ADC Market Landscape

Big pharma are dishing out billions to buy or license them: in 2023, Pfizer paid $43 billion for Seagen, AbbVie stumped up over $10 billion for ADC pioneer ImmunoGen, and Merck forked out $4 billion up-front – and potentially up to $22 billion – to Daiichi Sankyo for a share of three of its ADCs. The action continues in 2024, with Johnson & Johnson’s $2 billion cash deal for Ambrx Pharma and Roche’s licensing deal with Suzhou, China-based MediLink Therapeutics in January.

The total value of ADC-focused M&A and partnership activity was close to $100 billion in total in 2023 – more than three times the value of similar deals in 2022, and nine times the deal tally in 2019, according to Evaluate Pharma.

Despite a chock-full ADC pipeline, accessing even early-stage assets is now tricky for all but the biggest and richest: one biotech CEO in September declared being “priced out” of ADC licensing negotiations despite having raised close to $200 million.

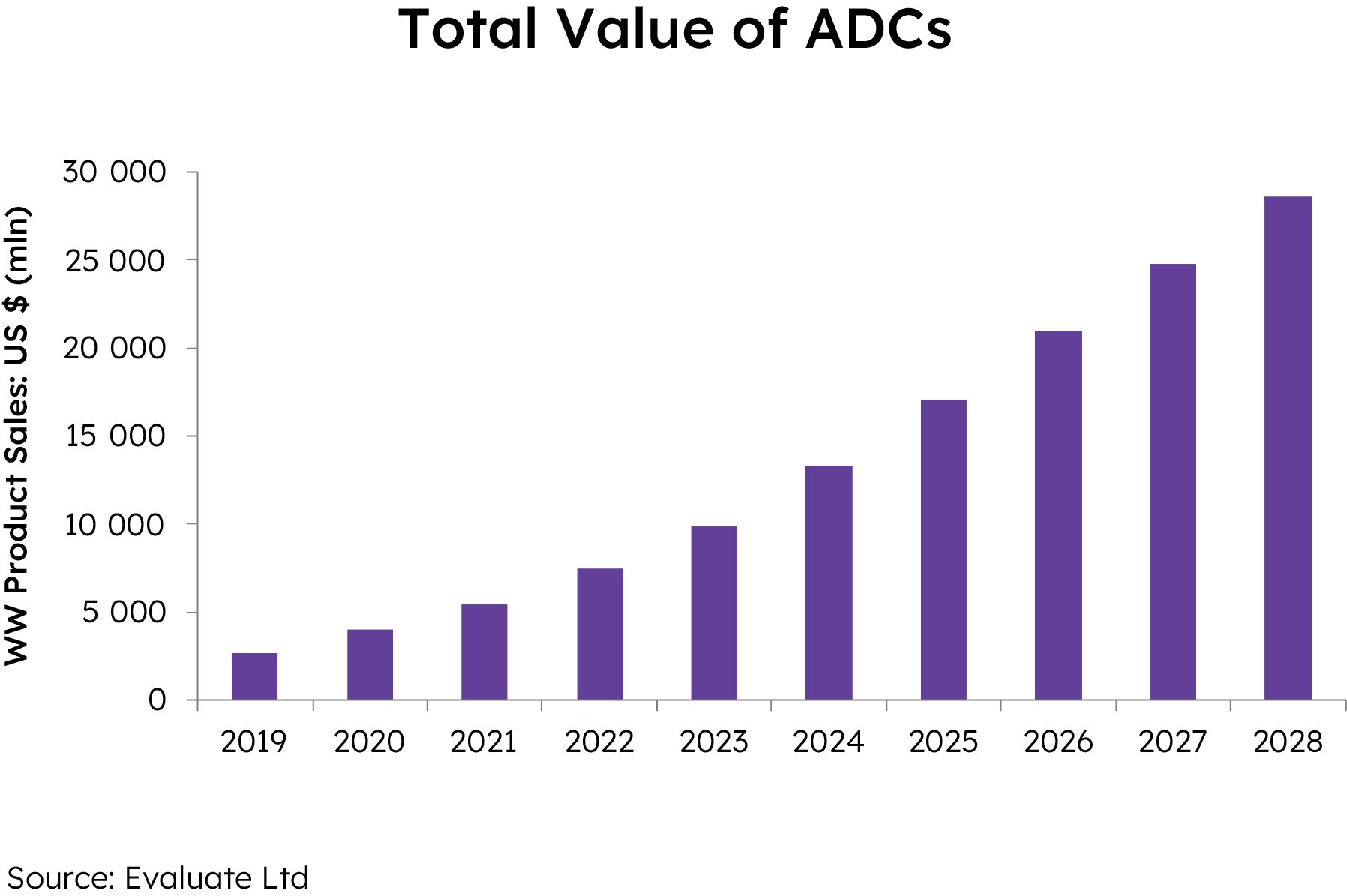

What’s the fuss? ADCs combine the specificity of monoclonal antibodies with the potency of cytotoxic drugs to create what is in effect precision chemotherapy. The scientific and commercial promise are real: over a dozen ADCs are approved in the US. The biggest, Daiichi/AstraZeneca’s Enhertu, sold more than $1.6 billion in 2022 and is forecast to top $9 billion by 2028, according to Evaluate consensus forecasts. By then, the ADC category – including development candidates with sales forecasts – will be worth almost $30 billion.

