Rapid Rise Or Slow Roll: How Long Does It Take To Become A Blockbuster?

Our team analysed data on top-selling drugs to see how long it takes to surpass $1bn in revenues and grow into $5bn and even $10bn brands.

A new drug that is quick to reach blockbuster status – or $1bn in revenues – is often a sign of a mega-blockbuster in the making. Launch trajectories are a closely watched metric to evaluate a new drug’s likelihood of long-term commercial success.

Historically, $200m in first year sales for a new drug has been a benchmark for predicting an eventual blockbuster-sized seller, though in some therapeutic areas like oncology and immunology, launch trajectories have lengthened as the categories have grown more competitive and market access has taken longer to secure.

In rare instances, new drugs burst out of the gate, addressing a critical unmet need or a big market opportunity, and in those cases a new drug can generate close to $1bn in sales in its first year, a sign the drug is on its way to becoming a mega-blockbuster-sized commercial winner.

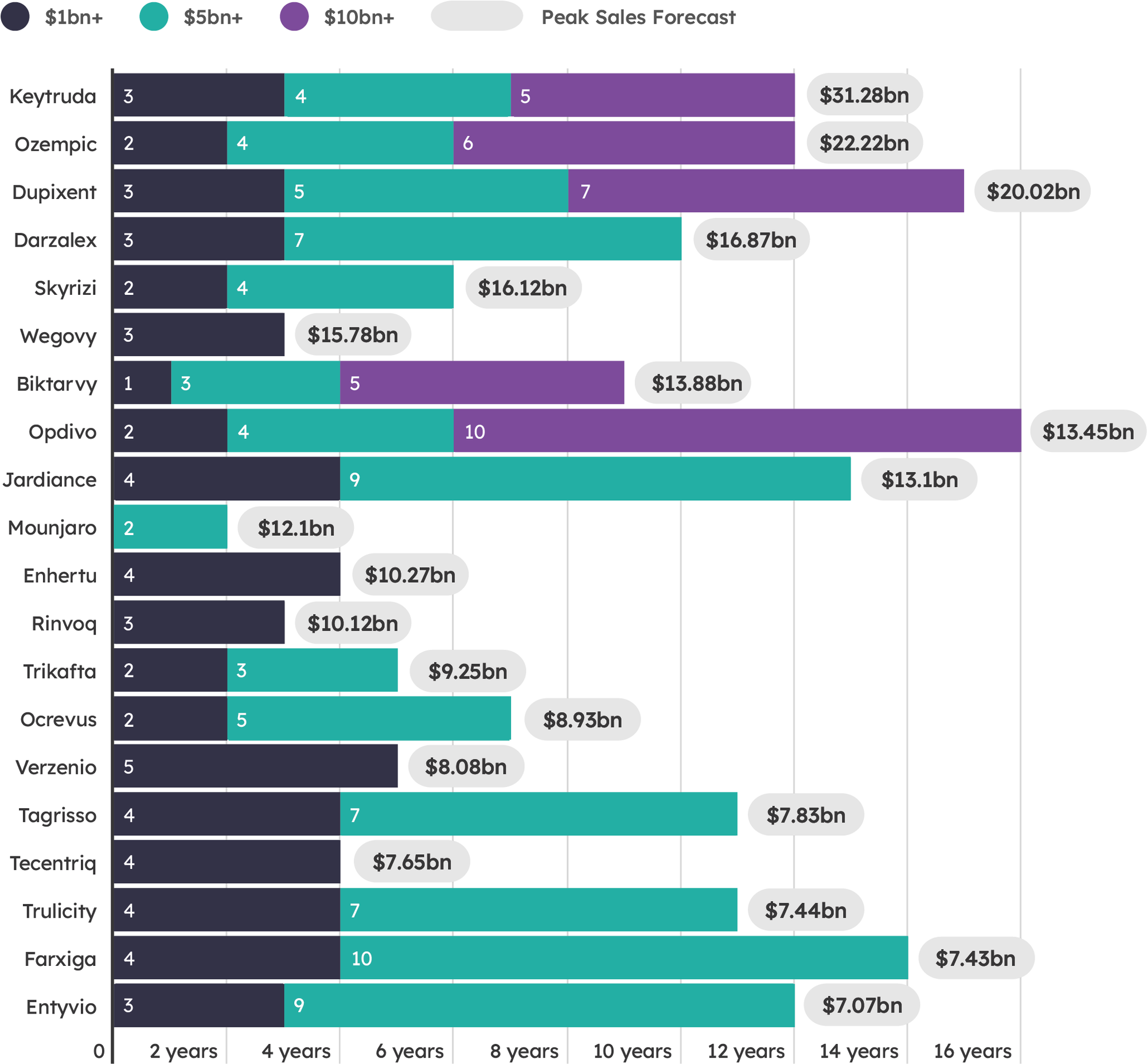

Of 20 top-selling drugs that launched since 2014, it took an average of three years for drugs to generate $1bn or more in sales. It took 5.5 years on average for the 15 drugs that surpassed $5bn in sales to reach that threshold and it took an average 6.6 years for the five drugs that reached $10bn or more in sales to hit that marker, according to Evaluate Pharma.

A look at how long it took some of the industry’s best-selling drugs to pass $1bn, $5bn and $10bn in annual revenues.

Note: Data includes year of launch as year one. Selected drugs are those that launched in the last 10 years and ranked by peak year sales forecasts, excluding COVID-19 products and Harvoni due to the unusual sales trajectory, and Zepbound, which only launched in December 2023. Source: Evaluate Pharma

The analysis counts the year of launch as the first year on the market even when the launch occurred late in the year. Each of the drugs launched at different times so it is not possible to draw any direct commercial comparisons, but all of the drugs included are expected to be among the industry’s top sellers based on peak sales forecast by Evaluate Pharma.

