Normality Reasserts Itself For Biotech IPOs

The highs of the COVID-19 era, and the lows that supplanted it, are beginning to fade.

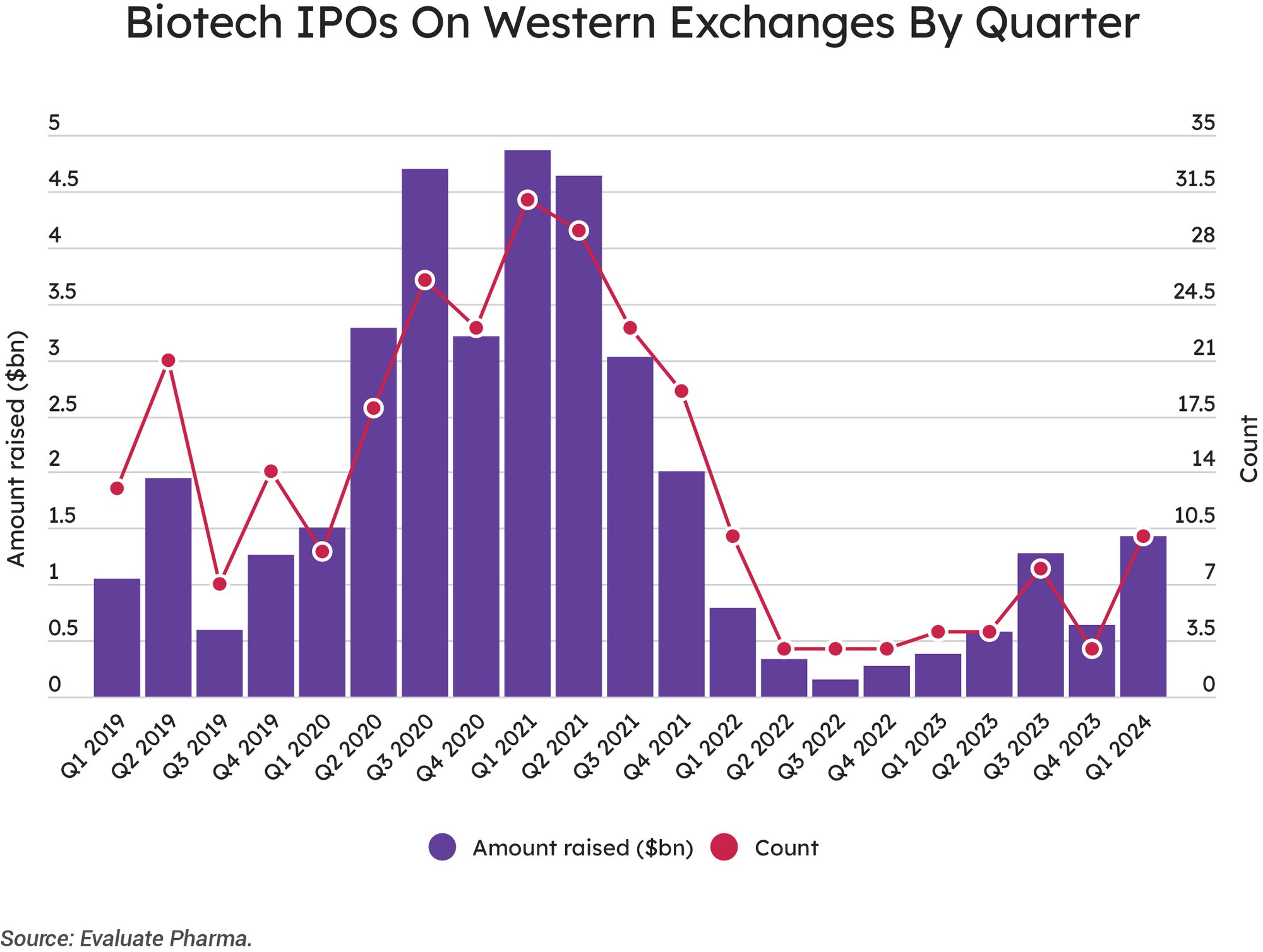

It is too early to say that biotech IPOs are back. But the showing in the first quarter of this year is cheering: more flotations got away since the first quarter of 2022, according to Evaluate Pharma, and more money was raised since the period before that.

But several of these groups have seen their share price slip since their debuts. While investors are certainly keen, the pressure is on for these newly public enterprises.