Roche tops the ADC pile in 2023, with breast cancer ADC Kadcyla and lymphoma therapy Polivy bringing in over $3 billion in combined annual sales. But Daiichi Sankyo is forecast to take the lead by 2028, with close to $10 billion combined sales from Enhertu and Phase 3 hopeful datopotamab deruxtecan whose positive results in September take it close to regulatory submission. Both are partnered with AstraZeneca. Pfizer will be in second place in 2028, thanks to the “goose laying the golden eggs” – aka Seagen.

TOP FIVE COMPANIES BY COMBINED ADC SALES, 2023 AND 2028

Company

2023 ADC sales ($m)

2028 ADC sales forecast ($m)

Daiichi Sankyo

2,459

9,998

Pfizer/Seagen

1,952

5,277

Gilead

1,071

3,423

Roche

3,072

3,128

AstraZeneca*

295

1,702

*shares of Daiichi’s Enhertu and datopotamab

2023’s European Society of Medical Oncology (ESMO) congress was a-buzz with ADC tales, including a doubling of median survival shown by Astellas/Seagen’s Padcev in combination with Merck’s checkpoint inhibitor Keytruda in advanced bladder cancer.

The ADC pipeline is bursting with next-generation hopefuls plus new indications and combinations for existing therapies. There are over 150 clinical stage programs, including almost forty in Phase 2 and a dozen in Phase 3, according to BioMedtracker. Current development-stage programs with forecasts attached – typically the most advanced – will be worth close to $6 billion by 2028, according to Evaluate.

The idea behind ADCs – using antibodies’ targeting ability to ferry toxic meds to cancer cells – sounds simple enough. But finding the right combination of antibody, linker technology and warhead is difficult. Linkers determine how much payload can be carried (the “drug-to-antibody” ratio), and when and where it is released. Dropping the payload early, or off-target, will limit ADC efficacy (at best) or, at worst, damage healthy tissue.

The choice of linker and payload matters: Enhertu and Kadcyla use the same antibody, trastuzumab (sold separately as Herceptin). Yet their linkers and payloads differ. Enhertu, which carries chemotherapy drug DXd via a cleavable linker, is more effective at prolonging survival than emtansine-carrying Kadcyla, with its non-cleavable linker. Hence the $7 billion gap in peak sales: ten-year-old Kadcyla is expected to max out at just over $2 billion this year.

Pfizer had to re-design and relaunch the first ever ADC, Mylotarg (approved in 2000) due to toxicity resulting from an unstable linker. AbbVie paid nearly $6 billion for Stemcentrx in 2016, but star ADC Rova-T failed two years later. So AbbVie’s played it safer with ImmunoGen, whose first ADC, Elahere, received conditional approval in 2021 for ovarian cancer and is growing fast.

Hiccups continue: GlaxoSmithKline withdrew multiple myeloma drug Blenrep (belantamab mafodotin) from the US market in late 2022 after a failed confirmatory trial (though it’s having another go), and ADC Therapeutics’ CD-19 targeting Zynlonta, which nabbed an accelerated approval in 2021 for B-cell lymphoma, this year failed a Phase 2 combination trial with rituximab due to adverse events. Zynlonta is also being hit by competition from Polivy.

Eli Lilly and Bristol Myers Squibb have kitted up with ADCs and linker technologies via smaller acquisitions. In June 2023, Lilly paid a few million for German start-up Emergence, whose pre-clinical Nectin-4 targeting ADC uses a linker technology licensed from Lyon, France-based Mablink Bioscience. So the big pharma bought Mablink too, with its platform promising targeted payload release and a higher drug-to-antibody ratio. Also in 2023, Bristol Myers Squibb paid $23 million for access to Tubulis’ conjugation technology and another $100 million for South Korean firm Orum Therapeutics’ Phase 1 antibody-protein degrader conjugate. In December, the Big Pharma plunged into ADCs deeper still, with an $800 million up-front deal for ex-China rights to SystImmune’s Phase 2 bispecific ADC targeting EGFR and HER3. GSK is also dipping its toes back into ADCs, with an $85 million up-front licensing deal in December 2023 for ex-China rights to Hansoh Pharma’s ovarian/endometrial tumor ADC. The drug is in Phase 1 trials in China, another region enjoying an ADC boom.

In other Western-Chinese ADC tie-ups, BioNtech in April 2023 handed over $170 million to Shanghai-based DualityBio for access to two pipeline ADCs including a HER2-targeted topoisomerase inhibitor-based ADC in Phase 2, and six months later licensed a HER3-directed ADC from MediLink. AstraZeneca licensed a pre-clinical ADC from Shanghai-based LaNova Medicines and Pfizer paid $53 million for Nona Biosciences’ mesothelin-targeted ADC in the final weeks of 2023 – a program co-designed by MediLink. (Nona is owned by Hong-Kong-based HBM Holdings Ltd.)