EVALUATING Key Players

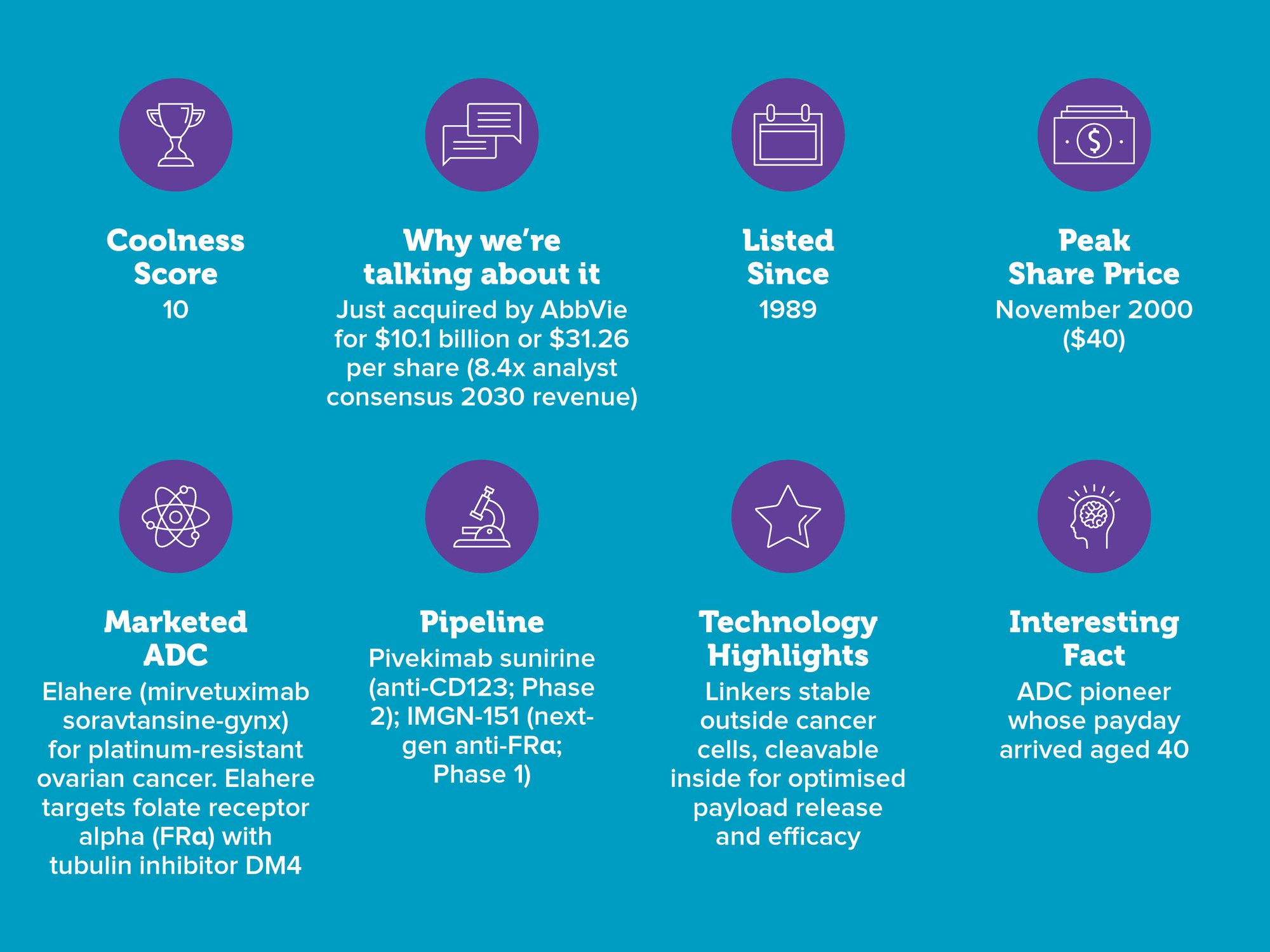

Forty-year old ImmunoGen, which was working on first-generation ADCs in the 1980s, saw its shares reach a ten-year high in 2023 after Elahere, which received accelerated approval in November 2022, showed a 35% reduction in risk of disease progression or death versus chemotherapy in some forms of resistant ovarian cancer. That was also enough to attract AbbVie with its $10 billion; the drugs giant thereby leapfrogs onto the market, carving a trail for its own ADC pipeline, which includes Phase 3 lung cancer candidate telizotuzumab vedotin.

Roche’s Kadcyla (which links antibody Herceptin to cytotoxic agent emtansine) uses ImmunoGen’s targeted cytotoxin technology. Oxford BioTherapeutics is another collaborator; it couples new targets with ImmunoGen’s ADC linker-payload technology, which features, along with a DM4 payload, in OBT’s lead Phase 1 program.

