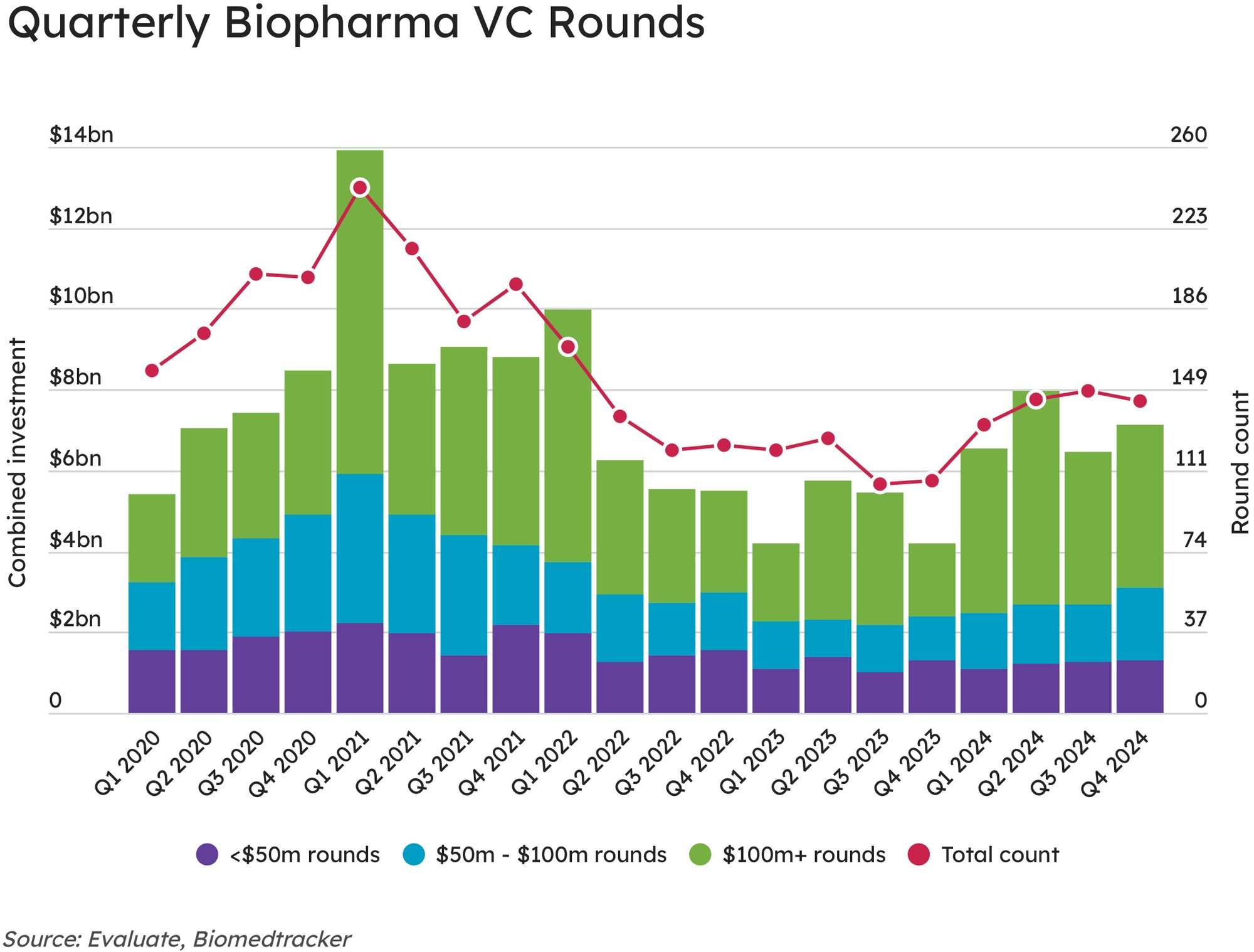

Biopharma VC Fundraising Reached Highest Total Since 2021

Evaluate Pharma data from the fourth quarter of 2024 show another period of venture capital fundraising that beat each quarter of 2023, as $100m-plus mega-rounds surged.

Venture capital fundraising by biopharmaceutical companies rose to $7.11bn in the fourth quarter of 2024, after falling to $6.46bn in Q3 from $7.95bn in Q2, according to data from Evaluate. But the year has shown a significant rebound. By the end of Q3, the 2024 fundraising total already exceeded the full-year 2023 total of $19.61bn, and with the Q4 data in hand, venture fundraising last year totaled $28.05bn, also beating the $27.27bn raised by drug developers in 2022.

Each quarter of 2024 exceeded each of the quarters in 2023.

Each quarter of 2024 exceeded each of the quarters in 2023, driven by a surge in VC mega-rounds of $100m or more. Evaluate’s data show that VC financings in the $100m-plus category totaled $3.79bn-$5.25bn during each of the four quarters of 2024, but the quarterly mega-round totals exceeded those levels during only four quarters between Q1 2020 and Q4 2023. The last quarter of 2024 included financings for two companies that raised $400m or more in venture capital – Treeline Biosciences and Kailera Therapeutics.

