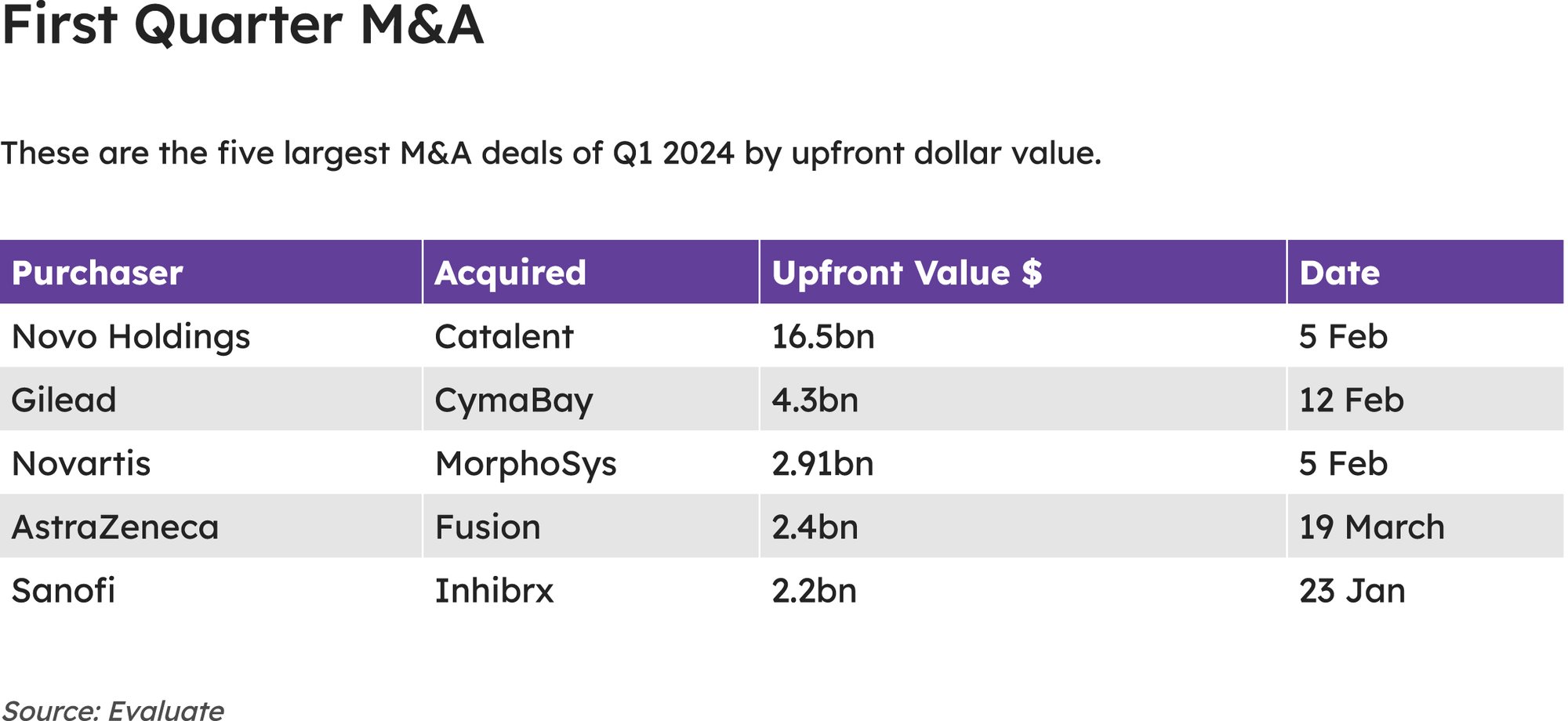

Q1 2024 Posts Big M&A Total Led By Novo Holdings’ Catalent Takeout

The $16.5bn deal, intended to increase Novo Nordisk’s production of semaglutide-containing products, led a $36bn-plus quarter for M&A transactions, according to Evaluate.

