Money, Markets and M&A

At time of writing, the year is not quite over but it is probably safe to say that expectations of a sustained recovery in biotech stocks in 2024 failed to materialise.

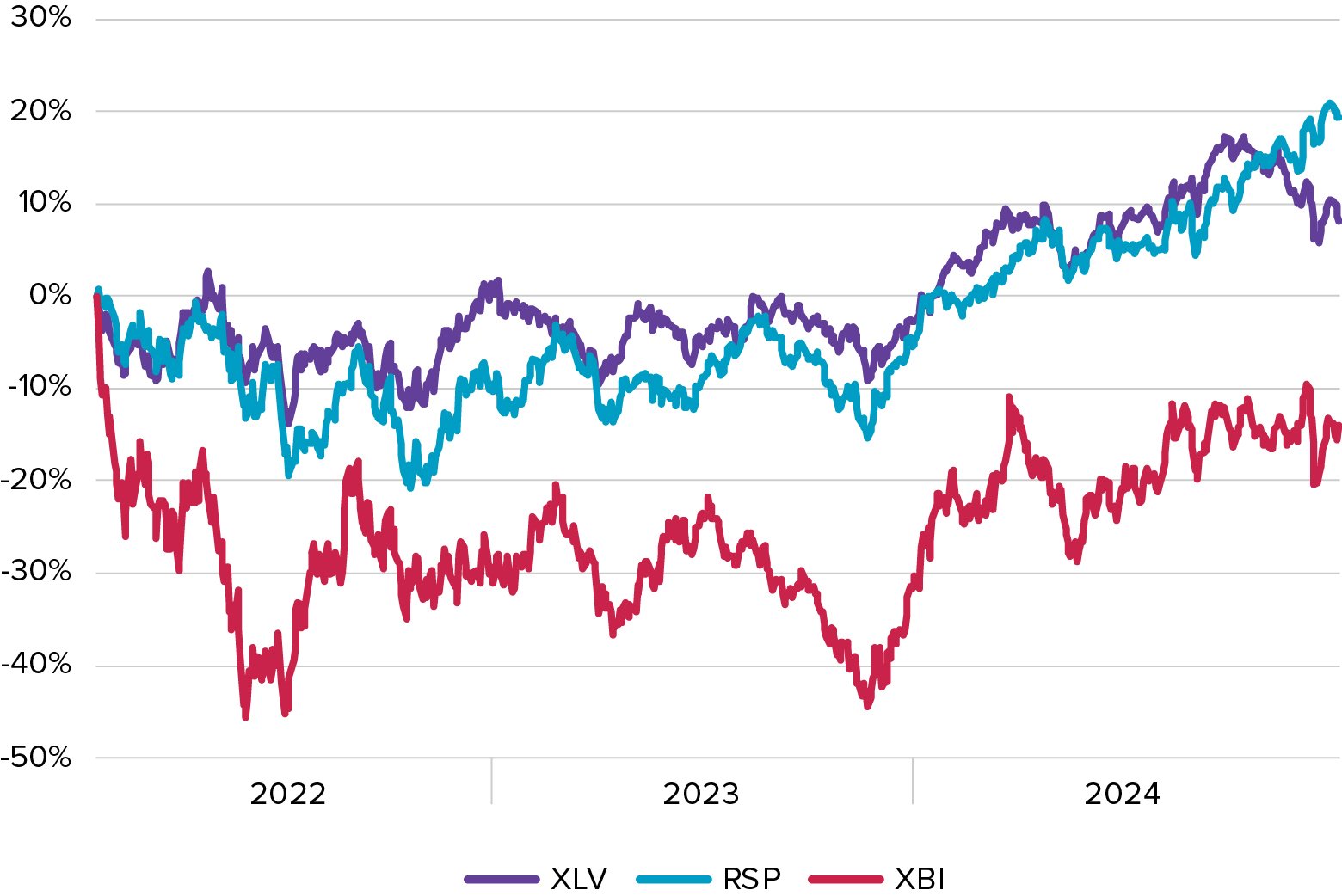

True, the closely watched index that tracks US biotechnology stocks, the XBI is, in early December marginally higher than at the start of the year. But over the second half of 2024 the XBI essentially moved sideways. Ongoing concerns about inflation and interest rates, which look likely to remain higher for longer, make risky drug development stocks an unappealing prospect for non-specialist investors.

