The Market Size Question

Just how big would this market become? Obesity is a sizeable market and co-morbidities could push it much higher.

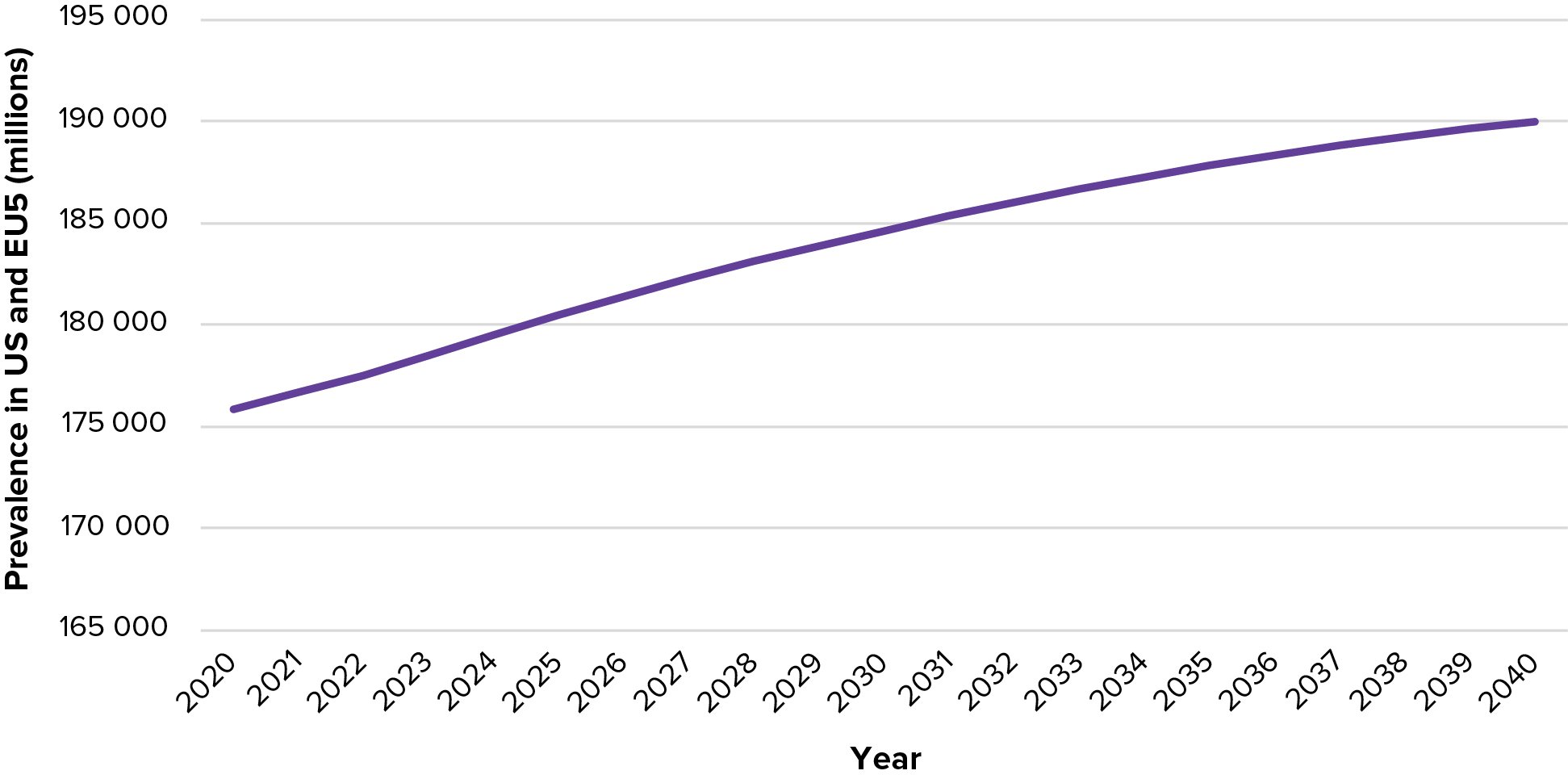

It is widely accepted that obesity is causing major problems in Western countries and is a growing concern for many less developed regions. Epidemiology data over a 20-year period show ballooning rates of obesity in the US and the five largest European economies – the United Kingdom, Germany, France, Italy and Spain.

The epidemiology data in this report focuses on this six-county region. The high price of these new obesity drugs means that these rich countries, particularly the US, will drive much of their demand.

