Innovation and Regulation

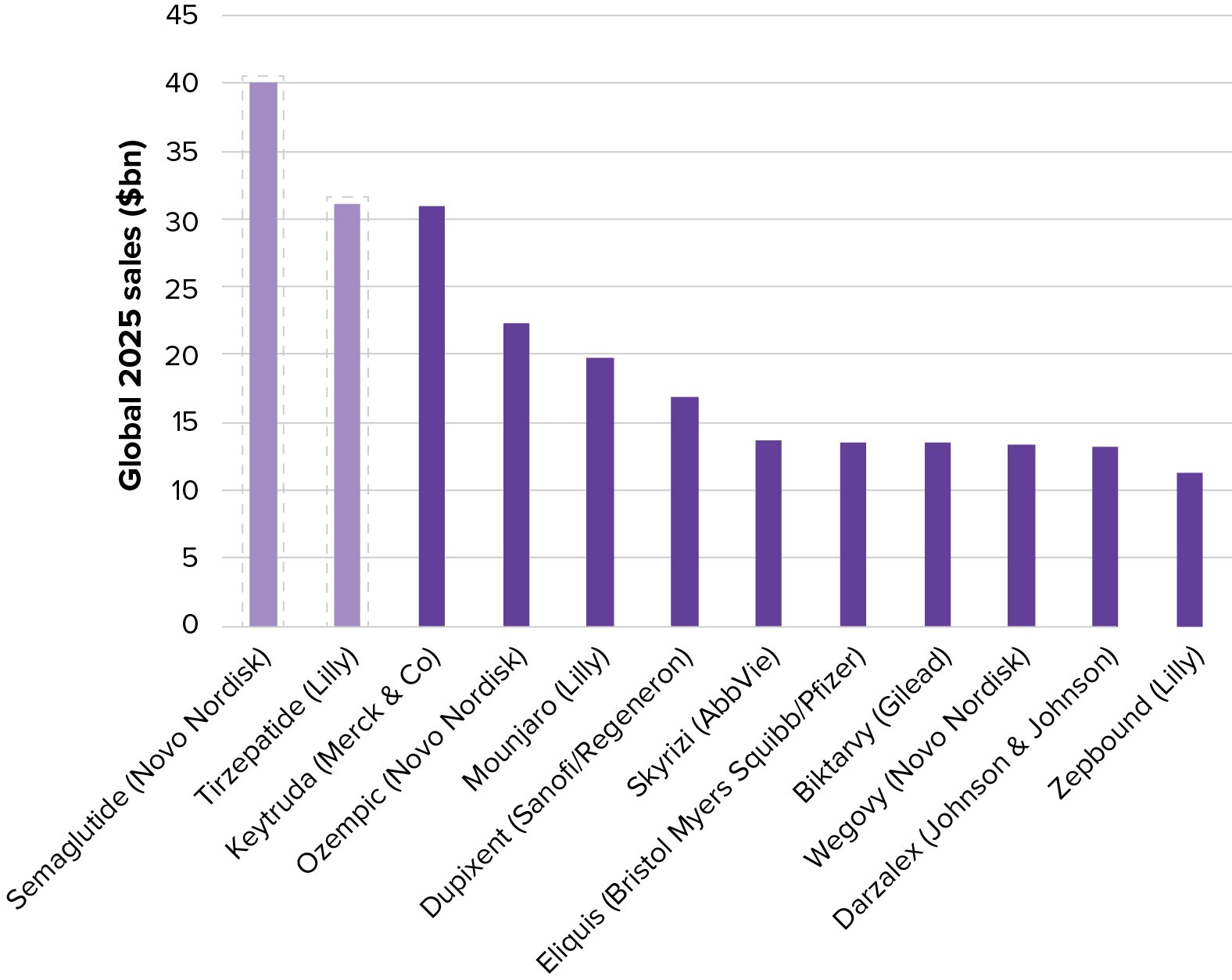

On one measure Merck & Co’s blockbuster cancer treatment, Keytruda, is set to retain its ranking as the world’s biggest selling product next year.

A look at sales by generic name, however, reveals the extent to which the incretin class, also known as GLP-1 analogues, has come to dominate the top table. Novo Nordisk’s semaglutide, sold as Ozempic for type 2 diabetes and Wegovy for obesity, and Lilly’s tirzepatide, respectively sold as Mounjaro and Zepbound, are on track to generate more than $70bn in combined sales in 2025, according to Evaluate Pharma’s consensus forecasts.

