Orphan Drugs Are Losing Their Sparkle

Report written by Melanie Senior

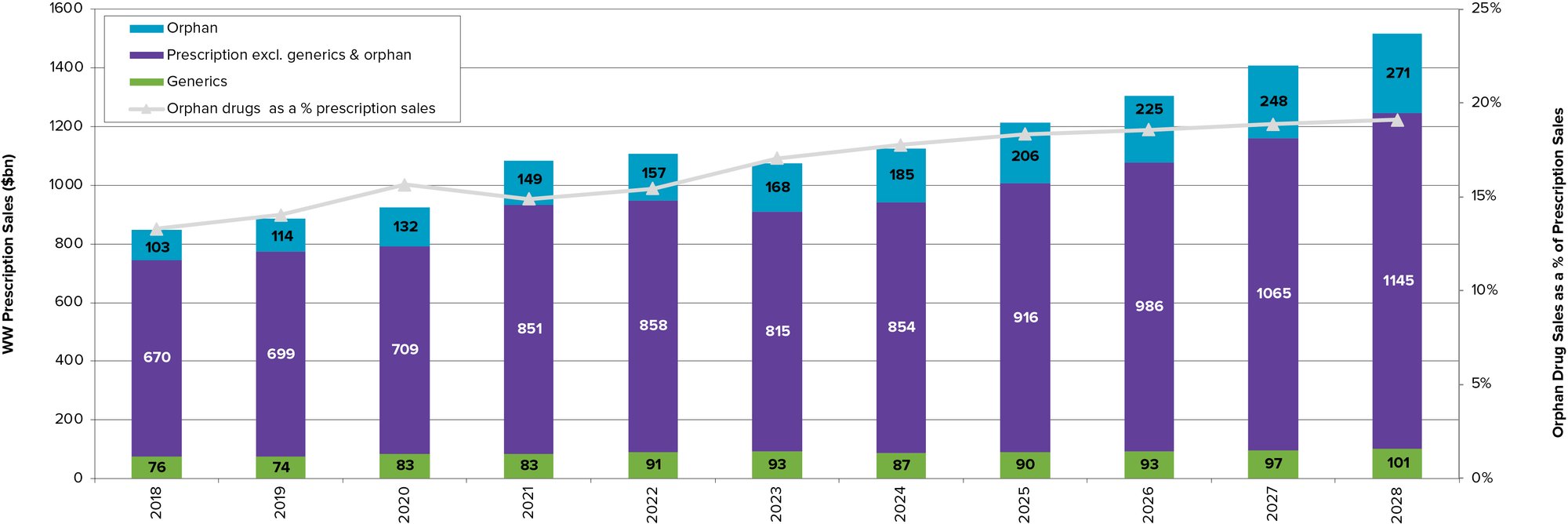

For more than a decade, orphan drugs’ growth has outpaced that of non-orphan prescription drugs. Niche products’ share of worldwide prescription drug sales by value has doubled over the last decade, from less than 10% in 2014 to almost a fifth today. Orphan drugs will generate $185 billion this year (2024), and close to $270 billion by 2028.

Worldwide Orphan Drug Sales & Share of Prescription Drug Market (2018-28)

But the growth gap is narrowing. The four percentage point gap in 2020-2025 compound annual growth rate (CAGR) for orphans vs non-orphans has shrunk to just over two percentage points for 2024-2028. Orphan drug sales growth averaged almost 11% annually in the ten years to 2023 yet will barely make double digits for the rest of this decade.

One reason is the blazing return of big drugs for big diseases. Obesity has captured the most attention, but emergent blockbusters across immunology and neurology are also drawing in R&D dollars as Big Pharma look to plug patent expiry holes. These markets’ sheer size more than compensates for the price premia commanded by niche drugs: the obesity market could reach over $100 billion by 2030, according to some estimates; so could that of neuroscience drugs targeting widespread conditions spanning anxiety, migraine, pain, depression, multiple sclerosis and Alzheimer’s.

Another reason for orphans’ relative slide may be more discerning payers. Many are prioritising more widespread health challenges facing their covered populations. They’re also baulking at orphans’ high prices – and may benefit from competitors’ crowding into some corners of the orphan drug market. These pricing pressures seep into R&D investment decisions.

ORPHANS ARE STILL HIGHLY ATTRACTIVEOrphans’ slowdown is relative, however. As the overall prescription drugs market continues to grow, so will that of drugs for rare diseases – even if their share remains steady.

High prices, small trials, well-defined populations and development incentives continue to buoy this important sector. So does regulators’ flexibility in offering expedited market access for drugs addressing unmet needs: almost 60%* of FDA’s new drug approvals in 2023 were orphan designated. (*includes CDER and CBER approvals) For the past five years, FDA’s share of orphan approvals has exceeded 50%.