Move Over, Oncology…

MOVE OVER, ONCOLOGY: CNS AND IMMUNOMODULATORS RISE

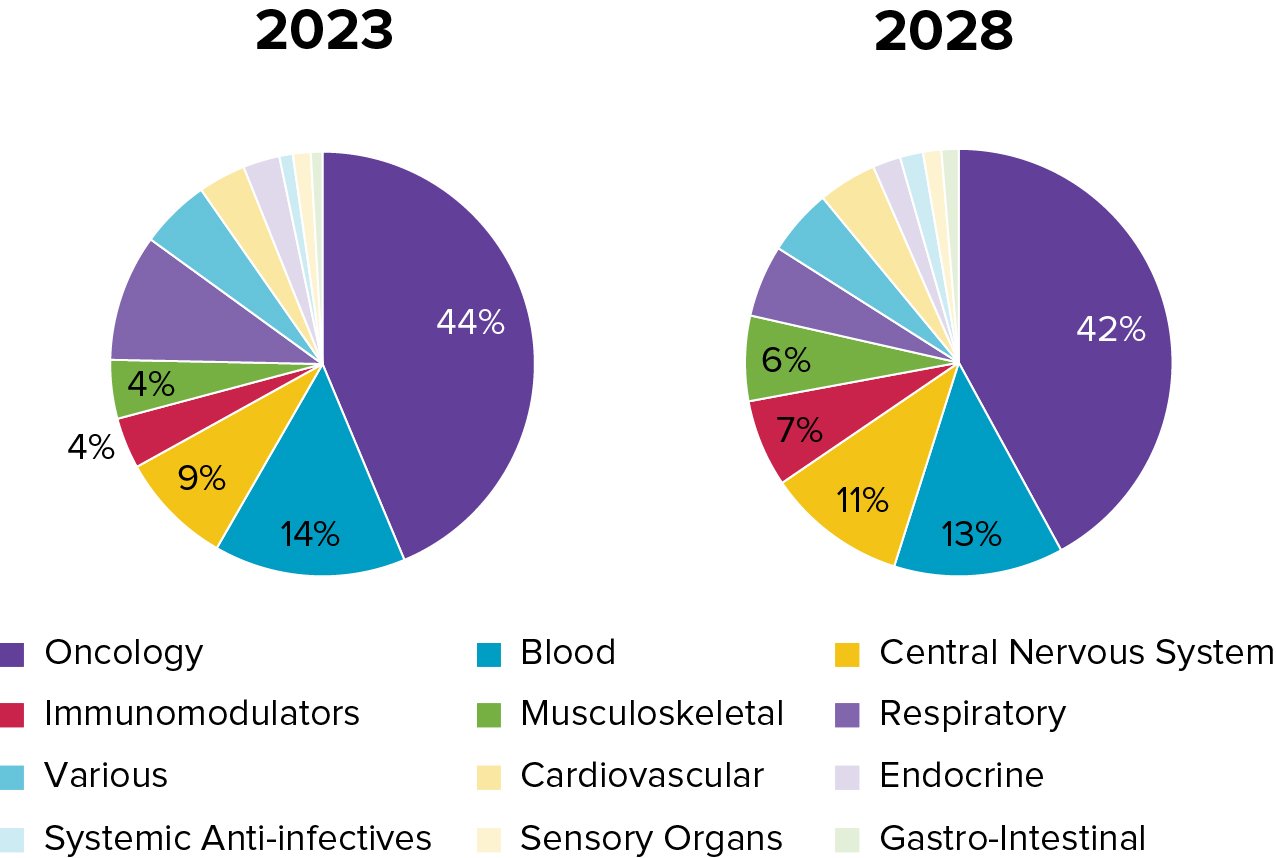

Oncology still leads the therapy area rankings for orphan drugs. But its share will fall over the next five years – mirroring the broader slow-down in orphan vs non-orphan growth. Oncology has come off the boil as precision medicines tackling ever-narrower genetic mutations run out of road commercially (druggable ‘pan-cancer’ mutations are elusive), and as CAR-T therapies continue to face challenging administration logistics.

CNS orphan drug sales will more than double between 2023 and 2028, by which time they’ll make up over 10% of orphan sales by value. This reflects broader industry interest in this once-neglected area: witness AbbVie’s $8.7 billion acquisition of CNS-focused Cerevel or Bristol Myers Squibb’s $14 billion Karuna deal, both announced in December 2023. Immunomodulators – another popular space, as per Merck’s $10.8 billion Prometheus Biosciences deal last April – are also grabbing a bigger share of the orphan pie. They will almost triple, reaching 7% in 2028, up from 4% in 2023.

WW Annual Sales ($bn)

Therapeutic Category

2023

2028

CAGR

Oncology

68.3

112.8

11%

Blood

22.8

34.4

9%

Central Nervous System

13.5

28.4

16%

Immunomodulators

6.1

17.7

24%

Musculoskeletal

7.0

17.3

20%

Respiratory

15.1

14.6

-1%

Various

8.3

10%

Cardiovascular

5.7

11.9

Endocrine

4.4

5%

Systemic Anti-infectives

1.6

4.7

Sensory Organs

2.1

3.7

12%

Gastro-Intestinal

1.4

3.5