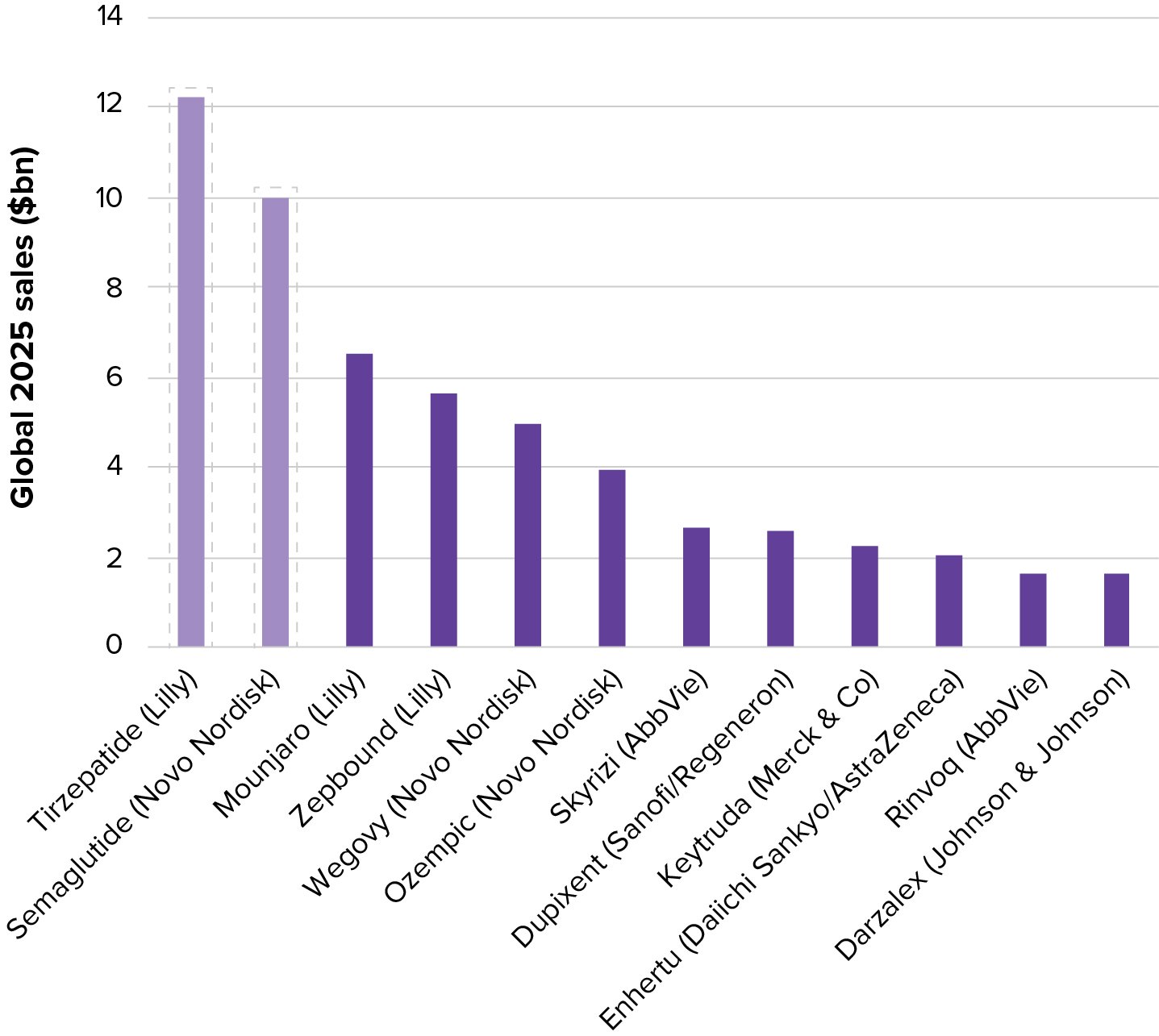

These four products also top the table of fastest growing drugs, shown in the second chart (next page). For Novo and Lilly, one of their main priorities in 2025 will be keeping up with demand, and meeting expectations of both patients and investors. Make no mistake, the growth of this field is vast in terms of both size and speed, exemplified by Zepbound’s launch statistics. Sales of the Lilly blockbuster are forecast to double in 2025 on the previous year, to $11.3bn. It was only approved in obesity at the back end of 2023.

Sales of Keytruda, meanwhile, are projected to peak in 2025. A subcutaneously administered version of the anti-PD-1 antibody will be filed with regulators next year, a project designed to extent the franchise’s life as loss of exclusivity approaches. Bristol Myers Squibb’s similarly acting Opdivo, which has been pushed out of the top 10 for the first time in several years by the incretins, is pursuing a similar strategy. Its subcutaneous formulation could be launched next year.