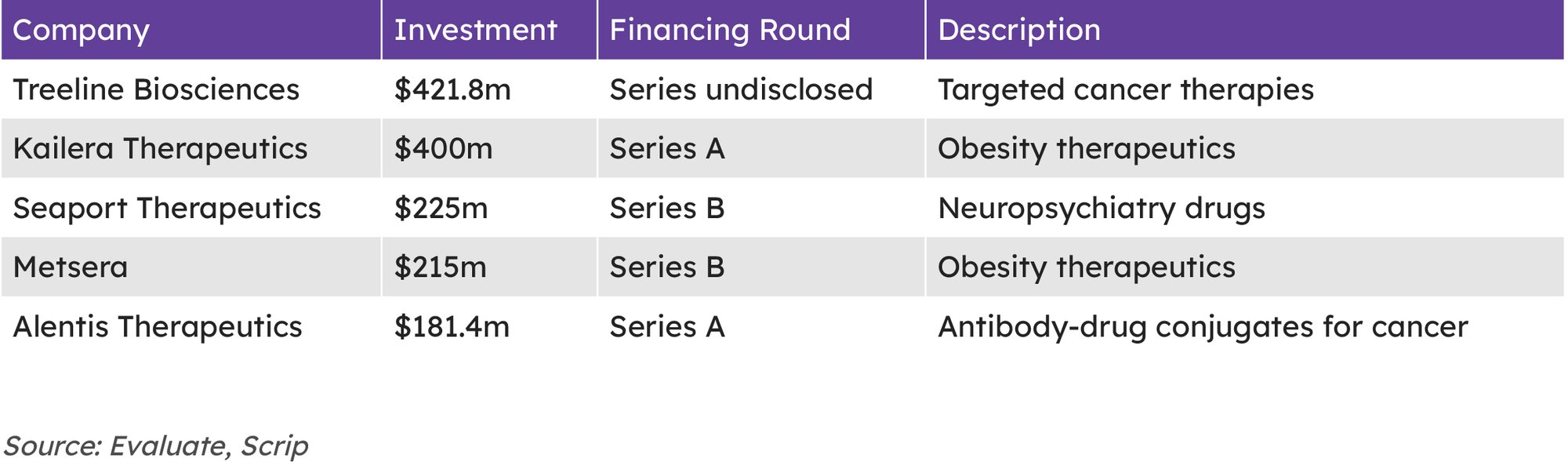

(See table alongside for Q4’s top five VC financings.)

Meanwhile, the $1.32bn in venture rounds of $50m or less and the $1.79bn in VC rounds of $50m-$100m in Q4 of this year were the biggest quarterly totals for the two categories in 2024. However, the quarterly total for VC financings of $50m or less exceeded the Q4 2024 level during 12 of the prior 19 quarters, while seven quarters exceeded the Q4 2024 total for financings of $50m-$100m.

The shift of venture capital to larger financings, usually for later-stage companies, is a reflection of the current capital markets environment in which investors are less likely to invest in riskier opportunities, such as early-stage drug development, while interest rates are high. VC and public market investors are favoring companies with clinical-stage drug candidates in therapeutic areas such as obesity and cardiovascular diseases, neuroscience, targeted oncology and immunology.

VC and public market investors are favoring companies with clinical-stage drug candidates in therapeutic areas such as obesity and cardiovascular diseases, neuroscience, targeted oncology and immunology.

If mergers and acquisitions continue at the pace and scale seen earlier in January – with Johnson & Johnson buying Intra-Cellular Therapies for $14.6bn, GSK paying up to $1.15bn for IDRx and Eli Lilly committing up to $2.5bn for Scorpion Therapeutics – that may boost investor confidence in biopharma opportunities. Even start-ups could benefit from similar business development activity, since IDRx’s and Scorpion’s lead programs were in early clinical development, and Big Pharma companies continue to seek partnerships at the preclinical stage.

The top five VC financings in Q4 of 2024 reflect the therapeutic areas of greatest interest to both Big Pharma buyers and investors – obesity, targeted cancer therapies and neuropsychiatry.

Treeline Biosciences has been quiet to date about its targeted cancer drug pipeline, but the company disclosed in a Form D filed with the US Securities and Exchange Commission (SEC) in October that it raised $421.8m, which followed two prior Form D filings with the SEC that exceeded $200m each in 2021 and 2022.

Kailera burst onto the scene at the start of Q4 with a $400m series A round to fund its pipeline of obesity medicines, including four drugs licensed from Hengrui – the GLP-1/GIP dual agonist HRS9531 (KAI-9531), the oral GLP-1 agonist KAI-7535, an oral tablet formulation of KAI-9531 and the preclinical GLP-1/GIP/glucagon receptor agonist KAI-4729. Kailera and Hengrui reported positive Phase II data for KAI-9531 earlier this month.

The team behind Karuna Therapeutics – the developer of the newly approved schizophrenia drug Cobenfy (xanomeline and trospium chloride), which Bristol Myers Squibb acquired for $14bn – launched Seaport Therapeutics with $225m in series A funding in October. Seaport will use its initial funding to initiate a Phase IIb clinical trial for lead drug candidate SPT-300 in major depressive disorder and begin clinical development of SPT-320 for generalized anxiety disorder.

Metsera raised $215m in series B financing in November after it closed a $290m series A round in April, bringing its 2024 venture capital haul to $505m. The proceeds will fund a Phase II trial of the once-monthly injectable GLP-1 receptor agonist MET-097i that the company initiated late last year as well as ongoing Phase I trials of MET-233i, an ultra long-acting injectable amylin analog, and MET-002, an oral GLP-1 receptor agonist.

In the targeted cancer drug space, Alentis Therapeutics raised $181.4m in

November to fund its pipeline of Claudin-1 positive (CLDN1+) antibodies and antibody-drug conjugates. The Swiss firm’s series D round also will support its CLDN1+ ADC program for fibrotic diseases.

For more on what 2025 will hold for pharma, check out our 2025 Preview Report.