Key Takeaways

10 biotechs floated on Western exchanges in Q1 2024

They raised a total of $1.4bn

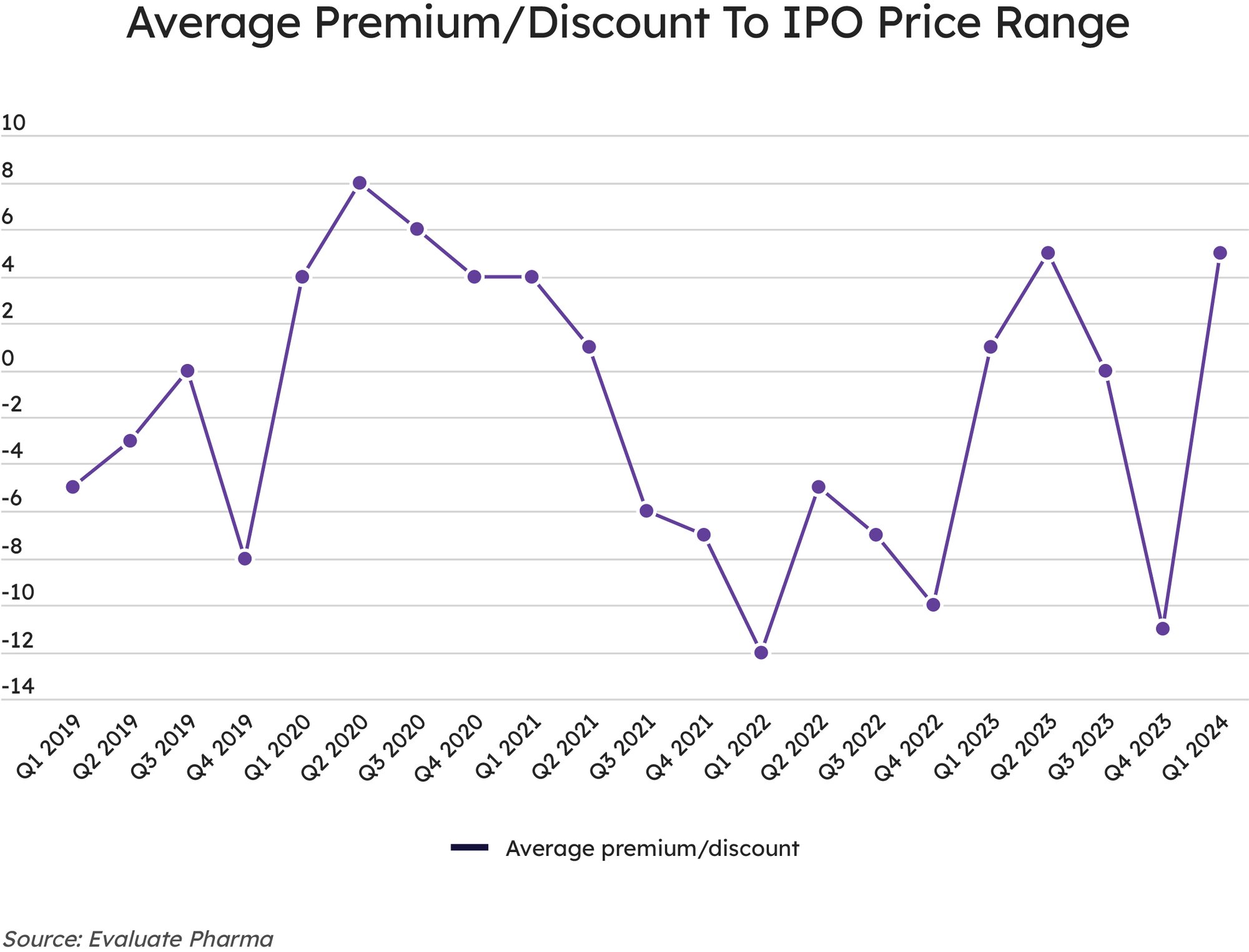

They did so at an average premium of 5% to their preannounced pricing

The analyses below track IPOs of companies developing prescription drugs, cell and gene therapies on Western stock exchanges; Asian and other markets are excluded. It also excludes spin-outs, so as to concentrate on younger companies seeking growth capital.

In the first three months of 2024 10 biotechs floated on Western exchanges, raising a total of $1.4bn. In some ways this looks like a regression to the mean. In 2020 the biotech IPO market took off like a rocket as the COVID-19 pandemic showed investors how vital the sector is, and how much money could be made by groups with successful technologies. As this trend wound down towards the end of 2021, however, there was far less activity, largely in reaction to the preceding frenzy. Now this lull, too, may be passing.

The $1.4bn raised in the past quarter is the best showing since the end of 2021– but compared with that period, the recent deals are larger. The average IPO in Q4 2021 raised $105m, whereas the deals in Q1 2024 raised an average of $143. The first deal of this year was also the largest: CG Oncology, Inc. raised $380m on the NASDAQ at the end of January.

It is not just deal sizes that are getting bigger. Investors’ eagerness seems to be expanding too. The groups that went public in the first quarter were able to price their offerings at a 5% premium, on average, to the initial prices proposed by bankers. Kyverna Therapeutics managed to price its $319m IPO at an astonishing 22% premium.

The average figure is a huge uptick from the final period of 2023, when listing companies were forced to take a haircut of around 11%, on average, to get their deals away.

GREAT EXPECTATIONS

Once they were away, however, they disappointed. Only three of the companies that have gone public in 2024 were trading above their IPO values as of mid-April.

This may just be a matter of managing expectations. For too many companies, the game plan is simply to get listed, raising all they can in upsized offerings with premium pricing. But this creates huge pressure for these new issues to perform. If groups planning an IPO were to inculcate more reasonable expectations of how their technology might do in the months and years after the float, they could perhaps keep their share price more buoyant.

Whether the uptick in the number of deals and the cash raised will continue throughout the year to come is hard to call. The track record of these freshly floated drug developers will be a major influence on investor appetite in the coming months. Currently only three private biotechs are currently known to have filed to float – Lirum Therapeutics, Jyong Biotech and Aprinoia Therapeutics, Inc. – and they are seeking relatively modest sums.