Elsewhere among the top 10 mega-blockbusters are products that have dominated both of these tables for several years thanks to approvals in a wide range of autoimmune and inflammatory disorders. Sanofi and Regeneron’s Dupixent for example, which is indicated for six settings included atopic dermatitis and allergic asthma.

Standing out among the fastest growing drugs is Enhertu. The antibody-drug conjugate is leading a new wave of agents to emerge in this modality, with impressive efficacy in breast and lung cancers demonstrating the potential of targeting highly toxic chemotherapy.

Top selling drugs in 2025

Top new sales: drugs

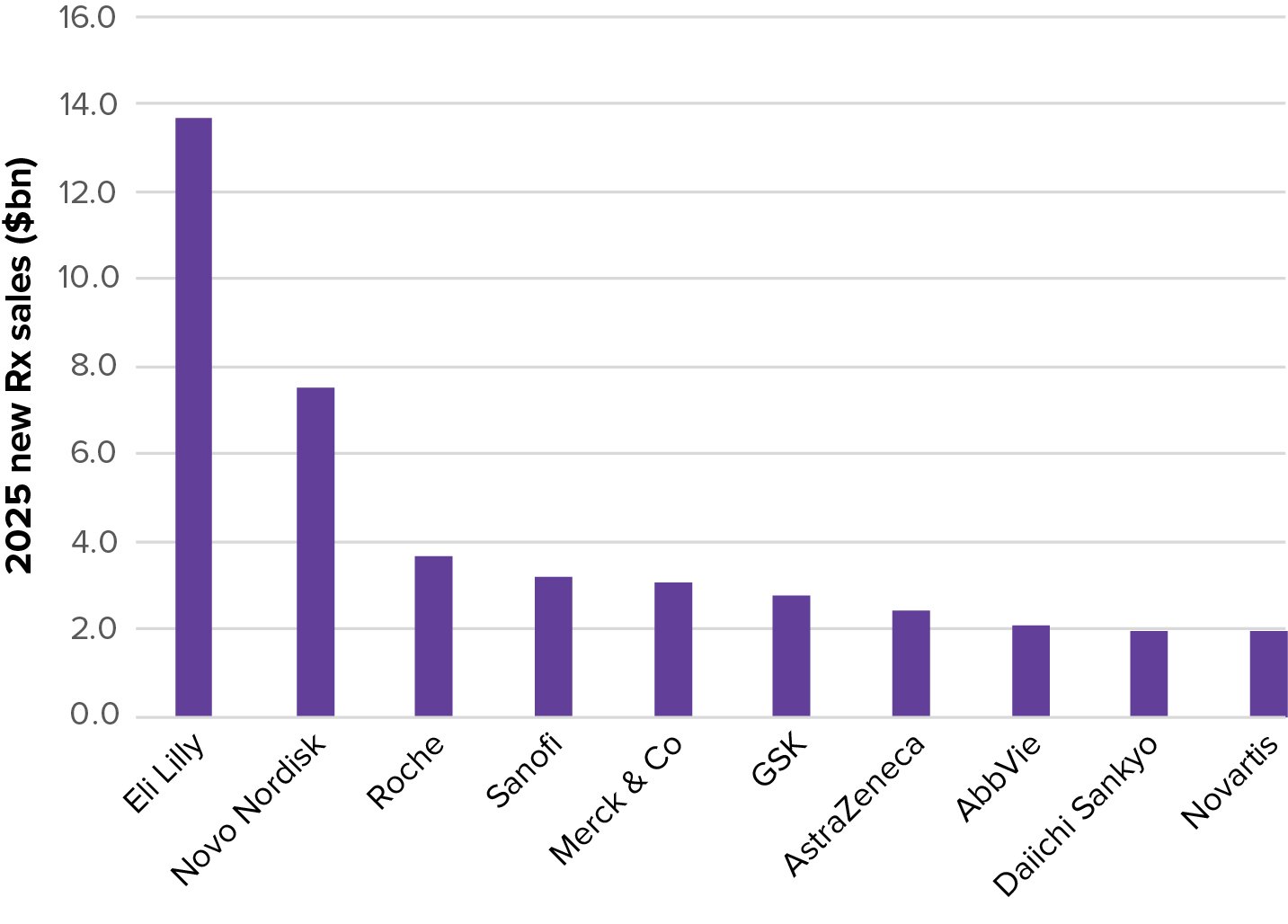

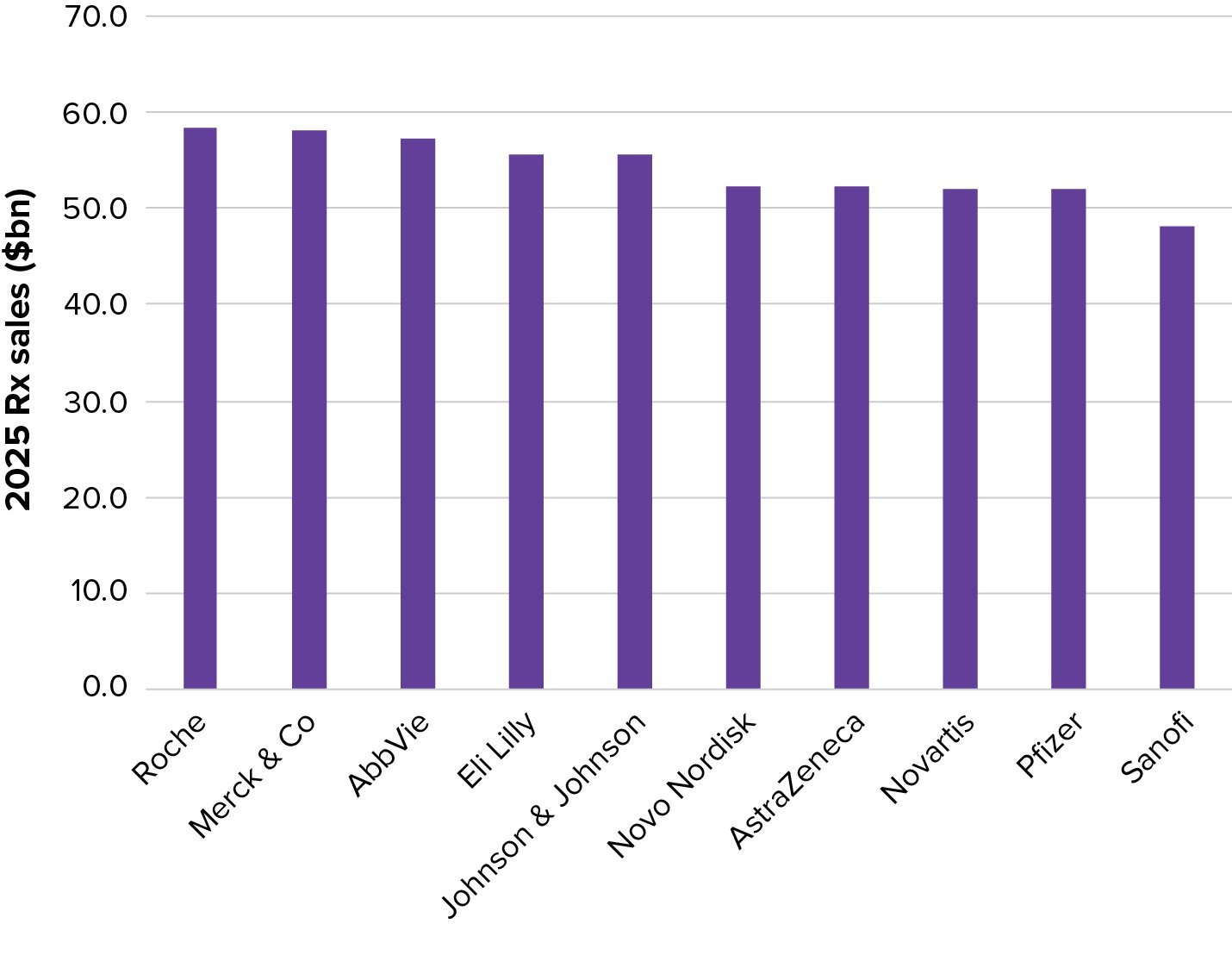

Ballooning incretin sales are set to catapult Lilly and Novo up the league tables next year, in this analysis of the world’s biggest pharma companies ranked on revenues.

But while these two groups lead the pack in sales growth in 2025, neither are placed in the top three drug makers by total prescription sales.

Lilly is on track to end 2024 as the 11th largest drug company by prescription sales; by the end of 2025 current forecasts put it in fourth position. Novo Nordisk is seen climbing from 10th to sixth in the same period. The numbers throughout this report are drawn from Evaluate Pharma’s consensus forecasts, which are based on models built by equity analysts.

It is almost inevitable that Lilly and Novo Nordisk will climb further up these ranking in subsequent years. But for now, Roche is predicted to top the table in 2025, retaining its ranking as the largest drug maker by prescription sales for a second year. The Swiss company’s pole position is somewhat surprising given that none of its products feature in the previous biggest drugs analyses. The pharma giant has breadth of portfolio, however, with several blockbusters just outside the top 10; eye disease therapy Vabysmo only narrowly missed out on a place in the fastest growing drugs table.

