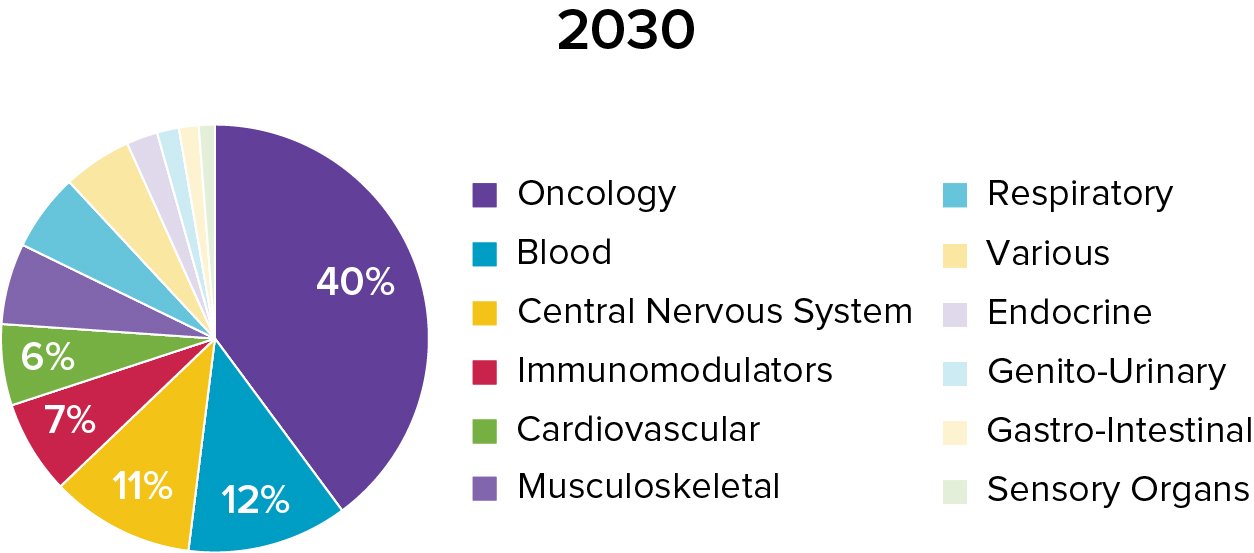

Blood Disorder and CNS Drugs in Cancer’s Shadow

Johnson & Johnson’s Darzalex-powered hematology engine drives oncology’s continued dominance of the orphan roster, with four of the top ten biggest drugs by 2030 forecast sales.

J&J’s engine also includes two other blood cancer treatments, Carvykti and Tecvayli, ranked fifth and fifteenth respectively. These highlight emerging modalities’ growing stature among the biggest orphans. CAR-T therapies like Carvykti (cilta-cel, first approved in 2022) have been slow to gain commercial and clinical traction and are out of favor with investors as a result. But forecasts suggest they will gain prominence as manufacturing technologies improve and long-term outcomes data accumulate. Tecvayli is a T-cell engaging bispecific antibody, another popular new-generation format. The FDA has approved seven new bispecifics in the last two years, and dealmaking remains healthy around these and other multi-specific antibodies.

CAR-T therapies like Carvykti have been slow to gain commercial and clinical traction and are out of favor with investors as a result.

Bruton’s Tyrosine Kinase (BTK) inhibitors Brukinsa and Calquence, in 8th and 9th place respectively, also contribute to blood cancer’s strong showing; both are approved for chronic lymphocytic leukemia and Mantle cell lymphoma. Brukinsa in March 2024 became the first US-approved BTK inhibitor for follicular lymphoma, with sponsor BeiGene showcasing the entry of China-founded companies into global rankings. [See Box: Enter China]

BeiGene, listed in Shanghai, Hong Kong and on Nasdaq, recently re-named itself BeOne Medicines in an apparent bid to shed its association with China. But that country’s dominance within global overall R&D rankings is undeniable: four of the top 20 biggest R&D engines are housed within Chinese biopharma, according to Citeline’s Pharmaprojects database. Those engines are increasingly fast and efficient, and provide a cost-effective asset-source for Western pharma: almost a third of all pharma licensing deals involve a Chinese biotech, per Stifel. Lackluster local capital markets also force Chinese innovators to seek investment and partnerships elsewhere; this trend – all too familiar to European biotechs – is unlikely to narrow the huge gulf between Chinese biopharmas’ commercial footprints and the global revenues enjoyed by their US and large European counterparts (see Biopharma’s R&D engine and the importance of looking east).

Blood disorders are the next biggest orphan drug category, driven largely by Roche’s hemophilia drug Hemlibra (emicizumab) and Bristol Myers Squibb’s Reblozyl (luspatercept) for beta thalassemia and myelodysplastic syndrome (MDS)-associated anaemia.

Third-placed CNS is boosted by Alnylam’s Amvuttra (vutrisiran), set to reach almost $5.5 billion in 2030 sales if it receives its anticipated expansion into transthyretin amyloid cardiomyopathy (ATTR-CM); the FDA’s action date is in March 2025. ATTR is crowded, though: Amvuttra will face competition from Pfizer’s established Vyndaqel/Vyndamax (tafamidis), BridgeBio’s newcomer Attruby, and, perhaps, from Intellia’s gene-editing Phase 3 nexiguran ziclumeran.

CNS gets a further hike from Roche/Genentech’s spinal muscular atrophy drug Evrysdi (risidiplam) whose almost-$3 billion 2030 sales place it just within the top 20. FDA in February 2025 approved a tablet form of Evrysdi, previously available only as an oral solution.