The situation was exacerbated in November by Trump’s leftfield choices for running US healthcare. The chart here shows how this issue hit more established, larger biopharma companies than small biotechs. The XLV, a broader index that encompasses the wider healthcare sector, remains below its pre-US election peak. President Trump’s plans for the Affordable Care Act, Medicare drug price negotiation and tariffs on imports from abroad are all keenly awaited and how they play out will be big themes for healthcare in 2025.

It is this latter issue – Trump’s threat to impose tariffs on imports from countries around the world – that is prompting concern in the financial markets about persistently high inflation and interest rates. This is not good news for cash-hungry sectors like biotech.

Despite this, investors are not completely pessimistic about 2025. Sentiment is seen improving next year, even for smaller biotechs, along with access to capital. The glacial pace of improvement feels locked in, however. A pickup in M&A, which many are predicting, should help attract non-specialist investors back to biopharma. But with so much uncertainty around the new Trump administration’s stance on healthcare, there are also plenty of reasons for caution.

Ongoing concerns about inflation and interest rates, which look likely to remain higher for longer, make risky drug development stocks an unappealing prospect for non-specialist investors.

Stock market performance

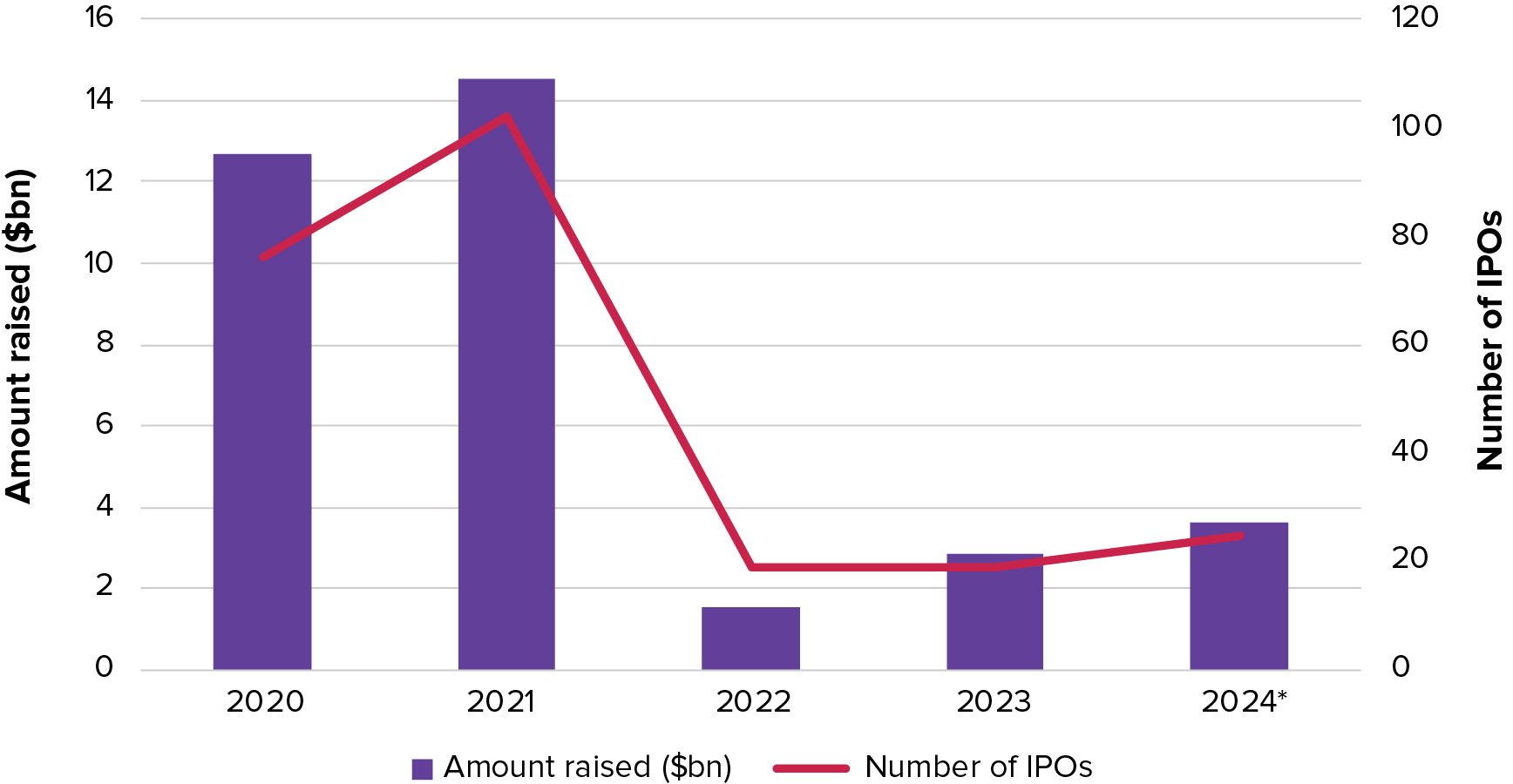

The slow return of the IPO market from 2022’s nadir continues.

While the US election caused flotations to pause in late 2024, as companies and their backers chose to avoid any potential volatility around the outcome, the pace is expected to pick up again.

With the markets effectively closed for so long, there is a huge amount of pent-up demand sitting in the private world. The equity markets can provide the sort of growth capital beyond the means of the venture world, a world that has had to support many portfolio companies for much longer than desirable. But while many predict that 2025 will see another uptick in these IPO statistics, few are predicting the flood gates to suddenly open.

The equity markets are skittish, and blow ups like BioAge in early December do not help improve biotech’s reputation. BioAge came to market in October 2024 with a high-profile mid-stage obesity candidate that was derailed by toxicity concerns only two months after floating. In the opening months of 2025 only the safest bets, and those heavily supported by existing investors, will make it onto the stock market. Market conditions need to improve for that situation to change, and it is hard to see that happening until the Trump administration is in place and laying out firm policy directions.

All of this refers to the US IPO markets, of course; Europe has not seen a notable biotech listing, outside of the tiny regional markets in Scandinavia, for years. The continent lacks a deep pool of specialist investors which, combined with a more risk averse culture, erases any prospect of a local listing for private European biotechs. They will continue to look to the US for access to the capital markets in 2025.

