Modest Final Quarter Completes Shaky Biotech IPO Comeback For 2024

Septerna is the best performer of newly launched firms from Q4, with more initial public offerings fueled by potential interest rate cuts hoped for in 2025.

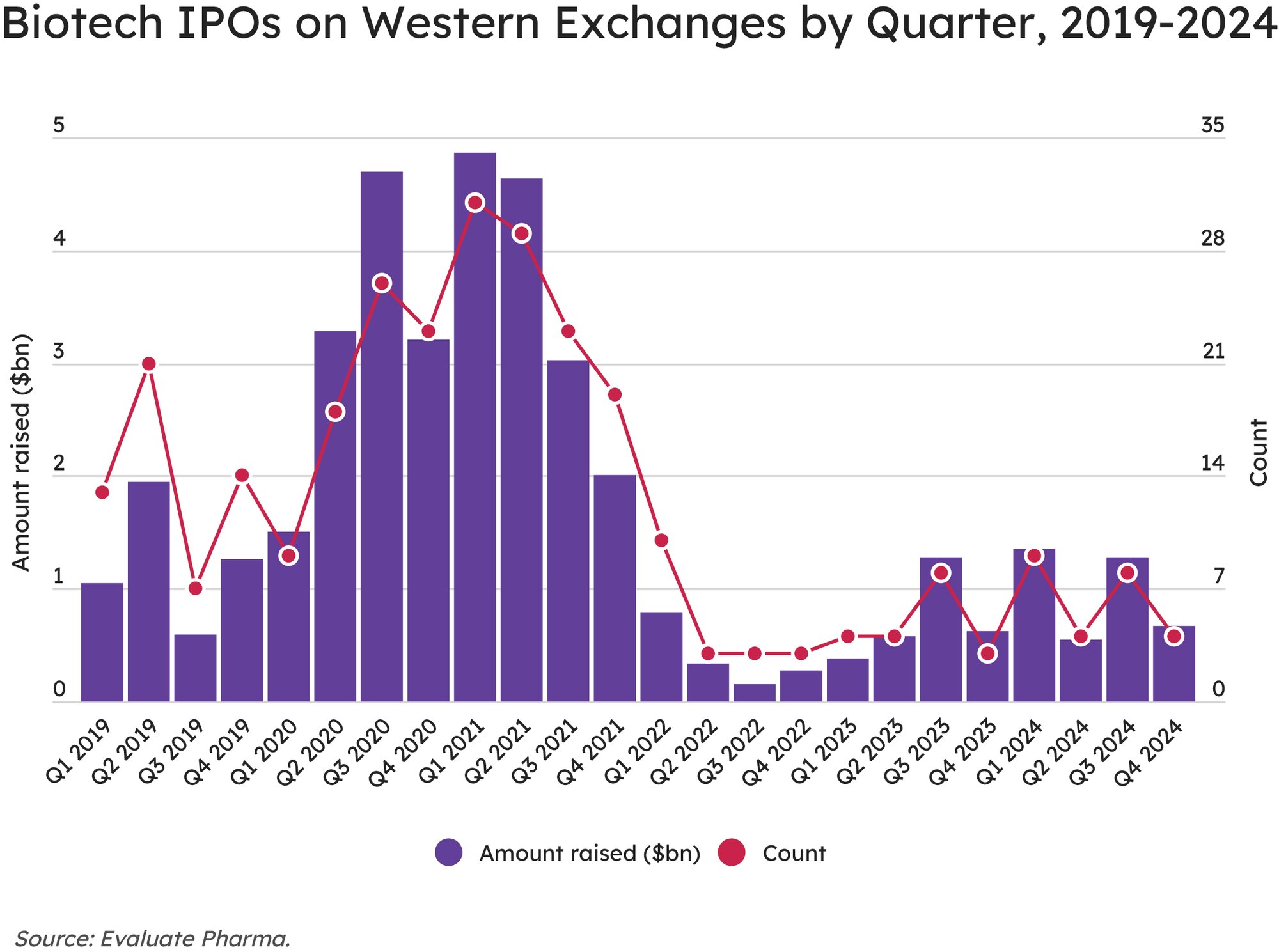

Biotech IPOs staged a moderate recovery in 2024 but a muted end to the year showed how fragile the market remains for companies looking to launch.

