Blockbusters By Indication: More Begets More

This analysis of the industry’s top-selling drugs examines the power of indication expansion to drive revenue growth.

Pharmaceutical manufacturers have been keen to invest in drugs that have potential in multiple diseases, paving the way for revenue growth through indication expansion. The phrase "pipeline-in-a-pill" has become as ubiquitous in R&D circles as "string of pearls" has become in dealmaking.

An analysis of industry’s top-selling drugs underscores the value of indication expansion to drive growth, but also raises questions about whether that pattern will continue at the same pace in the future.

Among 20 of the industry’s best-selling drugs that launched since 2014 and are forecast to have the highest peak sales potential, half are approved by the US Food and Drug Administration for three or more indications and seven are approved for five or more.

In this class, Merck & Co., Inc.’s Keytruda (pembrolizumab) – expected to have the highest peak sales – is the poster child with 20 different cancer indications. Keytruda is expected to generate revenues of $31.28bn in peak year sales in 2027, according to data compiled by Evaluate Pharma. Bristol Myers Squibb Company’s Opdivo (nivolumab) has the second most indications of the group with 11 cancer indications; peak year sales are forecast at $13.45bn in 2027.

Only one of the 20 drugs with the highest peak sales potential have a single indication – Vertex Pharmaceuticals Incorporated’s Trikafta (elexacaftor/tezacaftor/ivacaftor) for cystic fibrosis. Eli Lilly and Company has separate brands for tirzepatide – Mounjaro for diabetes and Zepbound for obesity – each producing blockbuster sales for the same molecule. Mounjaro/Zepbound are newer drugs, however, approved by the FDA in 2022 and 2023, respectively, and are likely to gain new indications.

A look at the top 20 best selling drugs launched since 2014, ordered by 2023 sales.

Drug

Company

Therapy Area

No. Of Indications

2023 Sales ($bn)

Keytruda

Merck & Co.

Oncology

20

18.1

Ozempic

NovNordisk

Metabolic

2

13.9

Biktar vy

Gilead Sciences

Antiviral

11.9

Dupixent

Sanofi

Immunology

5

11.6

Opdivo

Bristol Myers Squibb

11

9.9

Darzalex

Johnsn & Johnson

8

9.7

Trikafta

Vertex Pharmaceuticals

Respiratory

1

8.9

Jardiance

Boehringer Ingelheim

4

8.1

Skyrizi

AbbVie

3

7.8

Trulicity

Eli Lilly

7.1

Ocrevus

Roche

Neurology

Farxiga

AstraZeneca

6.5

Tagrisso

5.8

Entyvio

Takeda

Gastro-Intestinal

5.5

Mounjaro

5.2

Wegovy

4.6

Tecentriq

4.2

Rinvoq

4.0

Verzenio

3.9

Enher tu

Daichi Sankyo/AstraZeneca

2.6

Note: Top 20 drugs selected by peak year sales. Excludes COVID-19 products and Gilead’s hepatitis C drug Harvoni (ledipasvir/sofosbuvir) owing to their atypical launch trajectory, and Lilly’s obesity drug Zepbound, which is expected to be a big seller but only launched in December 2023. Source: drug labels and company 10-Ks.

It is hard to attain mega-blockbuster status with a single indication, but not impossible as Trikafta has shown, when a drug meets a serious unmet need in a substantial patient population. Cancer has been an especially prime field for growth through indication expansion. A typical launch pattern in oncology sees a drug starting in a hard-to-treat or late-stage disease before expanding into earlier lines of treatment and different indications.

Of the 20 drugs launched since 2014 that have the highest peak sales forecasts, seven are cancer drugs; all seven are approved for at least four indications.

Indication expansion has been a big area of industry focus over the past decade, but the rollout of the Inflation Reduction Act in the US, which introduces Medicare drug price negotiation, is believed to undermine that model of drug development. Evaluate Pharma’s forecasts also trend downwards. For drugs approved in 2019 and after, for drugs that have not yet had a full five years on the market, the five-year supplemental approval averages fall from 2.5 to a forecast of 1.8 from 2023-2028.