Another interesting name in the top growth table is GSK, a company that has struggled in recent years to convince investors about its prospects. Impressive growth is projected next year across its large vaccines and HIV business, and a couple of important new drug approvals are on the slate for next year. The potential arrival of a vaccine sceptic in an influential US government role, however, raises the prospect of turbulence ahead for the UK company.

Another group with clouds on the horizon is Pfizer, which has been criticised for failing to capitalise on its pandemic windfall. With sales of its Covid-19 vaccine Comirnaty continuing to shrink, the former highflier will see its global ranking fall next year from 5th to 9th place, according to current sales forecasts.

Biggest drug makers by prescription sales in 2025

It is almost inevitable that Lilly and Novo Nordisk will climb further up these ranking in subsequent years.

Top new sales: companies

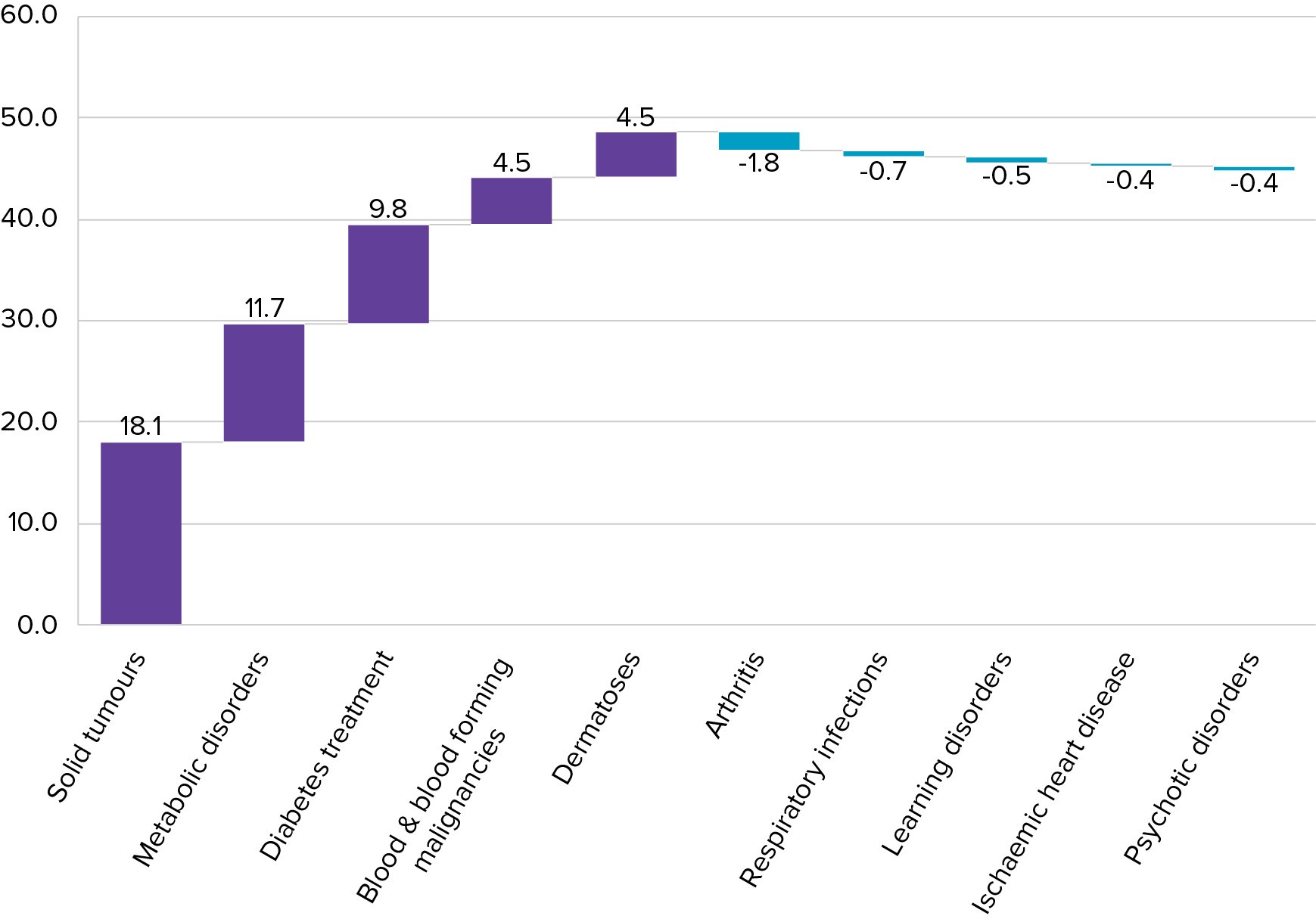

Evaluate Pharma is forecasting an $82bn increase in pharmaceutical product sales next year, the largest jump since the Covid-19 pandemic, with combined industry revenues topping $1tn for the first time.