FIGURE 1: OBESITY ON THE RISE

Note: EU5 is UK, Germany, France, Spain and Italy. Source: Evaluate Epi.

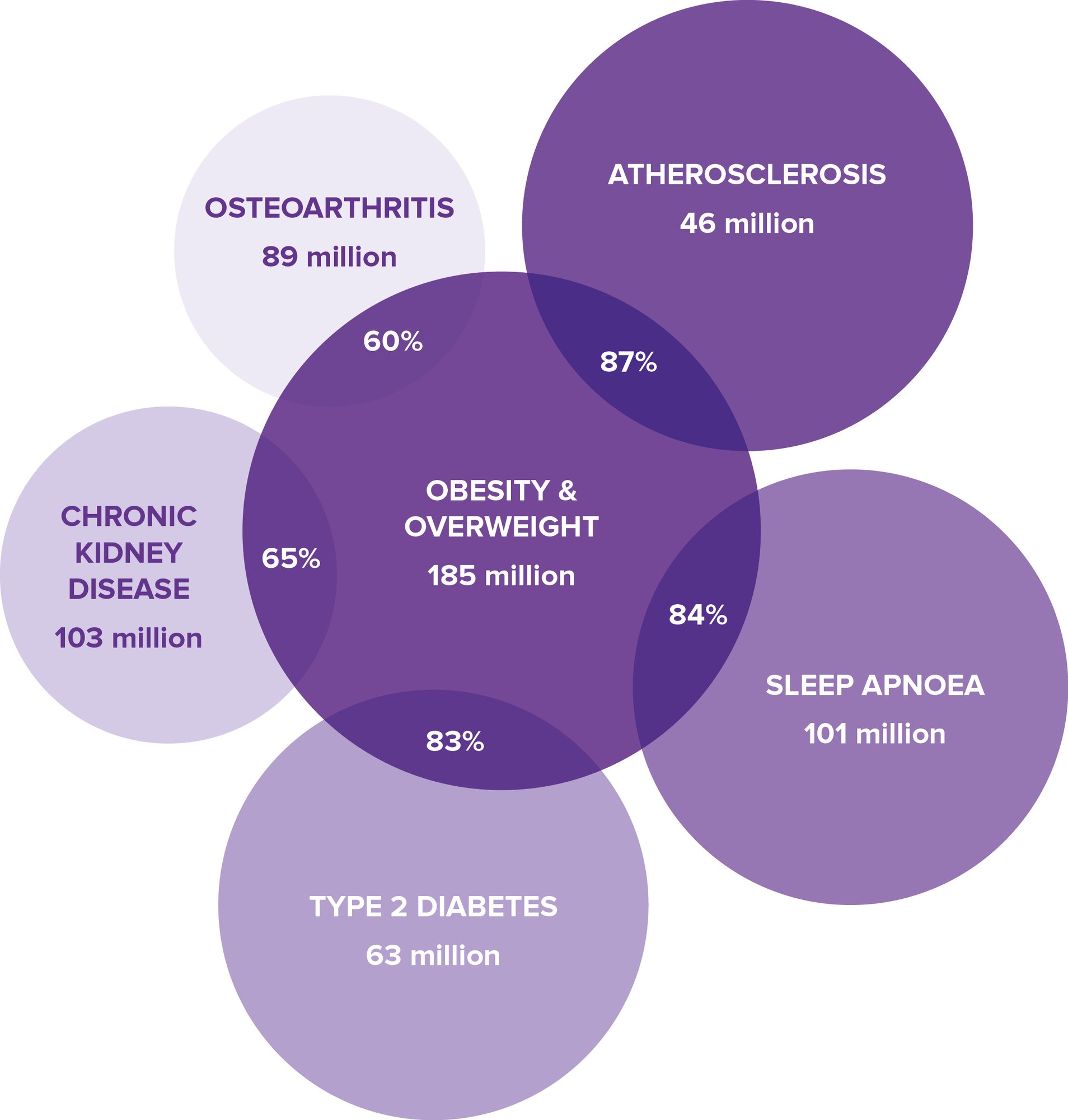

Obesity is a sizeable market in itself, however the incretins’ potential beyond straight weight loss is behind some of the really big numbers being attached to this drug mechanism. Excess body weight is associated with multiple co-morbidities, and much work is underway to prove that that these drugs can help conditions like sleep apnoea, chronic kidney disease and osteoarthritis.