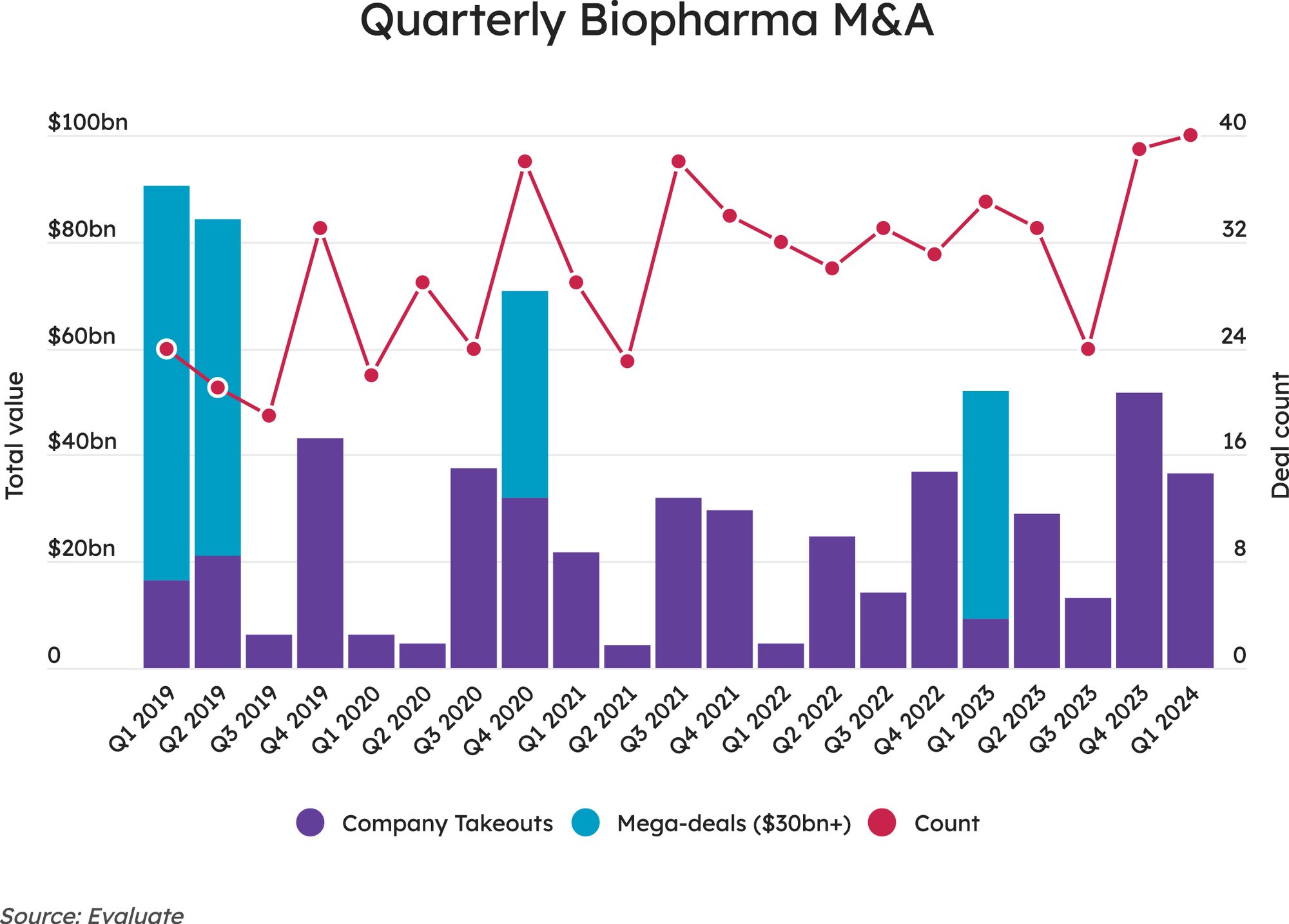

Merger-and-acquisition activity during the first quarter of 2024 was not likely to match the bustling pace of Q4 2023, when the aggregate dollar amount committed to acquisitions topped $52bn and nearly tripled the spend recorded during the previous quarter, but the first quarter did see strong M&A activity, with more than $36bn in total spend. Seven biopharma acquisitions valued at more than $1bn up front were recorded during Q1, including one above the $10bn mark.

All told, the $36.46bn in M&A upfront spending during the quarter was the fifth-highest quarterly total that Evaluate recorded since the beginning of 2020. And the Q1 data may augur a big M&A year overall for the biopharma sector, as the Q1 total dwarfed the below-$10bn totals seen in the first quarter of 2020 and 2022, and was significantly higher than the $22bn-plus recorded in Q1 2021.

Driving the quarterly total was Novo Holdings’ $16.5bn takeout of New Jersey-based contract development and manufacturing organisation (CDMO) Catalent, Inc., a deal intended to help Novo Nordisk A/S maintain its leading position in type 2 diabetes and obesity by increasing production of its mega-blockbuster semaglutide, the GLP-1 agonist contained in diabetes products Ozempic and Rybelsus and obesity drug Wegovy.

KEY TAKEAWAYS

The first quarter of 2024 produced 48 M&A deals with an aggregate upfront value of more than $36bn, Evaluate reported, the fifth-largest quarterly total since the start of 2020.

Leading the way was Novo Holdings’ $16.5bn acquisition of Catalent, which will bring Novo Nordisk increased production capacity for Ozempic and Wegovy.

