Development Versus Dealmaking: How To Obtain A Blockbuster

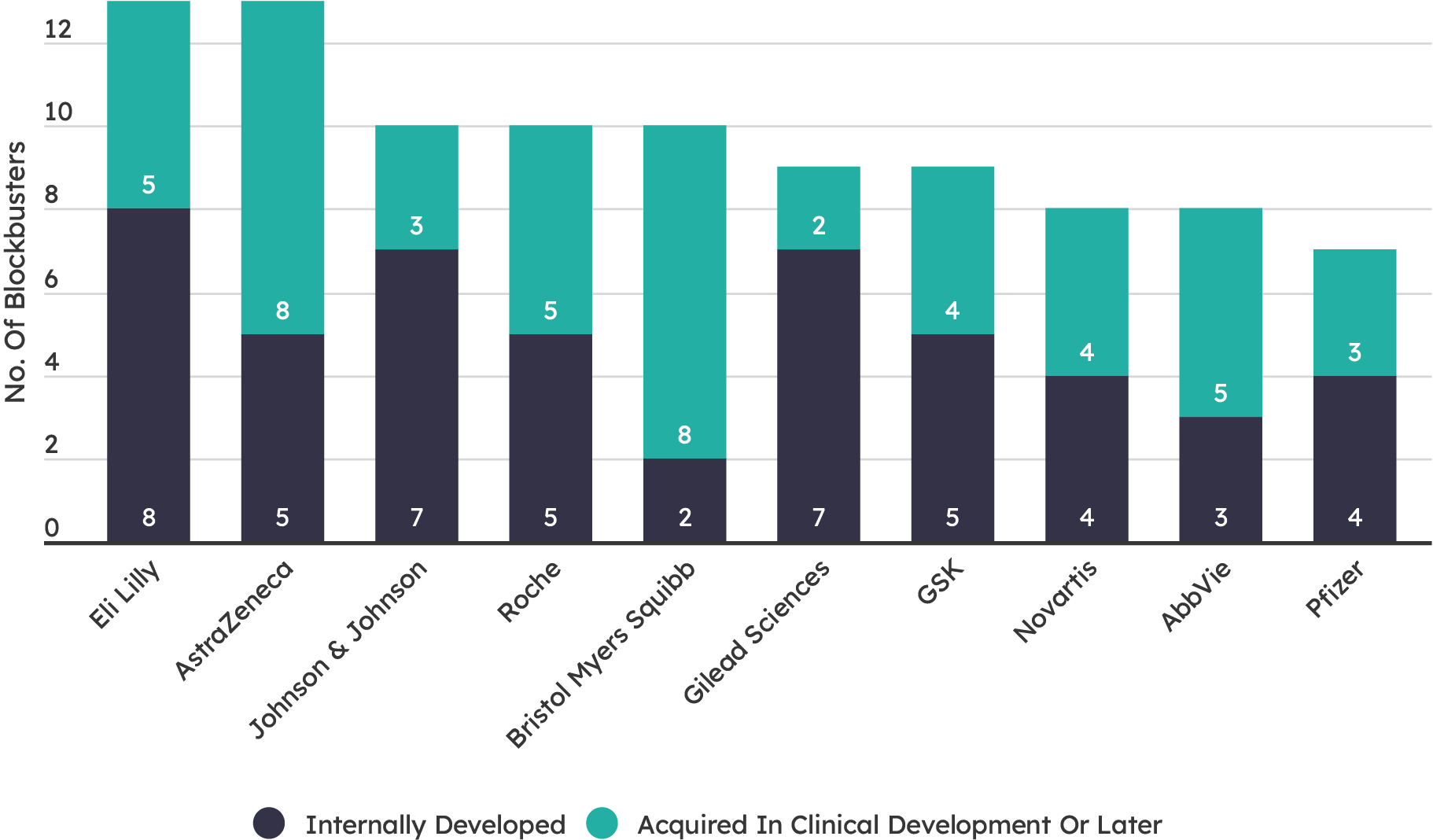

Most of the companies with blockbuster drugs approved over the past decade oversaw their clinical development internally. Lilly holds the lead with eight blockbusters developed in-house.