The analysis excludes COVID-19 products and Gilead Sciences, Inc.’s hepatitis C drug Harvoni (ledipasvir/sofosbuvir) due to their atypical launch trajectory and Eli Lilly and Company’s obesity drug Zepbound (tirzepatide), which is expected to be a big seller based on peak sales forecasts but only launched in December 2023.

Of the drugs included in the analysis, Lilly’s Mounjaro, the same active ingredient used in Zepbound but approved for type 2 diabetes, stands out as the fastest mega-blockbuster-sized seller. Mounjaro surpassed $5bn in revenues in only its second year on the market, generating $5.16bn in 2023, powered presumably by off-label use in obesity.

Novo Nordisk’s Wegovy (semaglutide) – another notable seller – would have presumably experienced a similar rocket-fuelled launch if the company had not faced supply constraints the first two years after approval by the US Food and Drug Administration. The drug generated much less in its first two years on the market, $200m and $888m, respectively in 2021 and 2022. Demand for the drug has continued to outstrip supply through 2023, but it did achieve blockbuster sales as of Q1 2024.

Gilead’s HIV pill Biktarvy (bictegravir/ emtricitabine/tenofovir) is another notable standout, surpassing blockbuster status its first year on the market, generating $1.18bn in 2018 and becoming a $10bn-plus seller in 2022, five years after launching. The combination pill, however, is built on the back of older, well-known medicines, so the launch trajectory is not necessarily similar to that of a brand new medicine.

Drugs that fit a typical launch model that generate more than $1bn in sales in the first year on the market are rare indeed. In addition to Mounjaro, which achieved that milestone, other drugs that have come close to hitting the mark include Regeneron’s Eylea (aflibercept) for wet age-related macular degeneration in 2012, Biogen’s MS drug Tecfidera (dimethyl fumarate) in 2013, Bristol Myers Squibb’s Opdivo (nivolumab) for cancer in 2015 and Roche’s multiple sclerosis drug Ocrevus (ocrelizumab) in 2018.