The Competition

Novo and Lilly may have an early lead, but there’s still plenty of room to improve side effects, safety and quality of weight loss. Let’s look at the pipeline.

If incretins are famous for their weight loss, they are equally notorious for their side effects. Nausea, vomiting, diarrhoea and abdominal pain are very frequently suffered by users, and discontinuation rates remain high, even among the newer drugs in this class which purport to be more tolerable.

Long term outcome studies have, so far, ruled out any serious toxicity concerns for the class, the spectre of thyroid cancer notwithstanding. This risk, identified in preclinical trials and widely considered to be very small, is highlighted in a black box on both Wegovy and Zepbound’s US prescribing labels. This, and additional concerns around suicidal thinking, are not holding back demand, though deserve monitoring in the future.

Improved safety offers competitors a way into the obesity market. And not just on gastro-intestinal tolerability. Muscle loss is an area of focus, sparked by concern around how much weight loss is coming from muscle rather than fat.

The implication here is that people who regain weight after coming off an incretin could be left with a worse body composition than when they started. Myostatin inhibitors have been proposed as one answer to this, and several are in the pipeline.

Is it telling that the incumbents are active here? Lilly owns this mechanism’s most advanced project, the phase 2 bimagrumab, a muscle stimulating agent it acquired from Versanis for up to $1.9bn.

Elsewhere, Regeneron is in the process of starting a phase 2 trial investigating whether the addition of trevogrumab, an anti-myostatin antibody, to semaglutide can improve the quality of weight loss. An anti-activin A antibody, garetosmab, is also being tested as a potential triple therapy in the same trial.

Tempted by the incretins’ success and soaring forecasts for market size, the obesity pipeline has grown dramatically in the last couple of years. Developers are racing to put more convenient oral formulations, novel incretins and new mechanisms of action into the clinic. And sellside analysts and investors are assigning ever higher valuations to the companies and projects involved.

In 2024, Lilly became the first pharma company to breach a market cap of $800bn, one of the many remarkable statistics associated with the obesity space.

Note: NPV=Net Present Value, constructed fromconsensus sellside forecasts. Subq=subcutaneous injection. Source: Evaluate Omnium.

FIGURE 5: VALUING THE OBESITY PIPELINE, AND A SELECTION OF MID- AND LATE-STAGE PROJECTS

Project

Company

Approach

NPV

Cagrisema

Novo Nordisk

Amylin & GLP-1 agonist (once weekly, subq)

$57bn

Retatrutide

Eli Lilly

GIP, GCG & GLP-1 agonist (once weekly, subq)

$23bn

Orforglipron

GLP-1 agonist (daily, oral)

$15bn

MariTide

Amgen

GIP antagonist & GLP-1 agonist (monthly, subq)

$12bn

VK2735

Viking Therapeutics

GLP-1 & GIP agonist (once weekly, subq)

$3.7bn

GSBR-1290

Structure Therapeutics

$1.0bn

NPV of obesity pipeline

$118bn

NPV of marketed obesity drugs

$161bn

The obesity race is also prompting much dealmaking, a theme that is likely to continue in the coming months. The smaller companies in the table above are widely considered to be among biopharma’s hottest takeout prospects.

The prospect of a buyout means that investors are proving more than willing to back the independent players. Viking raised $630m in a secondary stock offering in early 2024, followed by a $550m financing from Structure, huge fundraising by small developers.