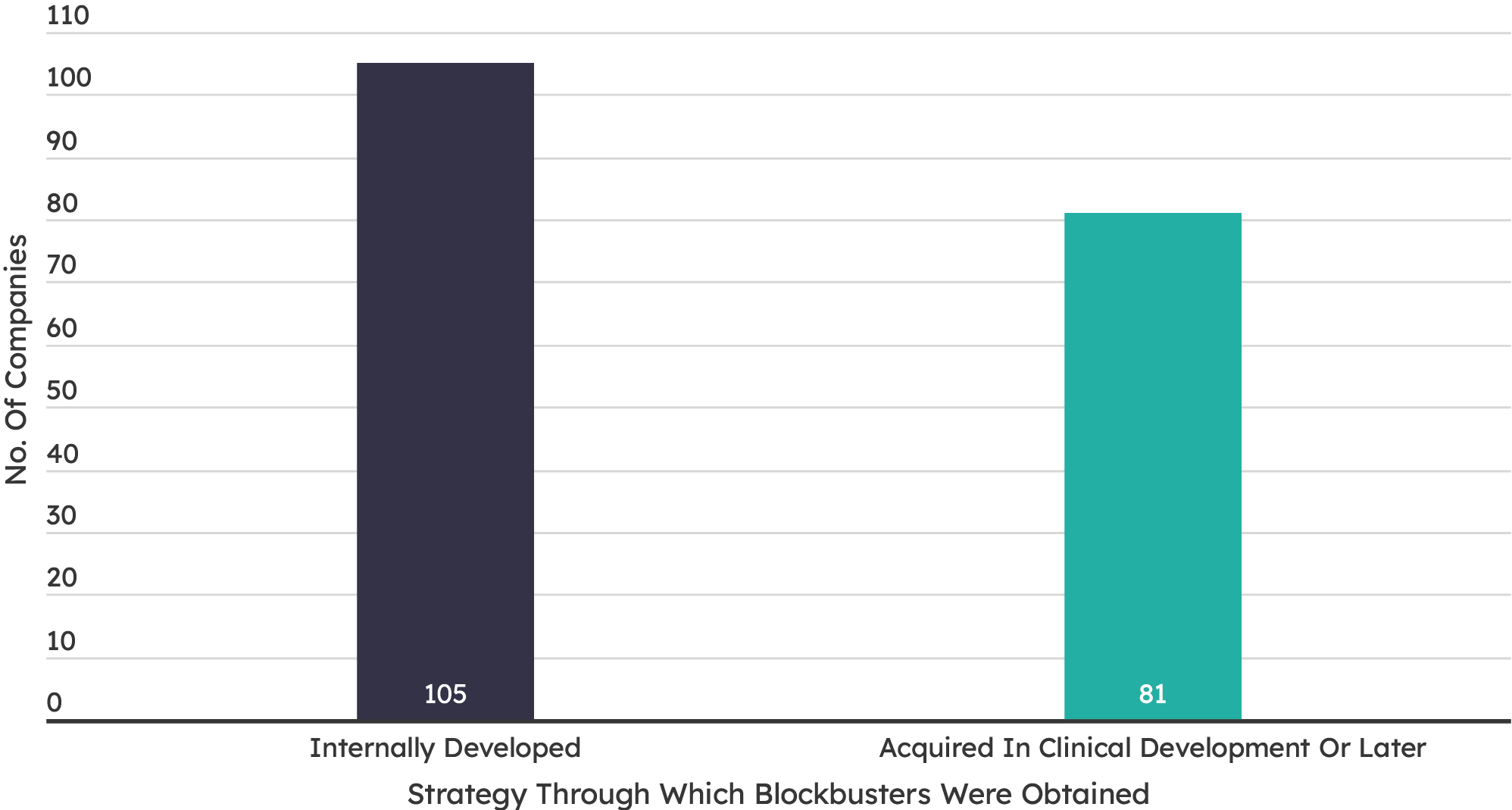

Considering that an actual or potential blockbuster developed by a smaller biotech is catnip to Big Pharma, obtaining a blockbuster by buying it might be expected to be the most common strategy. But according to data from Evaluate Pharma, only 81 companies with blockbusters gained them through dealmaking – at least when the parameters are limited to clinical stages.