Phase 3 trials in these and other related metabolic and cardiovascular settings represent some of biopharma’s most anticipated readouts, and not only because they could reinforce incretins’ broad utility. Success will help push open the doors of payers, many of which are reluctant to cover these expensive drugs for weight loss alone.

Incretin analogues are already well established – and selling billions – in type 2 diabetes, the disease for which these agents were initially developed. According to Evaluate Omnium, 83% of patients with type 2 diabetes also have obesity and overweight.

Evaluate Omnium’s epidemiology data allows this disease crossover to be mapped, with the below chart showing five co-morbidities; many more exist.

FIGURE 2: OBESITY AND BEYOND – PROJECTED CO-MORBIDITY PREVALENCE

Note: Note: Numbers are 2030 estimates for the US and EU5 (UK, Germany, France, Italy and Spain). Source: Evaluate Epi.

Studies in adjacent conditions remain a work in progress, but a handful of wins are fuelling big thinking. Notable successes include the FLOW trial of semaglutide in people with type 2 diabetes and chronic kidney disease, which was stopped early for efficacy, and tirzepatide’s performance in SYNERGY-NASH, in patients with liver disease.

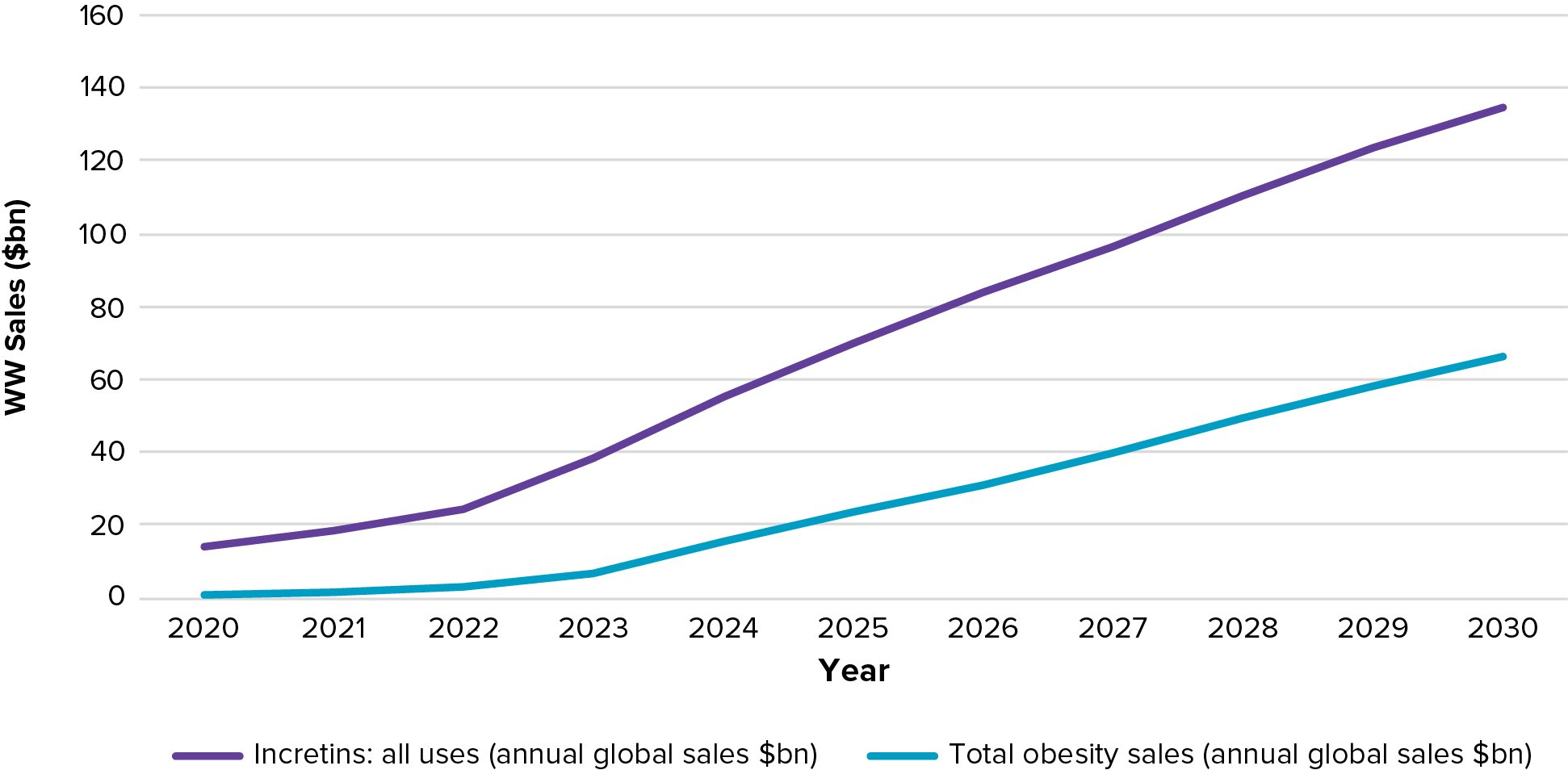

Many financial analysts believe that the incretins, across all uses, could become biopharma’s first drug class to hit annual sales of $100bn. Some estimate that figure could end up closer to $200bn. This is a huge prediction when considering the $67bn peak annual sales projection for the next most successful drug class, anti-PD-(L)1 antibodies, a group of cancer checkpoint inhibitors led by Merck & Co’s Keytruda.

That $100bn year is not that far away, Evaluate Pharma’s forecasts reveal. It is important to remember that these huge projections include incretin sales made in all settings, not just obesity. For now, that means type 2 diabetes.

The graph below shows sales of incretin drugs (all uses) against obesity market sales. The obesity market is mostly a picture of the incretins, which generated 93% of obesity market sales in 2023, a proportion set to grow to 97% by 2030.

These agents are on track to create an obesity market worth $66bn in only a decade.

The only notable non-incretin obesity drug on or close to the market is Rhythm Pharmaceuticals’ melanocortin-4 agonist Imcivree (setmelanotide), which is approved for rare, genetic causes of obesity.

FIGURE 3: SALES OF OBESITY DRUGS AND THE INCRETIN EFFECT