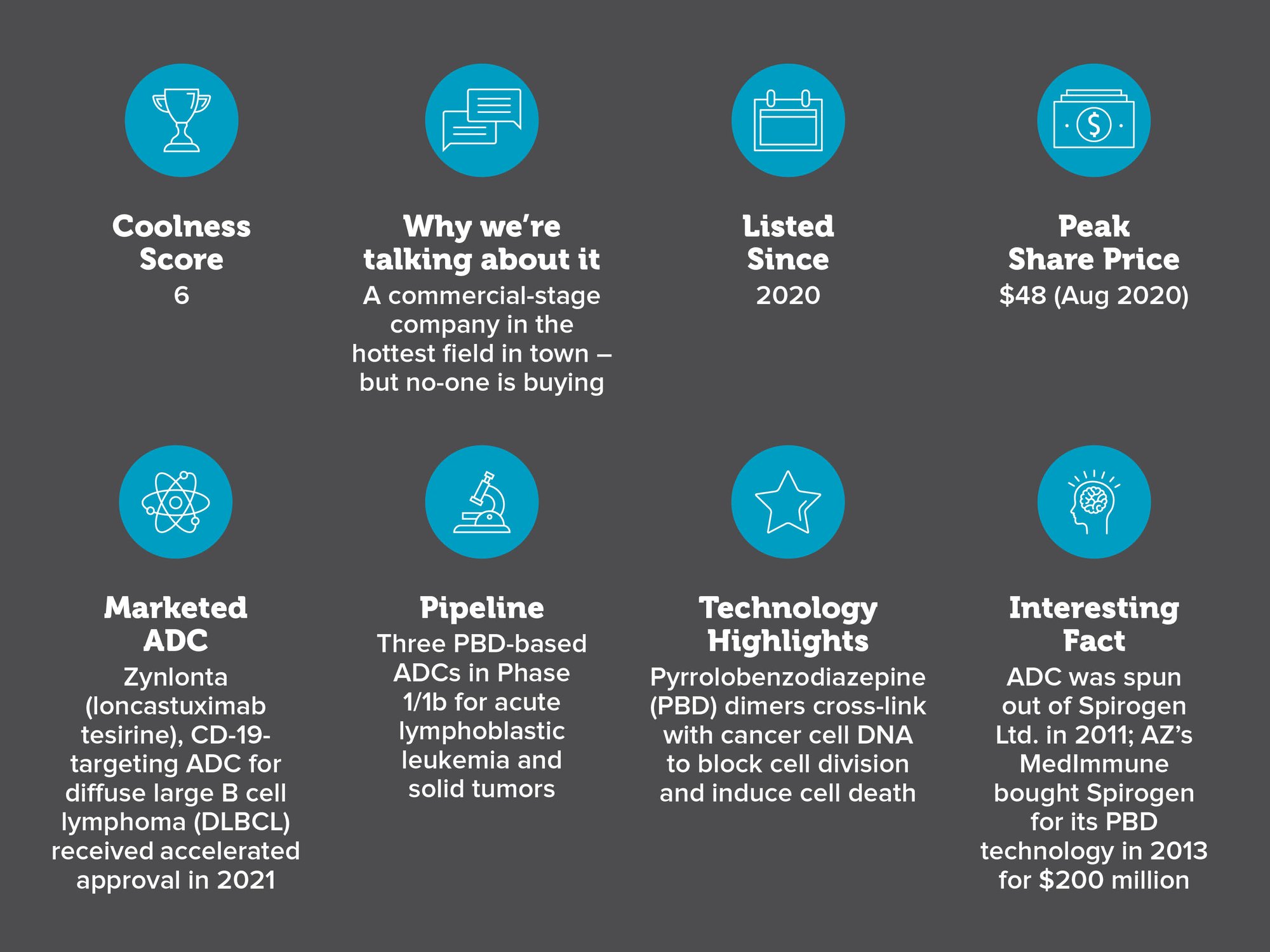

Zynlonta sales have fallen – along with ADC’s shares – due to a failed Phase II combination trial with rituximab and competition from Roche’s Polivy, which is also approved for DLBCL. Phase 2 Hodgkin’s lymphoma candidate camidanlumab tesirine was shelved following an FDA filing rebuttal in late 2022 and a failed combination study with Keytruda.

Two other ADCs developed using the PBD-based payload technology have failed: Seagen’s vadastuximab and Rova-T, the one-time crown jewel of AbbVie’s $6 billion Stemcentrx acquisition in 2016.

Doubts over the technology’s effectiveness may explain why no-one has snapped up ADC Therapeutics (yet).

ADCs are the main growth engine for this mid-sized Japanese pharma, whose overseas sales surpassed domestic for the first time in 2022.

The company expects its oncology business to grow to $6 billion (JPY 900bn) in 2025, making up almost half the group’s overall revenues.

Were its crown jewel ADCs not already spoken for, Daiichi Sankyo would be a big mouthful, even for cash-rich Western big pharma.

www.daiichisankyo.com/rd/pipeline/