AstraZeneca made two of the quarter’s potential $1bn-plus deals in acquiring Fusion Pharmaceuticals and Amolyt.

As part of the transaction, Novo Nordisk is paying $11bn to obtain three Catalent manufacturing sites – two in Europe, one in the US – to increase fill-finish capacity for semaglutide-containing products, for which the Danish pharma has been struggling to meet demand. Ozempic yielded $14bn in sales during 2023, while Wegovy brought in $4.36bn.

The rest of Q1’s M&A deals were significantly smaller in size, resulting in a reduced aggregate total from Q4. There were 48 M&A deals in Q1, up from 39 during the prior quarter, but the final three months of 2023 saw four acquisitions valued at more than $7bn and two above the $10bn threshold, although Novo Holdings/Catalent had a higher price tag than Bristol Myers Squibb Company’s $14bn purchase of Karuna Therapeutics, Inc. and AbbVie Inc.’s $10.1bn buyout of ImmunoGen, Inc.

The quarter’s second-largest deal saw Gilead Sciences, Inc. bolster its liver disease holdings by paying $4.3bn for CymaBay Therapeutics, Inc. and its Phase III PPAR delta agonist seladelpar for primary biliary cholangitis. Announced on 12 February, the deal wrapped up quickly, closing on 22 March. Hayward, CA-based CymaBay filed a new drug application for the candidate in December, setting up an August approval date at the US Food and Drug Administration.

If seladelpar obtains US approval for PBC, it will compete in the second-line treatment setting with Alfasigma S.p.A.’s established Ocaliva (obeticholic acid), an FXR agonist that has been on the market for PBC since 2016 but which presents a mixed safety/tolerability profile. Seladelpar also is under review by the European Medicines Agency for approval to treat PBC.

The first quarter saw four other M&A transactions valued at between $2bn and $3bn – there were seven acquisitions with upfront value of at least $1bn, while two other deals had potential total value of $1bn or more, but the upfront payment was either below that threshold or not reported.

ASTRAZENECA MADE TWO BUYOUTS DURING Q1

Novo Nordisk pledged up to €1.03bn (about $1.11bn) to acquire Germany’s cardiovascular-focused Cardior Pharmaceuticals GmbH on 25 March, but did not break down how much of that amount would be in upfront cash and how much in potential earnouts. Cardior has oligonucleotide candidate CDR132L in Phase II, trying to demonstrate ability to halt and partially reverse cellular pathology in patients with heart failure with reduced ejection fraction.

AstraZeneca PLC purchased Amolyt Pharma for $800m up front and potential $1.05bn total on the strength of Phase III hypoparathyroidism candidate eneboparatide on 14 March.

The Amolyt deal was AstraZeneca’s second substantial M&A transaction during Q1 – it also paid $2bn on 19 March, less than a week later, for its partner in radiopharmaceutical alpha emitter development Fusion Pharmaceuticals Inc. Fusion, which has been working with AstraZeneca since 2020 on FPI-2265, a radiopharmaceutical candidate for prostate cancer, and can realise an additional $400m in milestones under the sales agreement. (See chart on page 3.)

The deal was the third $1bn-plus transaction since the start of 2023 in which a large pharma company acquired a biotech specialising in radiopharmaceuticals. BMS bought RayzeBio, Inc. in December for $4.1bn, the same month in which Eli Lilly and Company committed $1.4bn for POINT Biopharma Global Inc.

In potentially the third-largest deal of Q1, Novartis AG made a $68-per-share offer on 6 February for Germany’s MorphoSys AG, a deal valued at an estimated $2.91bn and expected to close during the first half of 2024. MorphoSys, which announced that the proposed deal cleared US Federal Trade Commission review on 22 March, has reported out multiple Phase III studies of myelofibrosis candidate pelabresib and asserts that the BET inhibitor is approvable on the totality of data despite some mixed results in those trials.

January, meanwhile, saw a trio of $1bn-plus M&A deals, including Sanofi’s $2.2bn bid on 23 January for US rare disease specialist Inhibrx, Inc. The biotech’s AAT-fc fusion protein INBRX-101 is in Phase II for alpha-1 antitrypsin deficiency.

On 8 January, Johnson & Johnson announced that it would pay approximately $2bn to acquire Ambrx Biopharma, Inc. and its pipeline of cancer antibody-drug conjugate (ADC) therapies, most of which are being developed for solid tumours. The following day, GSK plc committed $1bn up front in a potential $1.4bn deal to acquire Aiolos Bio, which is developing AIO-001, an antibody against the thymic stromal lymphopoietin pathway, which might be positioned in asthma against AstraZeneca and Amgen, Inc.’s Tezspire (tezepelumab).