraLinQ technology platform to design antibody-drug conjugate (ADC) therapies for cancer that it said can offer greater safety and anti-tumor effect than competing ADCs. With milestone payments of up to $740m, the deal could be worth up to $1.14bn to Araris’s shareholders.

Lantheus Holdings committed $250m up front on 28 January to buy the radiopharmaceuticals discovery, commercialization and contract development and manufacturing services company Evergreen Theragnostics in a transaction with a total potential value of $1.003bn. That deal followed just weeks after Lantheus paid $350m up front with potential earnouts of up to $400m to acquire Life Molecular Imaging, a developer of positron emission tomography radiopharmaceutical diagnostics.

AstraZeneca made a big investment in in vivo cell therapies on 17 March by paying $425m up front to buy Belgium’s EsoBiotec. The deal has a total potential value of $1bn. EsoBiotec claims that its off-the-shelf chimeric antigen T-cell (CAR-T) technology platform can provide an alternative to autologous CAR-T therapeutics with intravenous delivery and no need for immune cell depletion.