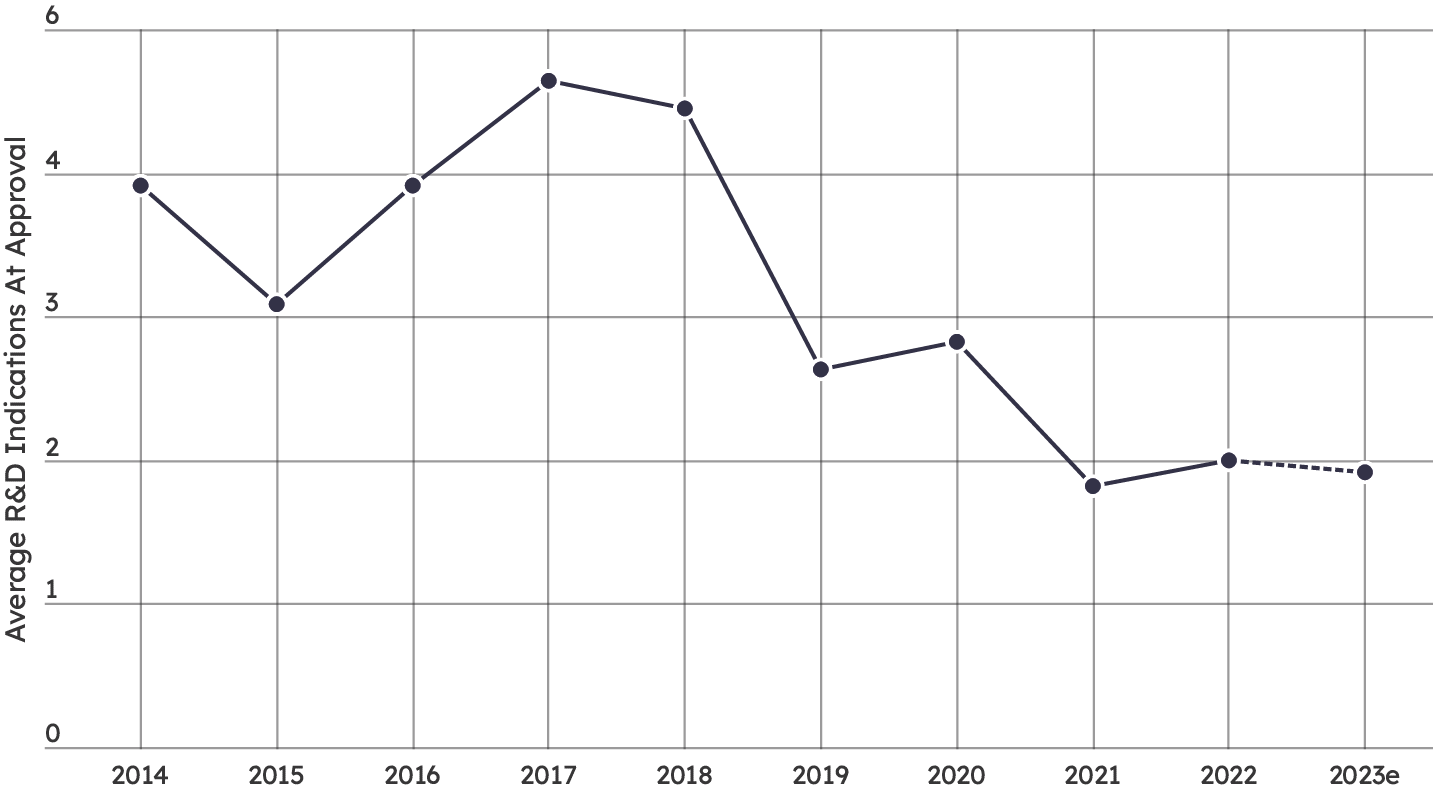

Diving deeper and looking at blockbusters with forecast supplemental approvals in indications for which they are still in clinical trials also shows a move toward fewer indications. Blockbusters approved in the US in 2018 were in the clinic for an average of 5.5 additional conditions, while blockbusters approved in 2022 were, on average, only being studied in 2.3 other conditions on average, a decline of nearly 60%.