There are still several moving parts to obesity forecasts, however, with duration of use one big unanswered question.

Patients stay on Saxenda, Novo Nordisk’s first-generation once-daily GLP-1 agonist, for five to six months on average and lose around 5% to 10% of their body weight. This improved to up to 20% with the once-weekly products, Wegovy and Zepbound, an experience that is expected to motivate people to remain on therapy for longer.

But how long exactly? In terms of real-world use, it is still too soon to answer that question, developers contend. This is fair for Lilly’s Zepbound, which was only approved in late 2023. But even Novo says it is too soon to confirm the so-called stay time of patients for Wegovy, despite the product having been available in the US since 2021.

True, supply problems have likely complicated the picture, though clues can be gleaned from clinical trials. In the large cardiovascular outcome study, SELECT, 8,800 patients took Wegovy for a median duration of 33.3 months. And in the pivotal STEP 1 trial, 83% of the 1,306 subjects randomised to Wegovy were still on treatment at the end of 68 weeks.

The manufacturers state that obesity is a chronic disease that requires chronic treatment, a stance that is slowly gaining support in the medical community. Payers are proving harder to convince, however, so for now duration of use is more of a reimbursement question.

Those picking up the bills for these new drugs are placing restrictions on use, including around treatment duration. For example, in the UK the price watchdog NICE restricts Wegovy to a maximum of two years. Commercial health plans in the US have put duration limitations that vary from weeks to years.

The US government funded healthcare system for elderly patients, Medicare, has long been prohibited by law from paying for drugs for weight loss alone. But that red line is starting to fade. The FDA’s approval of a cardiovascular risk reduction claim on Wegovy’s label, in the wake of SELECT, means that Medicare can now cover Wegovy, and other obesity drugs, if they are approved for additional health benefits.

Payers’ reluctance is understandable given the cost of these drugs and the many millions of potential patients. A frequently cited New England Journal of Medicine editorial calculated that if all eligible Medicare enrolees were prescribed Wegovy, it would cost $269bn.

So, what is the price of these medicines? In the US, wholesale acquisition costs put a year’s supply of Wegovy at $16,118; Zepbound comes in at $12,718 a year. These numbers do not reflect rebates or the effect of volume negotiations.