Meanwhile, 105 drug companies either discovered blockbusters internally or bought them before clinical trials had started. Many companies that developed blockbusters in-house are Big Pharmas or big biotechs, including big names like Novo Nordisk A/S, which discovered and developed Ozempic (semaglutide) and Johnson & Johnson, which developed Tremfya (guselkumab).

There are also some niche products that are out-licensed but are only expected to yield blockbuster numbers for the originator. One such is Sarepta Therapeutics, Inc.’s Duchenne gene therapy Elevidys (delandistrogene moxeparvovec), partnered with Roche Holding AG. Elevidys is forecast to earn $2.4bn for Sarepta in 2028, down from a peak of $3.0bn in 2026. The same year, just $489m will accrue to Roche, according to Evaluate’s forecasts.

Note: "Internally Developed" includes assets acquired or licensed while still preclinical. Source: Evaluate Pharma

One of the companies with the most blockbusters approved in recent years is Eli Lilly and Company – currently the world’s biggest pharma company by market cap.

From the start of 2014 to the end of 2023 170 drugs were approved in the US that, as of February 2024, had earned (or were forecast to earn) total sales of more than $1bn in any year up to 2028. This analysis counts only those drugs with blockbuster revenues that will accrue to a single company. For example, a partnered drug poised to earn $600m for

company A and $600m for company B, is excluded from the analysis.

Conversely, a product that earns over $1bn for more than one company – such as Enhertu (trastuzumab deruxtecan), the cancer drug that has made blockbuster numbers for both Daiichi Sankyo Co., Ltd. and AstraZeneca PLC – is counted twice.

Lastly, if a product deal is done while the asset is still preclinical, it is counted as internally developed by the buyer. A clear example is Keytruda (pembrolizumab), the checkpoint inhibitor discovered by Organon and, through nested acquisitions, ultimately landed with Merck & Co., Inc.. Since Merck obtained pembrolizumab before the asset entered the clinic, and funded its clinical development, Evaluate counts it as an internal Merck product.

The asset that later became the mega-blockbuster Keytruda, the PD-1 inhibitor pembrolizumab, was initially discovered by scientists at Organon. This group was bought by Schering-Plough in November 2007 for $14.4bn; at this point pembrolizumab was still preclinical. Schering-Plough was itself taken out by Merck & Co. in November 2009, for $41.1bn. Pembrolizumab had not yet reached the clinic, and Merck showed little interest in the program until 2011, when it pushed the drug into Phase I in metastatic carcinoma, melanoma, or non-small cell lung cancer. Keytruda was first approved for melanoma in 2014, and became a blockbuster in 2016.

When AstraZeneca obtained the paroxysmal nocturnal hemoglobinuria therapy Ultomiris, via the $13.3bn acquisition of the drug’s originator, Alexion Pharmaceuticals, in July 2021, the product had been on the market for two years. Though it did not become a blockbuster until 2022, the drug already carried billion-dollar forecasts, and the lure of adding a blockbuster would have been a major factor in AstraZeneca’s decision to buy Alexion.

Bristol Myers Squibb’s rival PD-1, Opdivo (nivolumab), also arrived via acquisition, BMS’s purchase of Medarex for $2.4bn in 2009.

Medarex started the first clinical trial of nivolumab in 2006, but it was not the originator. Nivolumab initially came from the labs of Ono Pharmaceutical, and it was still in early research when Medarex licensed it from Ono. Opdivo was first approved for melanoma in December 2014, and achieved blockbuster status the year after.