The graph here shows which therapy areas are acting as growth drivers and brakes.

Among the drivers, cancer is ostensibly leading the way with the incretins coming behind. But with diabetes and obesity falling into two separate therapy areas, the dominance of the incretin class is revealed once again if the metabolic space is considered as one.

The blood cancer therapy area features products like Darzalex and Carvykti, sold primarily for multiple myeloma by J&J, while dermatoses is dominated by large franchises mentioned earlier like Dupixent and Skyrizi. The latter, sold for psoriatic conditions and inflammatory bowel disease, now counts as AbbVie’s most important growth driver, with future sales forecast to top $20bn.

Loss of exclusivity explains much of the contraction seen among the growth brake categories. Arthritis for example is contracting as sales of AbbVie’s Humira are replaced by sales of lower cost biosimilars. The learning disorders field is being hit by the patent expiry of ADHD medicine Vyvanse. Respiratory infections, of course, reflects the end of Covid-19, with sales of vaccines and antivirals expected to dip again next year, as the pandemic’s impact on the sector continues to fade.

It should be noted that this analysis only includes forecasts where covering analysts have assigned specific indications for the sales, so the $1tn figure cited earlier should not be interpreted as a projection for total biopharma sector sales in 2025.

Therapy areas: growth drivers and brakes

Obesity might suck much of the sector’s attention next year, but 2025 is unlikely to see any novel weight loss approvals, at least not in the US.

The wild card here is Novo Nordisk’s cagrisema, which has yet to yield phase 3 data at time of writing and is therefore included among the most valuable R&D projects, rather than biggest launches. With a speedy filing and a priority review voucher perhaps a 2025 approval is possible for cagrisema.

There is an incretin agent in this list of biggest launches, however: Innovent’s mazdutide. This GLP-1 and glucagon receptor agonist was originated at Lilly but licensed out while the US group focused on tirzepatide. The Chinese developer is seeking approval in its home market; 2030 sales of $1.3bn might not move the needle for a metabolic agent in the West, but for the Chinese market this is a substantial sum.

Vertex’s latest cystic fibrosis offering is ranked as the biggest 2025 approval decision, in potential sales terms. The success of the company’s existing CF franchise means another commercial hit is expected from this triple therapy. Vertex’s second 2025 regulatory decision sits with suzetrigine which, if approved, would count as the first novel pain mechanism to reach the market for decades. Acute pain is the indication currently under regulatory review, and data in other neuropathic pain settings are keenly awaited next year.

The FDA’s decision on the second ADC to emerge from Daiichi and AstraZeneca’s partnership is another big event; the partners withdrew an initial filing in lung cancer in 2024. Huge expectations sit behind the project, which targets TROP2 to deliver its toxic payload.

Insmed and Cytokinetics carry the torch for smaller, independent developers here, although both have a nervous wait until the end of 2025 for their decisions. The former is preparing to file brensocatib in the lung disease bronchiecstatis, while Cytokinetics is approaching the cardiology world with aficamten, a treatment for hypertrophic cardiomyopathy.

Biggest potential drug launches of 2025

Product

Companies involved

Description

Status

2030e sales ($bn)

Vanza Triple

Vertex

Triple combination CFTR modulator for cystic fibrosis

PDUFA January 2, 2025; EU approval Q2'25

8.3

Datopotamab Deruxtecan

Daiichi Sankyo/AstraZeneca

Anti-Trop2 ADC for lung and breast cancers

US and EU decisions due Q1'25

5.9

Suzetrigine

Nav1.8 channel blocker for acute and neuropathic pain

PDUFA January 2025

2.9

Aficamten

Cytokinetics

Cardiac myosin inhibitor for hypertrophic cardiomyopathy

US and EU decisions due Q4'25

2.8

Brensocatib

Insmed

DPP1 inhibitor for neutrophil-mediated diseases

Filing planned by YE'24 (priority review expected)

Tolebrutinib

Sanofi

BTK inhibitor for multiple sclerosis

Filing planned before YE'24

1.4

Mazdutide

Innovent/Lilly

GLP-1 & glucagon receptor agonist for T2D and obesity

China obesity approval due H1'25; T2D due H2'25

1.3

Depemokimab

GSK

Long-acting anti-IL-5 Mab for severe allergic asthma

1.2

MenABCWY

Meningococcal A, B, C, W-135 & Y vaccine

PDUFA February 14, 2025

Nipocalimab

J&J

FcRn antagonist in broad autoimmune development programme

US and EU decisions due H1'25

Note: T2D = type 2 diabetes. Source: Evaluate Pharma. Consensus for datopotamab deruxtecan pre-dates withdrawal of US lung cancer filing.

