Orphan Pipeline: CAR-Ts and Gene-Edits

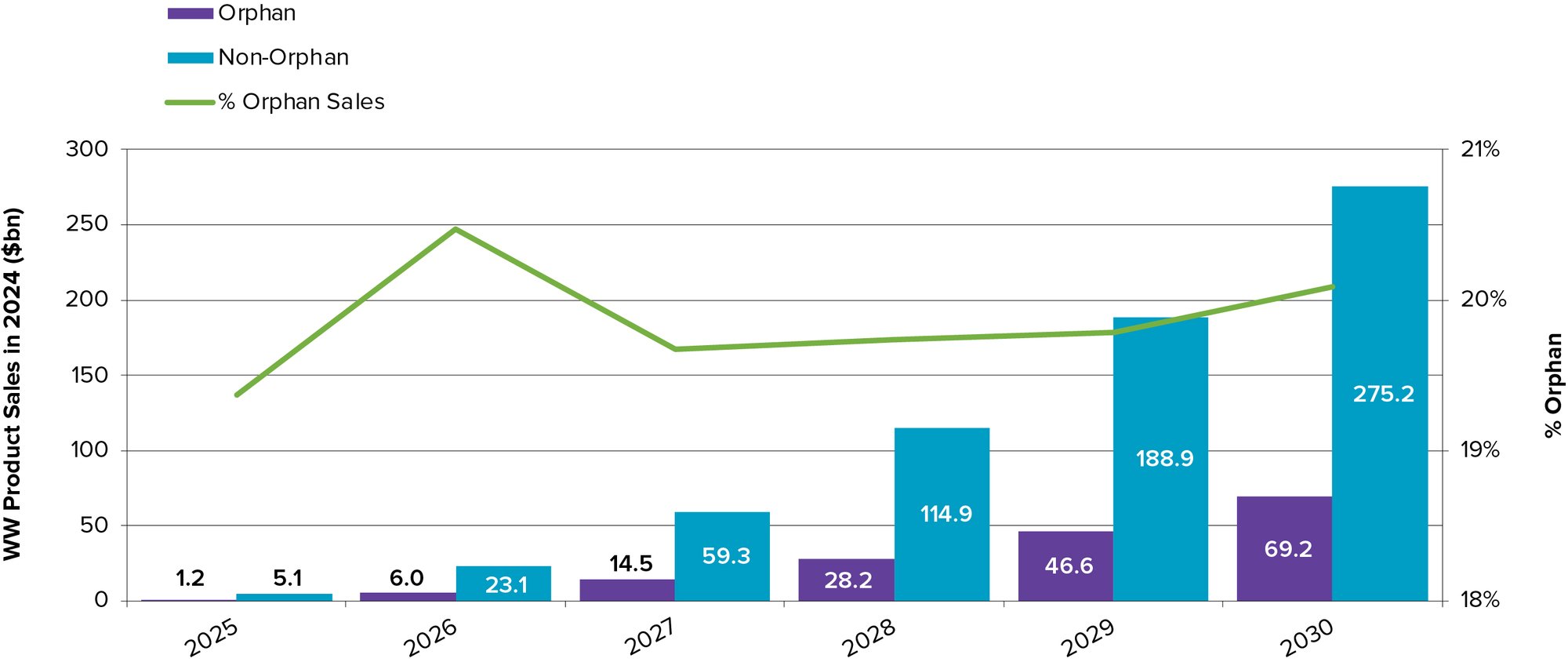

Orphan drug candidates will make up 20% of global pipeline forecast sales over the rest of this decade – in line with the category’s share of 2030 prescription pharmaceutical sales.