Boehringer Ingelheim first put Ofev (nintedanib) into clinical trials in 2005, having discovered the tyrosine kinase inhibitor internally. Approved for idiopathic pulmonary fibrosis in 2014, it became a blockbuster in 2017. Boehringer has never cut a deal for the product.

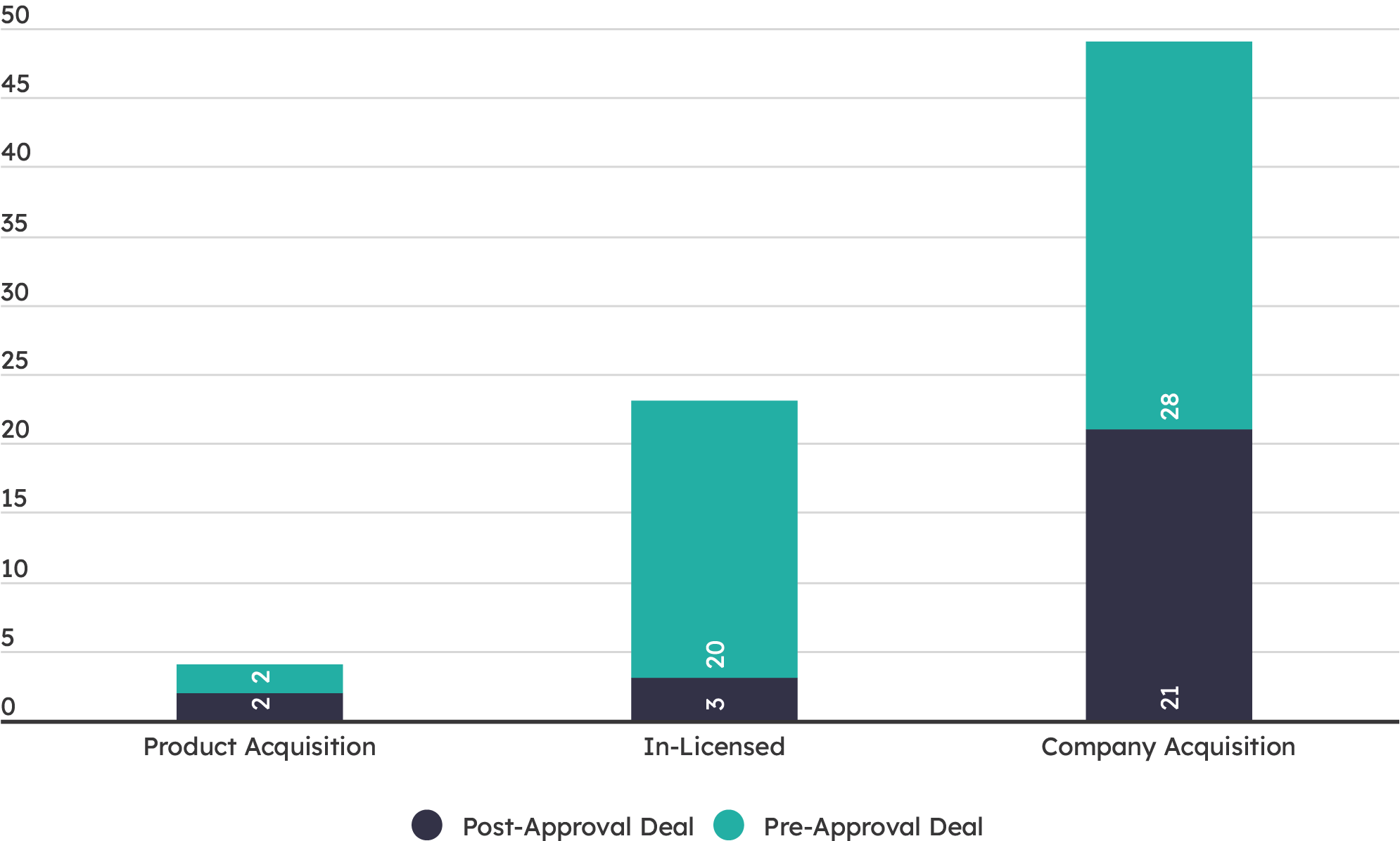

There are three main strategies for getting hold of a current or future blockbuster that was originated elsewhere – licensing, buying the product, or buying the whole company. A company acquisition is the most popular. In the past decade, 49 companies with a product earning blockbuster sales, or still in clinical trials but forecast to be a blockbuster, have been bought out. And buyers are comfortable with a certain amount of risk. Twenty-eight companies took action while the potential billion-dollar seller was still in clinical trials, while only 21 companies reduced their risk by obtaining it post-approval.

Licensing deals are much more likely to occur for clinical stage blockbusters-in-waiting than approved products. Spotting the promise of a drug and signing up rights at an early clinical stage can be a highly lucrative strategy; if things go wrong, milestone and royalty payments need never be made.

Note: "Pre-approval deal" does not include assets that were preclinical when the deal was struck Source: Evaluate Pharma

If the effort to develop or otherwise obtain blockbusters over the past 10 years is a competition, the joint winners are Lilly and AstraZeneca. Each has gained approval in that time for 13 assets with actual or forecast blockbuster sales. But Lilly managed to originate eight, whereas only two of AstraZeneca’s were discovered by that company (AstraZeneca bought in a further two and in-licensed another while they were still preclinical).

And Lilly’s blockbusters are bringing in more, driven by the obesity surge. Mounjaro (tirzepatide), is forecast to be Lilly’s best seller in 2028 with sales of $12.1bn. AstraZeneca’s biggest drug that year will be its lung cancer therapy Tagrisso (osimertinib), with sales of $7.8bn.

