The Orphan Pipeline – The ‘Vanza Triple’ Dominates

VERTEX’S ‘VANZA TRIPLE’ DOMINATES ORPHAN PIPELINE, AFTER SOTATERCEPT APPROVAL

Vertex’s Phase 3 VX-121 or “vanza triple” for cystic fibrosis – a once daily treatment that combines new molecule vanzacaftor with tezacaftor and deutivacaftor – tops the pipeline in net present value (NPV) terms. But it has done so only since March 26, 2024, when Merck’s pulmonary arterial hypertension (PAH) drug sotatercept, with an NPV of close to $9 billion, was approved by FDA at Winrevair, removing it from the pipeline rankings. Winrevair’s 2028 projected sales of just under $2 billion don’t make the top ten marketed orphans, but the activin signalling inhibitor is the first approved biologic for PAH, may be disease-modifying, and is in late-stage trials for several related indications. Merck acquired sotatercept via its 2021 Acceleron acquisition and owes sales royalties to Bristol Myers Squibb, which bought co-developer Celgene in 2019.

With over $1.2 billion in forecast 2028 sales and an NPV just shy of $6 billion, the “vanza triple” now overshadows the four next-biggest pipeline orphans, in part thanks to its high likelihood of approval: vanzacaftor is similar to already-marketed tezacaftor (one half of CF treatment Symdeko). It helps move the cystic fibrosis transmembrane conductance regulator (CFTR) protein to the cell surface where it can work more effectively. Deutivacaftor is designed to help keep the protein there for longer – it’s a tweaked version of another of Vertex’s marketed drugs, Kalydeco (ivacaftor).

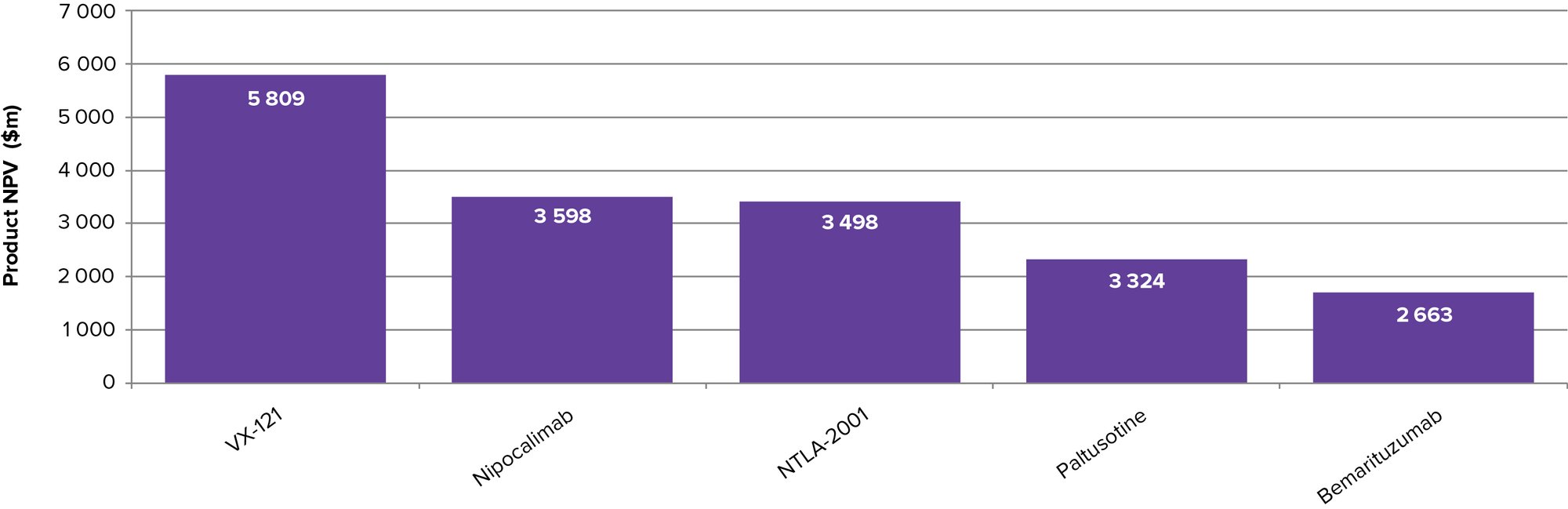

Top 5 Orphan Drugs in 2028 (Phase III/ Filed) by NPV

Worldwide Top 5 Orphan R&D Products based on NPV (Sales, NPV)