Worldwide Pipeline to 2030: Orphan vs. Non-Orphan

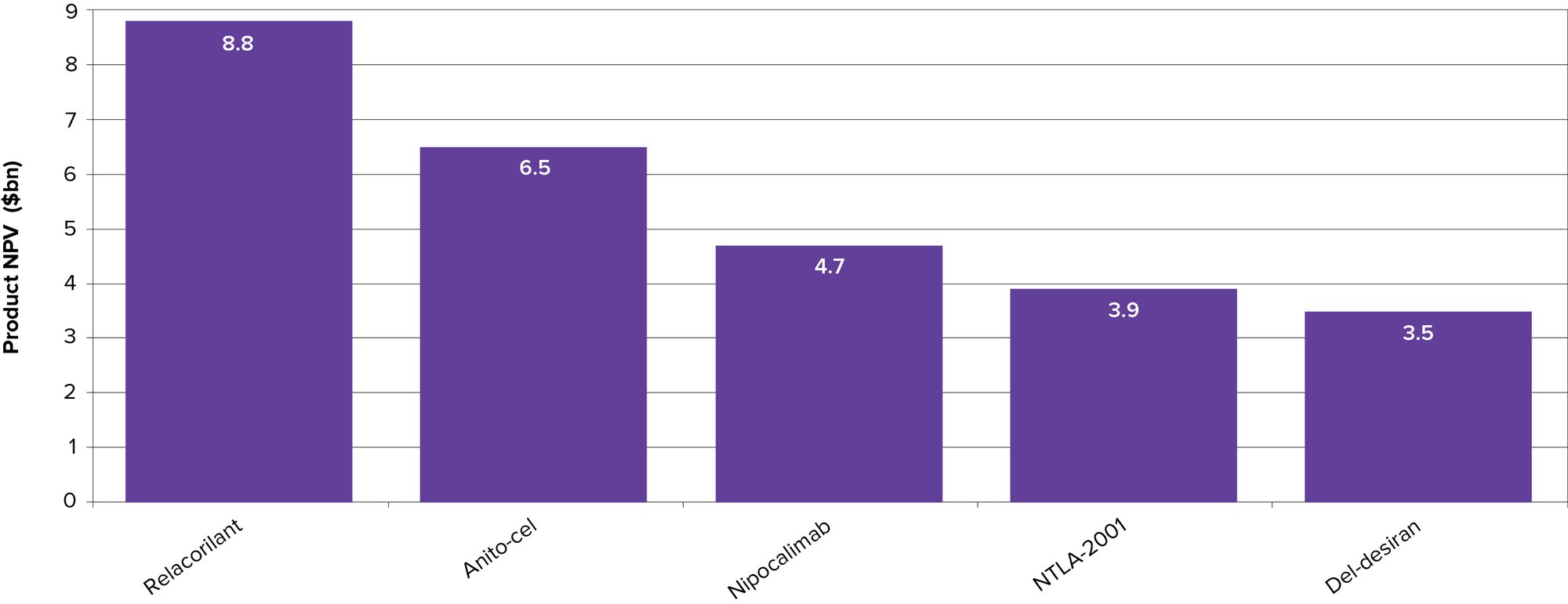

Next up in the orphan pipeline: look out for Gilead Sciences / Arcellx’s Phase 3 CAR-T cell therapy anito-cel, which is coming for Carvykti. Forecast 2030 sales of almost $1.4 billion contribute to a net present value (NPV) approaching $6.5 billion.

J&J’s immunotherapy nipocalimab, filed for MG, is currently third biggest with anticipated 2030 sales topping $1 billion and a net present value of over $4.5 billion. It’s also in clinical testing for rheumatoid arthritis and lupus (alongside other rare diseases), so may not stay niche for long.

Top 5 Orphan Drugs in 2030 (Phase III/ Filed) by NPV

Number one placed relacorilant, a selective cortisol modulator sponsored by Corcept Pharmaceuticals, was filed at FDA in December 2024 for hypercortisolism (Cushing’s Syndrome) and is also in the clinic for ovarian and prostate cancer. Oncologists have long observed that stressed patients have worse outcomes; this drug – if it works – would confirm that view, since it blocks the effects of the stress hormone cortisol.

Intellia’s NTLA-2001 (nexiguran ziclumeran) is the first drug to edit genes within the body and is in testing for both types of ATTR, cardiomyopathy and polyneuropathy, though an initial filing is expected in the smaller polyneuropathy (ATTR-PN) segment in 2028. Its NPV is close to $4 billion. Avidity Biosciences’ del-desiran makes up the last of the top five orphan R&D candidates based on NPV. Del-desiran, an antibody-conjugated siRNA molecule, is in Phase 3 trials for myotonic dystrophy type 1, a rare musculoskeletal disorder.

These future earnings estimates may include best-case estimates not fully adjusted for development risk. Still, the range of modalities and therapy areas represented by these highly-valued candidates may signal a weakening (if not, by any means, an end) of oncology’s overwhelming dominance and underscore an increasingly multi-modal pipeline.

The range of modalities and therapy areas represented by these highly-valued candidates may signal a weakening (if not, by any means, an end) of oncology’s overwhelming dominance.