A look at some of the most valuable R&D projects means a return to the story of incretin’s dominance, with the top four positions occupied by novel anti-obesity/type 2 diabetes agents.

Cagrisema carries huge hopes for Novo Nordisk, which hopes the dual-acting agent will give it an obesity proposition that can offer similar levels of weight loss as Lilly’s tirzepatide.

Impressive phase 2 data have triggered substantial expectations around Lilly’s own follow-on, retatrutide, which is now in a large pivotal programme. Another Lilly asset, orforglipron, is the leading contender in the race to develop an oral obesity drug; phase 3 data due later in the year count as one of 2025’s most keenly anticipated readouts. MariTide’s valuation is likely to have been trimmed since the data for this report was collected, in the wake of Amgen’s disappointing phase 2 disclosure in late November.

Elsewhere in the sector’s pipeline are two agents, batoclimab and IMVT-1402, that their developers hope will compete in the anti-FcRn space. For now this is owned by Argenyx and its hugely successful Vyvgart, though will be likely be joined on the market next year by J&J’s nipocalimab, which made the previous biggest launches table. The inflammatory disease field is set to remain a huge focus next year, with Moonlake and its highly valued sonelokimab another example of this enthusiasm.

In the last few years biopharma has shifted much attention towards immunology and, more recently, metabolic science. To some extent that has happened at the expense of oncology, although a handful of modalities within the expansive cancer field continue to attract much attention. Bispecifics is one such area, and ivonescimab a prime example. The project’s success versus Keytruda in a study conducted in China triggered much interest in the anti-PD-1xVEGF mechanism. Ivonescimab, which was discovered by Akeso and licensed by Summit, also speaks to another theme likely to continue playing out in 2025: the hunt for China-originated projects, where early-stage development can be carried out much more cheaply, and quickly, than in the West.

Note: T2D = type 2 diabetes; MG = myasthenia gravis; CIDP = chronic inflammatory demyelinating polyneuropathy; TED = thyroid eye disease. Consensus estimates for Cagrisema and MariTide pre-date clinical readouts in late 2024, both of which disappointed. Source: Evaluate Pharma.

Biopharma's valuable R&D projects

NPV ($bn)

Cagrisema

Novo Nordisk

Fixed-dose combination of amylin and GLP-1 agonists for obesity and T2D; ph3 data late 2024

87.3

Retatrutide

Eli Lilly

GLP-1, GIP and glucagon tri-agonst for obesity and T2D; ph3 data in 2026

38.6

Orforglipron

Eli Lilly/Chugai

Oral GLP-1 receptor agonist for T2D and obesity; ph3 data from late 2025

37.9

MariTide

Amgen

GLP-1 agonist & GIP antagonist for obesity and T2D; ph3 to start 2025

31.4

IMVT-1402

Immunovant/Roivant

Anti-FcRn Mab, broad autoimmune pivotal development programme to start 2025

5.3

Batoclimab

Anti-FcRn Mab; ph3 data in MG, CIDP and TED due 2025

5.8

Sonelokimab

Moonlake Immunotherapeutics

Trivalent nanobody against IL-17A, IL-17F and albumin for inflammatory disease; ph3 data from mid-2025

8.0

Olpasiran

ApoA RNAi therapeutic for elevated Lp(a) and atherosclerotic cardiovascular disease; ph2 data from 2026