The slow return of the biotech IPO

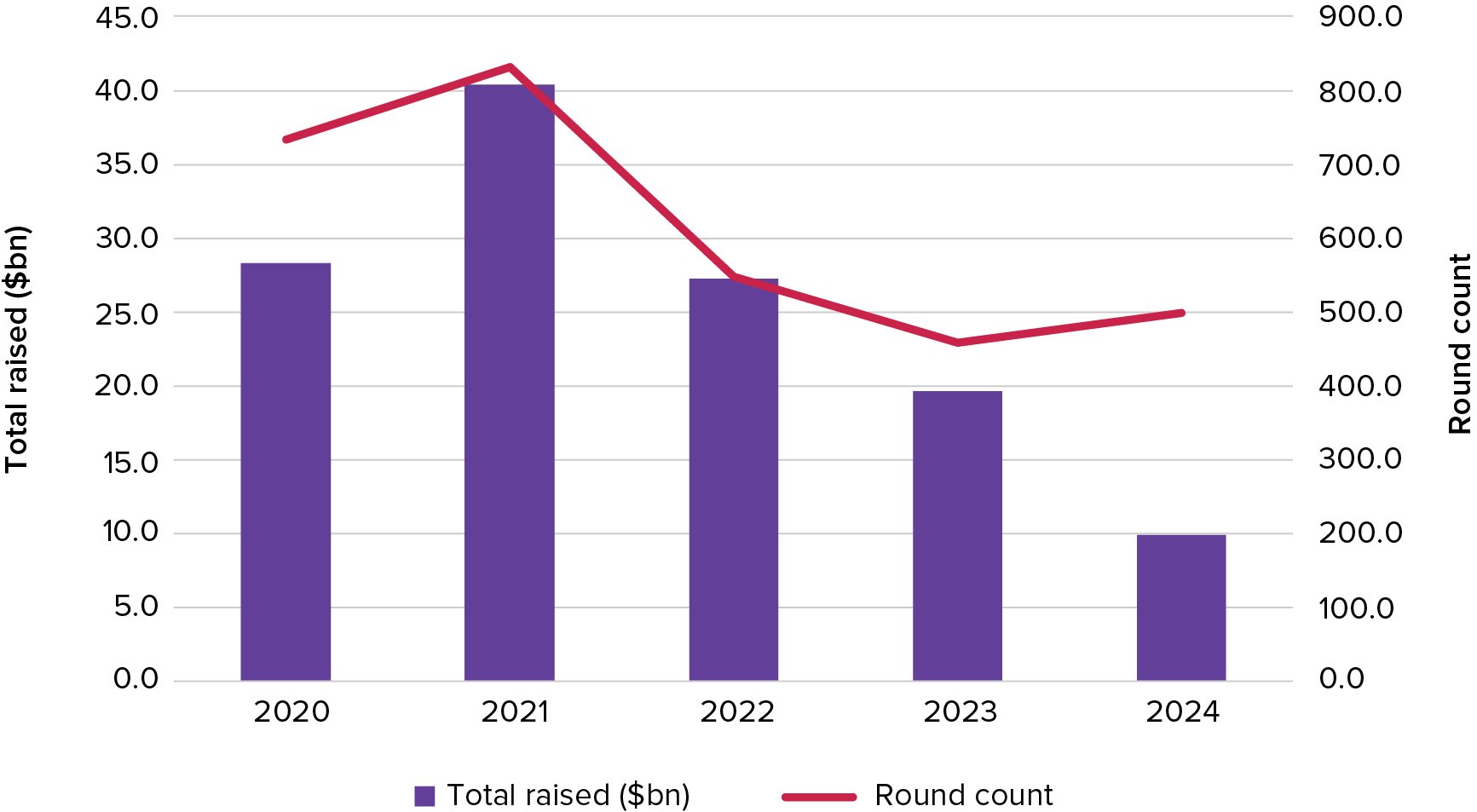

Private investors are entering 2025 in a more optimistic mood, suggesting that the climb out of 2023’s trough is continuing.

Substantial funds are being raised by the most successful investors in the US and Europe. And the most appealing portfolio companies are being bestowed with large funding rounds.

The bursting of the pandemic bubble caused equity markets to close and prompted buyers to walk away from frothy valuations, scenarios that created a difficult exit environment for venture firms. But with the IPO market opening, albeit slowly, and a string of takeouts emerging in the private world, venture investors are seeing more opportunities to pass on their investments.

Venture is increasingly becoming a world of haves and have nots, however. Money is being concentrated in fewer hands, a trend that has been developing for some years but shows no sign of reversing. New company creation is a number to watch in 2025, as venture investors continue to seek safety in numbers and create broad syndicates.

In terms of where the money is flowing, the therapy areas driving the sector’s top line growth, detailed in earlier sections of this report, will remain in favour. Immunology and inflammation, metabolic diseases, antibody drug conjugates, radiopharmaceuticals, to name a few hot areas.

Venture capital: another down year?