Rank

Product

Company

Phase (Current)

Therapeutic Category

Sales ($m) 2028

WW NPV

1

VX-121

Vertex Pharmaceuticals

Phase III

Respiratory

1,256

5,809

2

Nipocalimab

Johnson & Johnson

Immunomodulators

737

3,598

3

NTLA-2001

Intellia Therapeutics

Various

891*

3,498

4

Paltusotine

Crinetics Pharmaceuticals

Oncology

729

3,324

5

Bemarituzumab

Amgen

387

2,663

*NTLA-2001 sales in 2028 are Alliance Revenue through a co-promotion deal with Regeneron Pharmaceuticals.

The “vanza triple” will eat into sales of Vertex’s Trikafta – ranked second-most valuable orphan in 2028, with anticipated sales of almost $6 billion. But that’s the idea: Vertex will owe substantially lower royalties on the vanza triple than it does on those of Trikafta and its other cystic fibrosis drugs. (Royalty Pharma purchased Cystic Fibrosis Foundation Therapeutics’ royalty benefits in 2014 for $3.3 billion, in one of the largest pharma royalty deals ever). Vertex ran a Phase 3 head-to-head trial of the new combination versus Trikafta, showing non-inferiority on a primary efficacy endpoint and superiority on several secondary efficacy endpoints.

Vertex is adept at transitioning to new generation CF products: this is not a new gig. But there is novelty elsewhere in the orphan pipeline: Intellia’s CRISPR-Cas9 therapy for transthyretin amyloidosis with cardiomyopathy (ATTR-CM).

J&J’S NIPOCALIMAB HOLDS ON

Johnson and Johnson’s ‘pipeline-in-a-product’ nipocalimab holds its place in the top five despite the increasingly crowded MG market: alongside Argenx’s Vyvgart and UCB’s newly-approved duo, Amgen is gunning for an MG approval for Uplinza, acquired via its $27.8 billion Horizon acquisition in 2022. Uplinza’s Phase 3 completes in May 2024.

GENE EDITING DRUG TAKES BRONZE

Intellia’s third-placed drug uses a gene editing technology that has only just reached the US market, through the December 2023 FDA approval of Vertex’s sickle cell disease gene therapy Casgevy. Casgevy, developed with CRISPR Therapeutics, uses CRISPR-Cas9 to edit stem cells outside the body so they express the foetal version of haemoglobin. Intellia’s drug, developed with Regeneron, could become the first to edit cellular genomes within the body.

Intellia’s candidate may offer the first single-dose treatment for ATTR-CM, where it will compete with Pfizer’s Vyndamax/Vyndaqel, and, perhaps, with Alnylam’s next-generation RNA interference drug Amvuttra (vutrisiran). Amvuttra is already approved for ATTR with polyneuropathy; its highly-anticipated Phase 3 HELIOS B read-out in ATTR-CM has been delayed to mid-year following trial design changes. (FDA in 2023 rejected an expanded label in ATTR-CM for Alnylam’s older therapy

Onpattro (patisiran), despite a positive advisory committee vote.) BridgeBio’s acoramidis, a small molecule which works similarly to Vyndamax, is already under FDA review with a decision expected in November 2024.

Crinetics Pharma’s paltusotine, an oral somatostatin receptor type 2 (SSRT2) agonist for acromegaly and carcinoid syndrome is more convenient than alternatives. It generated positive Phase 3 data in patients pre-treated with somatostatin therapy; further data is due in treatment-naïve patients.

Amgen’s anti-fibroblast growth factor receptor 2 (FGFR2) antibody bemaritizumab is at number five in the NPV table, with $2.6 billion in potential value. It’s in Phase 3 for gastric and gastro-oesophageal junction cancers with over-expressed FGFR2 and sits alongside a host of other antibody-based therapies and combinations vying for sub-segments of the advanced GC market. Ocular toxicity is a concern for FGFR inhibitors.

Several of last year’s top five pipeline orphans were approved in 2023, including Sarepta’s gene therapy Elevidys. This therapy narrowly won FDA accelerated approval in age-restricted population of Duchenne’s muscular dystrophy sufferers; limited efficacy evidence made this another of 2023’s more controversial FDA decisions. Sarepta hopes to achieve full approval and a wider label this year for its $3.2 million therapy after submitting additional data, despite missing the primary endpoint in a recent Phase 3 trial. The therapy pulled in $200 million in its first six months on the market.