Average clinical-stage indications under way for blockbuster drugs at initial US approval

These analyses take as their basis all the drugs approved in the US in the past decade that are either already blockbusters or are predicted to achieve this status by 2028. This is dated from the first US approval, but sales from subsequent approvals are included in the total. Source: Evaluate Pharma (data as of February)

The saturation of the market with checkpoint inhibitors is likely a contributor to that downward trend. Keytruda, for example, was in the clinic for 20 additional tumour types in 2014, the year it was approved for melanoma.

Of 17 drugs that are forecast to become blockbusters that gained an initial US approval in 2023, meanwhile, six of them are not in the clinic for any other diseases. RSV vaccines like GSK plc’s Arexvy and Pfizer Inc.’s Abrysvo are in this category as they are not applicable to any other infection.

Nonetheless, Big Pharma’s interest in the pipeline-in-a-pill strategy doesn’t appear to be waning. Indication expansion opportunities have been a cornerstone of some recent high-profile business development deals like Pfizer’s acquisition of Velsipity (etrasimod) with the buyout of Arena Pharmaceuticals, Inc. in 2021 and Merck & Co.’s addition of Winrevair (sotatercept) with the 2021 acquisition of Acceleron Pharma, Inc.

An area of R&D that will likely drive continued indication expansion is antibody-drug conjugates (ADCs) for cancer. One pioneering ADC is blazing that trail already: Daiichi Sankyo Co., Ltd./AstraZeneca PLC’s Enhertu (fam-trastuzumab deruxtecan), which is approved in five cancer types and in trials in 11 more. The partners are also developing a second ADC, datopotamab deruxtecan, which is expected to be approved this year and forecast to become a blockbuster in its first indication, non-small cell lung cancer, but is also in the clinic in 12 more tumour types.