Looked at a different way, though, perhaps AstraZeneca’s achievement is the greater. The UK group is punching above its weight in terms of market cap, since its valuation of $205bn is less than a third of Lilly’s worth. And even more impressively, the cumulative figure for actual and forecast sales of AstraZeneca’s 13 blockbusters from 2014 to 2028 comes to $306bn. The equivalent number for Lilly is $283bn.

Of these top 10 companies, the best at originating its own products, in percentage terms, is Gilead Sciences, Inc.. Seven of its nine blockbusters were invented in-house, for a 78% hit rate.

Bristol Myers Squibb Company is at the other end of the scale, having bought in all but two of its 10 money-spinners. Its $74bn acquisition of Celgene Corporation netted it four of them, but a better value deal was its 2009 takeout of Medarex for the much lower sum of $2.4bn, through which it gained the checkpoint inhibitors Yervoy (ipilimumab) and Opdivo (nivolumab). Sales of the latter are forecast to peak in 2027 at $13bn, showing that, done right, deals can be an excellent way of entering the blockbuster hall of fame.

Drug

Company

Strategy

Stage at which it changed hands

Keytruda

Merck & Co.

Internally developed

Preclinical*

Ozempic

Novo Nordisk

-

Biktar vy

Gilead Sciences

Dupixent

Sanofi

Opdivo

Bristol Myers Squibb

Acquired in clinical development or later

Phase I

Darzalex

Johnson & Johnson

Phase II

Trikafta

Vertex Pharmaceuticals

Jardiance

Boehringer Ingelheim

Phase III

Skyrizi

AbbVie

Trulicity

Eli Lilly

Ocrevus

Roche

Farxiga

AstraZeneca

Marketed

Tagrisso

Entyvio

Takeda

Mounjaro

Wegovy

Tecentriq

Rinvoq

Verzenio

Enher tu**

Daichi Sankyo

*Drugs which changed hands at the preclinical stage are defined as internally developed for the purposes of this analysis. **Enhertu was originated by Daiichi and licensed to AstraZeneca; since it brings in blockbuster sales for both, this analysis counts it twice.