7.9

mRNA-4157

Moderna/Merck & Co

Individualised neoantigen immunotherapy for melanoma; ph3 data from late 2025

5.2

Ivonescimab

Akeso/Summit

Anti-PD-1 & VEGF bispecific for lung cancer; ph3 data from mid-2025

7.2

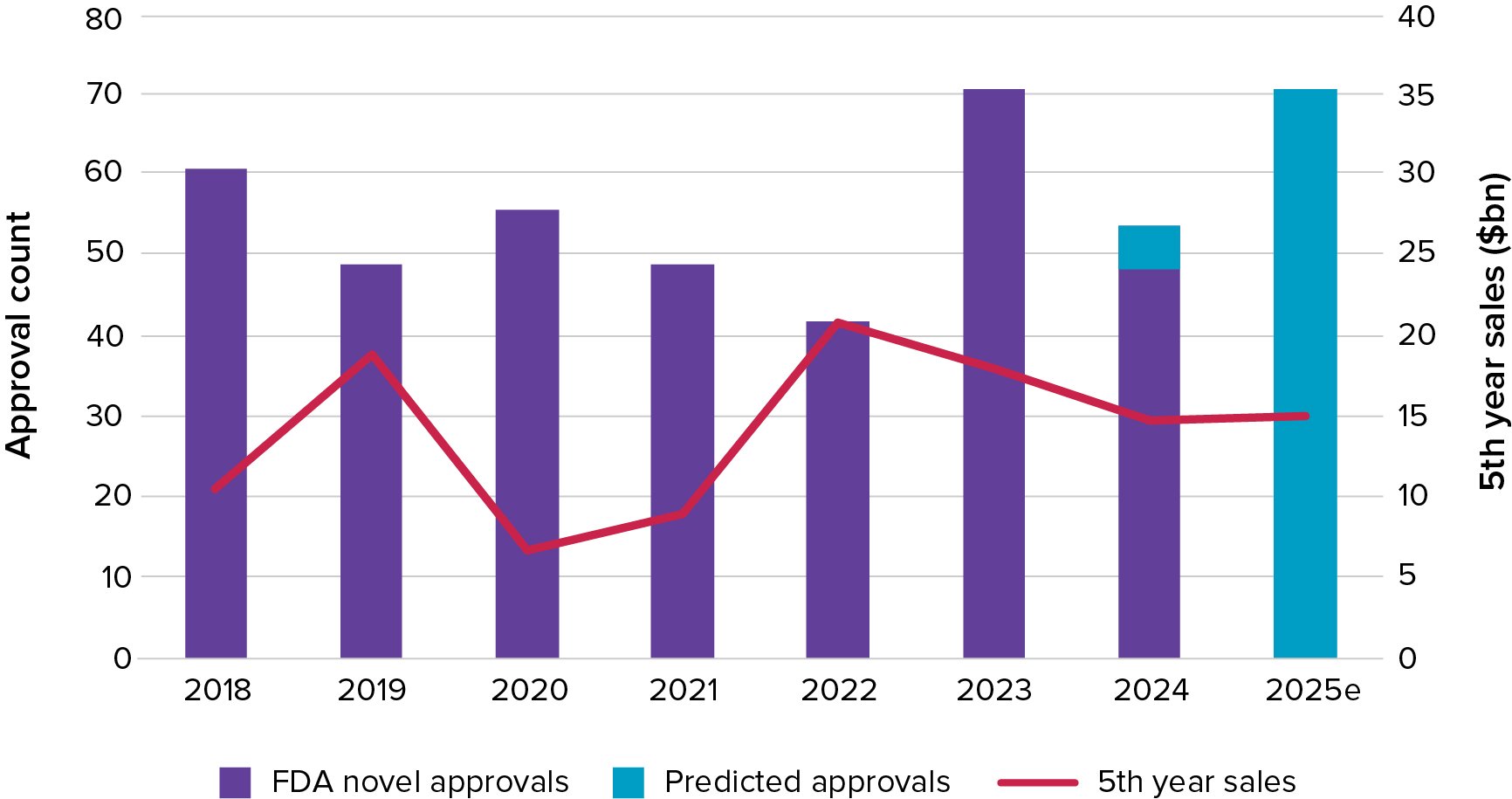

Next year holds the potential to see a historically high number of novel approvals, with Evaluate Omnium yielding 71 projects with a good chance of reaching the US market.

This includes the 10 detailed earlier which are seen as the most commercially promising. This estimate is far from set in stone, of course, with both small and large companies liable to encounter regulatory hick ups. Matching 2023’s record 71 novel approvals would be notable, however.

The chart here shows how biopharma and the FDA have filled in the hole that Covid-19 put in sector productivity. The pandemic impact can really be seen in fifth-year sales, with the classes of 2020 and 2021 showing substantially lower market potential than surrounding years, presumably as the sector focused its efforts on combating the virus.

The big unknown for the FDA regulator next year is the identity of its new commissioner, and what agenda they might pursue. Martin Makary, Trump’s pick for the job is, like the incoming President’s other nominees, a controversial name who has criticised the agency on several issues. Vaccine sceptic Robert F. Kennedy Jr. has been proposed to run the U.S. Department of Health and Human Services, which is technically in control of the FDA.

What the following years might hold for drug regulation – and the biopharma sector more widely – depends a lot on the people that end up with the top jobs in Trump’s new administration. It is also worth remembering that the Prescription Drug User Fee agreement that funds new drug reviews at the FDA must be reauthorised by the end of September 2027. The coming few years hold the potential for much turbulence at the influential regulator.

Tracking US approvals