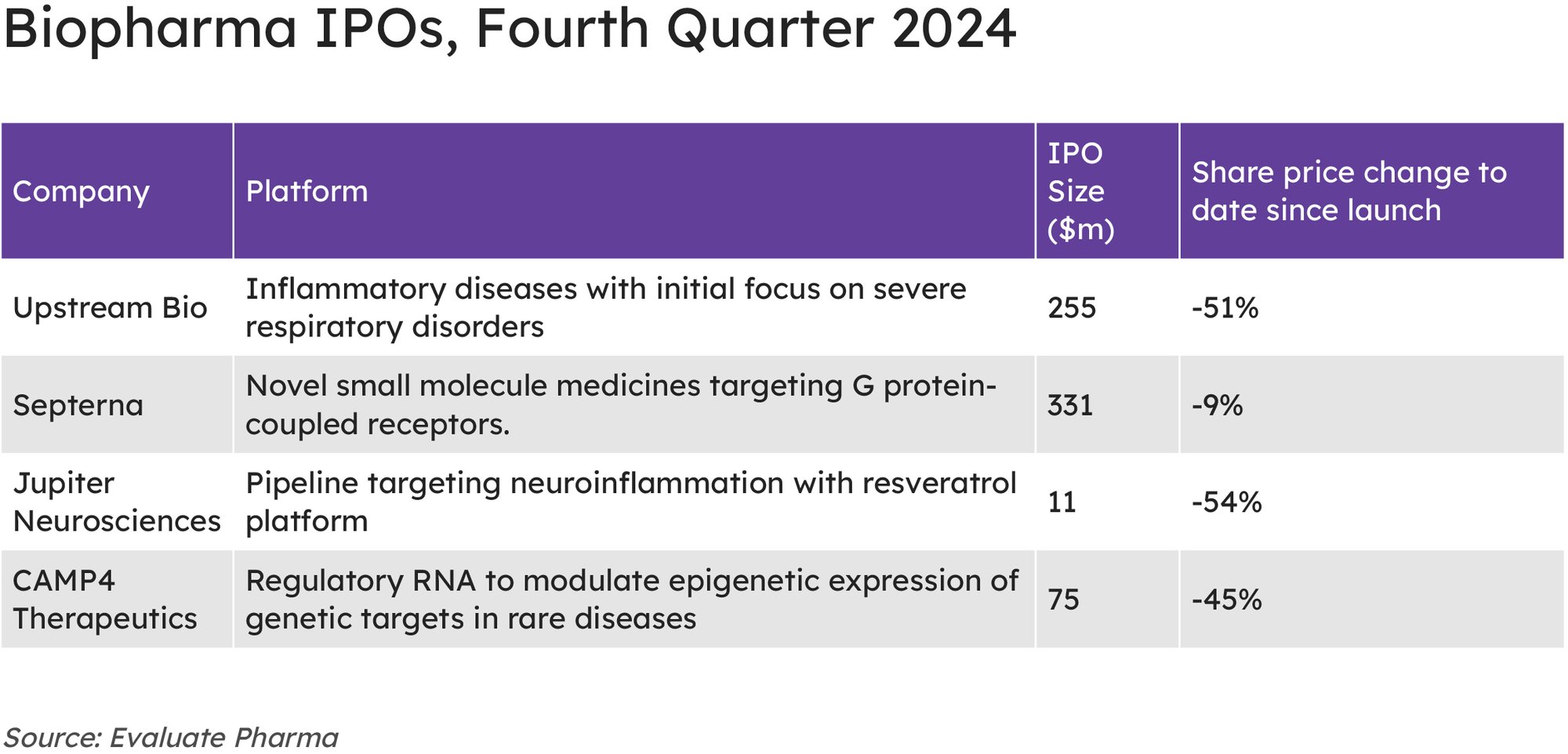

Full year data shows 26 companies debuted on US exchanges last year, higher than the 21 achieved in 2023 and 22 in 2022, when a pandemic-fueled boom in biotech flotations abruptly ended. However the market is no surefire route for new biotechs looking to accelerate their business plans and the final quarter of 2024 saw just four companies complete an IPO, raising a total of $670m.

Lukewarm investor sentiment for the whole sector is undermining performance for post-IPO biotechs, with many launched in the last few years trading well below their launch values. This applies to the most recent additions, with three of the four launched in the final quarter – Upstream Bio, Jupiter Neurosciences and CAMP4 Therapeutics – currently trading at a 50% discount to their launch prices. (see table).

There is a considerable backlog of private biotech companies looking to launch IPOs.

Standing out from this cohort is Septerna, which raised the most capital ($331m) and its share price ($19.30 on 23 January) is only 9% lower than its late October launch price. The South San Francisco, CA-based company is developing next generation oral small molecule GPCR therapies and its lead candidate is SEP-786, a PTH receptor agonist for hypoparathyroidism. Currently in a Phase I study, the company is expecting to share initial results by mid-2025.

Research by analysts at Jefferies shows there is a considerable backlog of private biotech companies looking to launch IPOs, with many awaiting more favorable macro-economic and biotech market conditions.

Chief among the macro factors is the US interest rate, and the Federal Reserve has indicated that it may continue to cut the rate in 2025, as long as inflation remains under control and down from its 2022 peak.

In December, the US central bank lowered its policy rate to a 4.25%-4.50% range, with expectations of two further rate cuts this year, with the first potentially arriving in March.

The new Trump administration has promised a broad and wide-ranging set of policy changes, the impact of which remains hard to read. These will include macro-economic policies such as tariffs on certain imports and at the sector level, efforts to shake up regulation, including the likely appointment of pharma industry skeptic Robert F. Kennedy Jnr at the Department of Health and Human Services.

Lackluster interest in small-to-medium biotech was demonstrated by the overall flat performance of the sector-specific XBI exchange in 2024, which showed virtually no growth over the 12 months. This was in contrast to a continuing boom in tech company stocks, which helped raise the Dow Jones by 16% last year.

There is some optimism about a bounceback in the biotech sector in 2025.

Nevertheless, there is some optimism about a bounceback in the biotech sector in 2025, with the hoped for interest rate cuts potentially combining with higher M&A activity to stimulate the sector.

On the IPO front, four companies have already declared their intention to float in early 2025: cystic fibrosis-focused Sionna, autoimmune and inflammatory conditions company Odyssey, precision medicines firm Maze Therapeutics and obesity specialists Metsera.