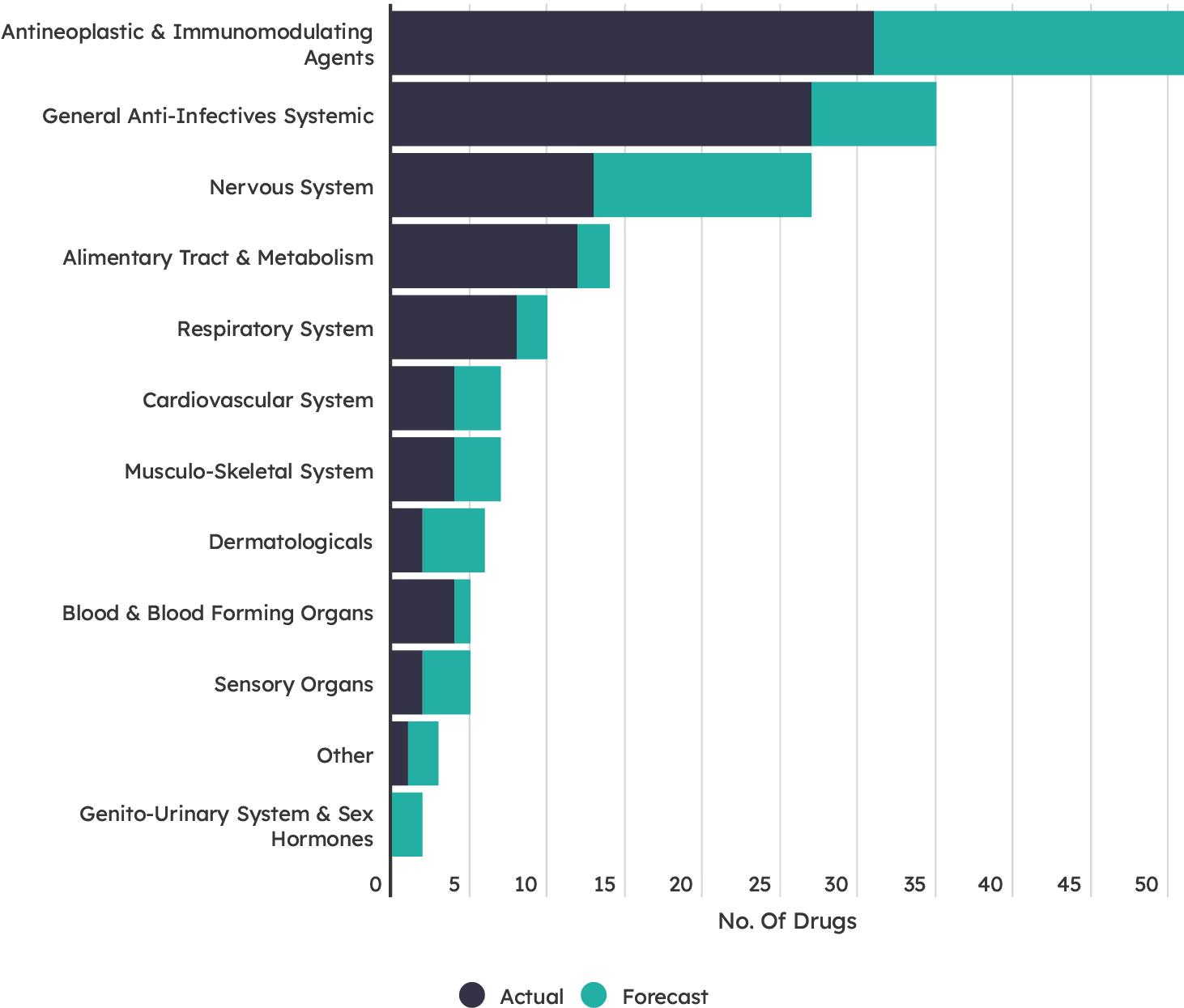

Over the past 10 years from 2014-2024, cancer has reliably been where the money is, with anti-infection drugs coming behind, according to Evaluate data.

Looking at drugs by therapeutic area shows cancer has led the blockbuster field. Of the 51 drugs classified as antineoplastic and immunomodulating agents – the categories most often used to treat cancer – approved in the US between 2014 and 2023, 31 are already blockbusters. A further 20 cancer drugs are forecast by Evaluate to hit $1bn in sales over the next four years, including Bristol Myers Squibb’s CAR-T therapy Abecma (idecabtagene vicleucel), Johnson & Johnson’s Carvykti (ciltacabtagene autoleucel) and Roche’s Polivy (polatuzumab vedotin).

The anti-infective category is not far behind cancer when it comes to existing blockbusters, with 27 drugs approved in the past decade generating $1bn or more. Perhaps surprisingly, COVID-19 does not play as large a role as might be expected. True, big names like Comirnaty from BioNTech and Pfizer, Moderna’s Spikevax and Pfizer’s therapy Paxlovid (nirmatrelvir/ritonavir) are represented. But the majority of the past decade’s existing anti-infective blockbusters predate the pandemic.

Gilead is the big name in this category, with its HIV and hepatitis franchises, along with its COVID-19 therapy Veklury (remdesivir), accounting for seven of the 27 existing blockbusters. Looking ahead, the respiratory syncytial virus (RSV) category is poised to be a lucrative one, with vaccines like GSK’s Arexvy and Pfizer’s Abrysvo and AstraZeneca/Sanofi’s monoclonal antibody treatment Beyfortus (nirsevimab) positioned to be big sellers.

Actual and forecast blockbuster drugs approved between 2014-2023

These analyses take as their basis all the drugs approved in the US in the past decade that are either already blockbusters or are predicted to achieve this status by 2028. This is dated from the first US approval, but sales from subsequent approvals are included in the total. Product s are categorised by EPHMRA code. These were devised by the European Pharmaceutical Market Research Association (EPHMRA) to classify product s according to their indications and therapeutic use. Source: Evaluate Pharma (data as of February 2024).