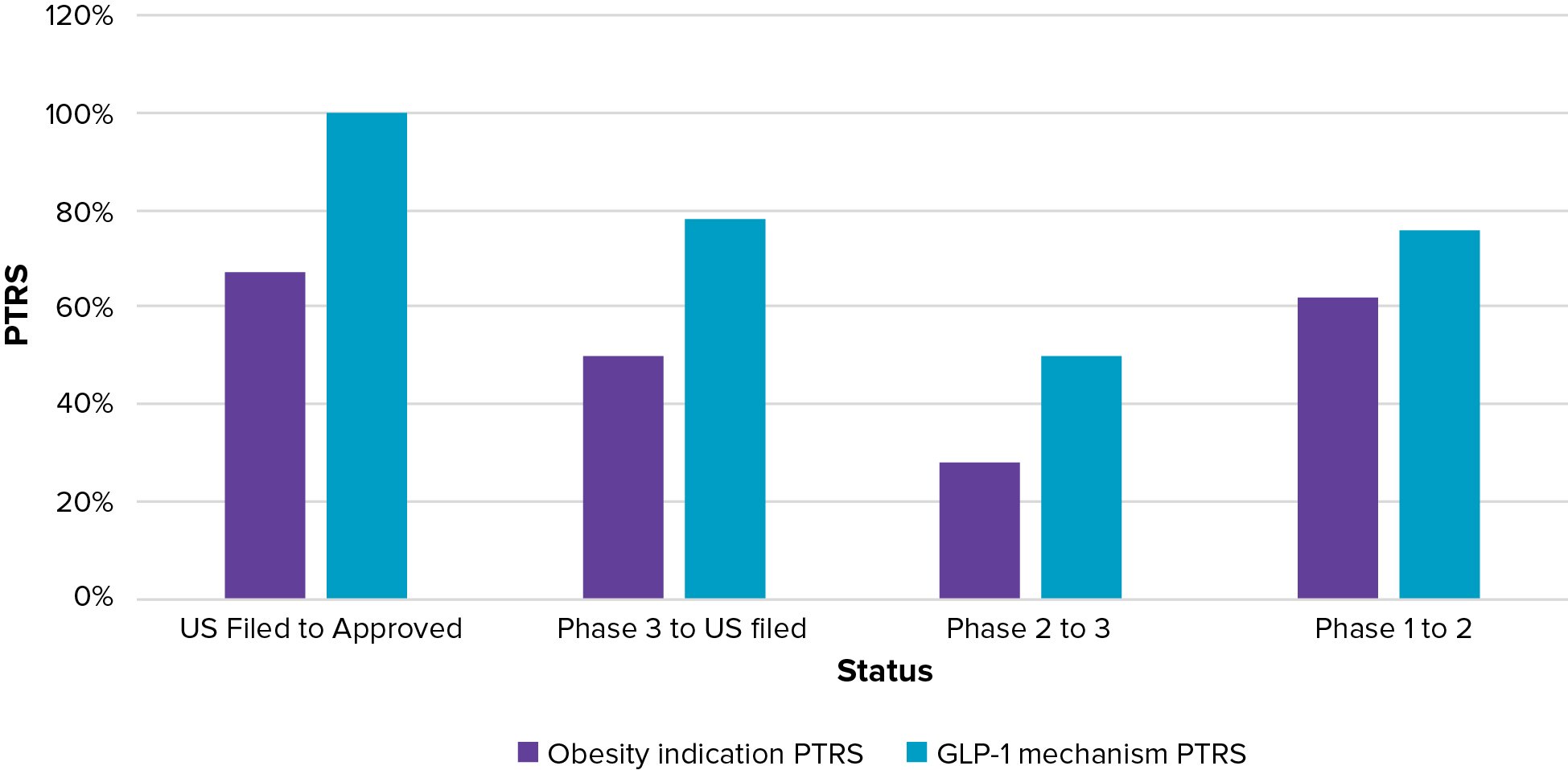

Some asset valuations in the table on the left suggest that success is guaranteed. But recent wins have come in the wake of years of disappointment. A look at the probability of technical and regulatory success – an estimate of a drug’s chances of progressing through the clinic – serves as a reminder.

Figure 6 shows Evaluate Omnium’s probability of technical and regulatory success for obesity as an indication, and the GLP-1 mechanism alone. This shows how novel GLP-1s, at all phase transition stages, have a substantially higher chance of success than the average obesity project.

The figures for GLP-1s include their progress across type 2 diabetes as well as obesity.

PTRS does not incorporate commercial success, of course, and on this measure the outperformance of the GLP mechanism over older obesity drugs would be even starker.