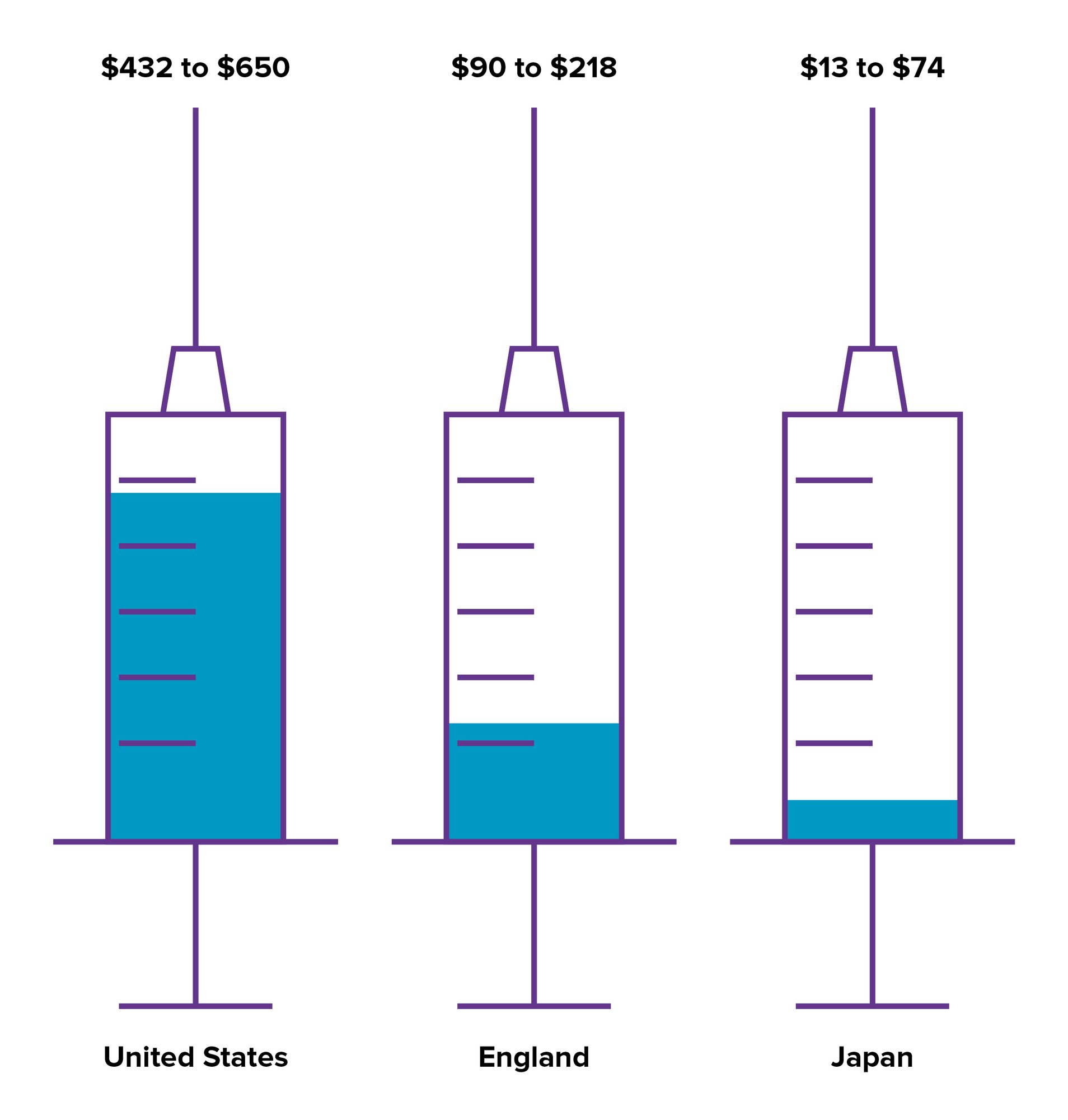

US drug prices are higher than elsewhere, however. In Europe, each country will negotiate separately, and prices paid are frequently confidential. Evaluate Omnium does provide some snap shots from across the globe, however.

As of early 2024, one pre-filled Wegovy syringe, enough for a weekly dose, cost between $432 and $650 in the US, depending on the dose, according to the Centers for Medicare and Medicaid Services’ NADAC survey. In England, that comparative range was $90 to $218, while in Japan that cost comes in at $13 to $74.

How these prices evolve is a big focus for those watching the obesity space. With competition mounting, expectations are that prices will fall. The approval of more oral agents could also prompt price drops, as pills can typically be made more cheaply than drugs that need to be injected.

FIGURE 4: COMPARATIVE COST RANGE OF ONE PRE-FILLED WEGOVY SYRINGE