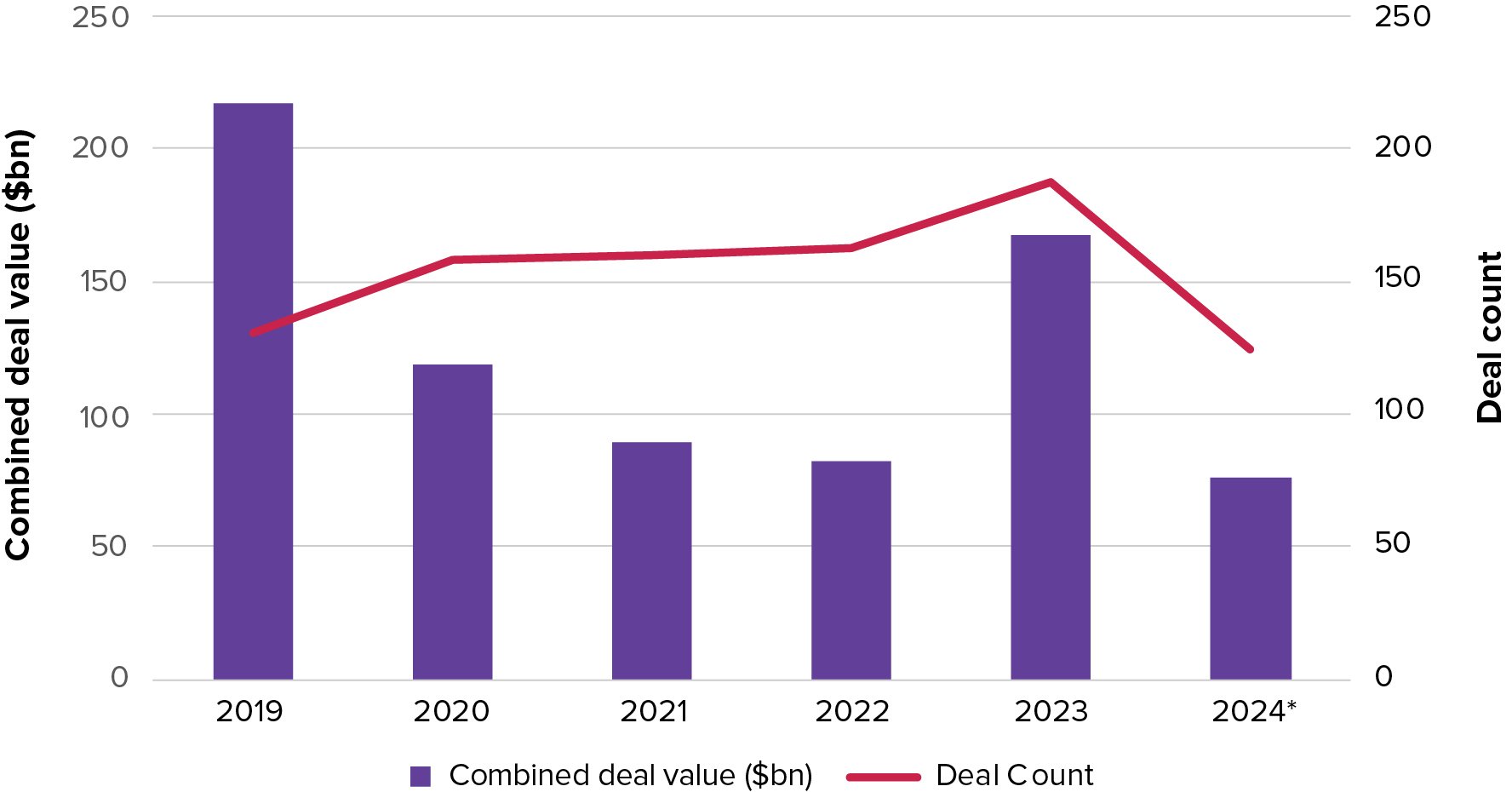

An absence of M&A has not helped the downtrodden biotech sector in 2024.

The data here concern full company takeouts, but all sorts of dealmaking has been subdued, even product licensing deals. Much blame has been laid at the feet of the Federal Trade Commission, whose hawkish stance has caused caused boardrooms to rule out moves that might attract scrutiny and suck time and money.

This is one area where the new Trump administration spells good news for biopharma, with a complete change in stance expected. In fact, many hopes for a sector pick up in 2025 rest on an increase in dealmaking.

Again, what exactly might transpire at the new Trump administration is unclear. But it is undeniable that numerous large developers need pipeline expansion. This makes an M&A uptick next year almost inevitable, as big pharma boardrooms come under pressure to deliver long term growth.

Biopharma company takeouts