FIGURE 6: CALCULATING THE PROBABILITY OF TECHNICAL AND REGULATORY SUCCESS

Note: NMEs only. GLP mechanism includes single target drugs only (eg ex-GIP), and estimates reflect their progress across all indications. Source: Evaluate Omnium.

The obesity market’s vital stats unquestionably make it big pharma territory. Huge addressable populations need huge sales and marketing budgets; investment in manufacturing capacity is running to billions for Novo and Lilly, which are still scrambling to keep up with demand and still facing supply issues despite these investments. And ballooning asset costs require the writing of big business and development cheques.

True, smaller developers are vital for innovation and early research, but the cost of late-stage development, with vast clinical programmes required, can only be met by very deep pockets.

Figure 7 shows Evaluate Omnium’s estimates of the cost of cardiovascular outcome trials. These huge studies, designed to find even small signals of long-term harm, are among the most expensive to run. Any drug that wants to seriously compete in obesity will need to be put through this sort of trial.

FIGURE 7: THE COST OF CLINICAL DEVELOPMENT

Product

CVOT name

Enrollment

Estimated trial cost ($m)

Status

Wegovy

Novo

Select

17,604

$2.1bn

20% reduction of the risk of major CV events*

Survodutide

Boehringer Ingelheim/ Zealand

Synchronize-CVOT

4,935

$430m

Top-line readout likely 2025+

Redefine 3

7,000

$822m

Top-line readout due 2026+

Lilly

Triumph-Outcomes

10,000

$2.4bn

Zepbound

Surmount-MMO

15,374

Note: *NEJM, study conducted in people with obesity and overweight and preexisting cardiovascular disease. Source: Evaluate Omnium.https://www.nejm.org/doi/full/10.1056/NEJMoa2307563

So what is coming next for the obesity space? A lot of more data for a start. The table below is a tiny snapshot of the most anticipated read-outs. With vast sums of money being thrown at the disease, obesity has swiftly become one of biopharma’s most fast-moving fields.

It is also one of the most expansive, with vast amounts of work seeking to test the limits of incretins’ usefulness. Obesity and the processes of metabolic disfunction and inflammation are being associated with ever more disease areas. Neurological conditions like Alzheimer’s disease and Parkinson’s, for example, where incretins’ ability to lower inflammation are hypothesised to be behind potential efficacy.

Trials in these adjacent and related settings are now more important for expanding incretins’ potential than pushing weight loss in obesity a few percentage points higher. With Lilly and Novo now ranked the world’s 10th and 12th most valuable companies, many are already betting that these successes are locked in.

FIGURE 8: ON THE NEAR AND FAR TERM HORIZON: SELECTED OBESITY EVENTS AND READOUTS

Mechanism

Event

Oral semaglutide (sold as Rybelsus in T2D)

GLP-1 agonist

Second ph3 trial readout, OASIS-4, due mid-2024.

High-dose Wegovy

STEP UP trial (7.2mg) read out expected late 2024

MariTide (AMG 133)

GIP antagonist & GLP-1 agonist

Top-line ph2 data due late 2024, which could trigger move into pivotal development

Amylin & GLP-1 agonist

Readout of REDEFINE 1 expected late 2024, first pivotal trial from obesity programme (25% weight loss is the target)

Oral GLP-1 agonist

Ph2b trial projected to start late 2024

GLP-1 & GIP agonist

Ph2b trial projected to start late 2024. Further data on ph1 oral formulation also due 2024

Danuglipron

Pfizer

Update expected 2H24 on plans for once-daily programme (and probably other pipeline obesity projects)

Bimagrumab

Anti-activin Mab

Phase IIb BELIEVE trial in 495 patients, alone and in combination with semaglutide to report 2025

Orforglipron (oral)

Pivotal programme to report from 2025

GCG & GLP-1 agonist

Boehringer Ingelheim/ Zealand Pharma

Pivotal programme to report from 2026

Source: Evaluate Omnium's Calendar of Events