M&A Values Continued To Decline During Q4 2024

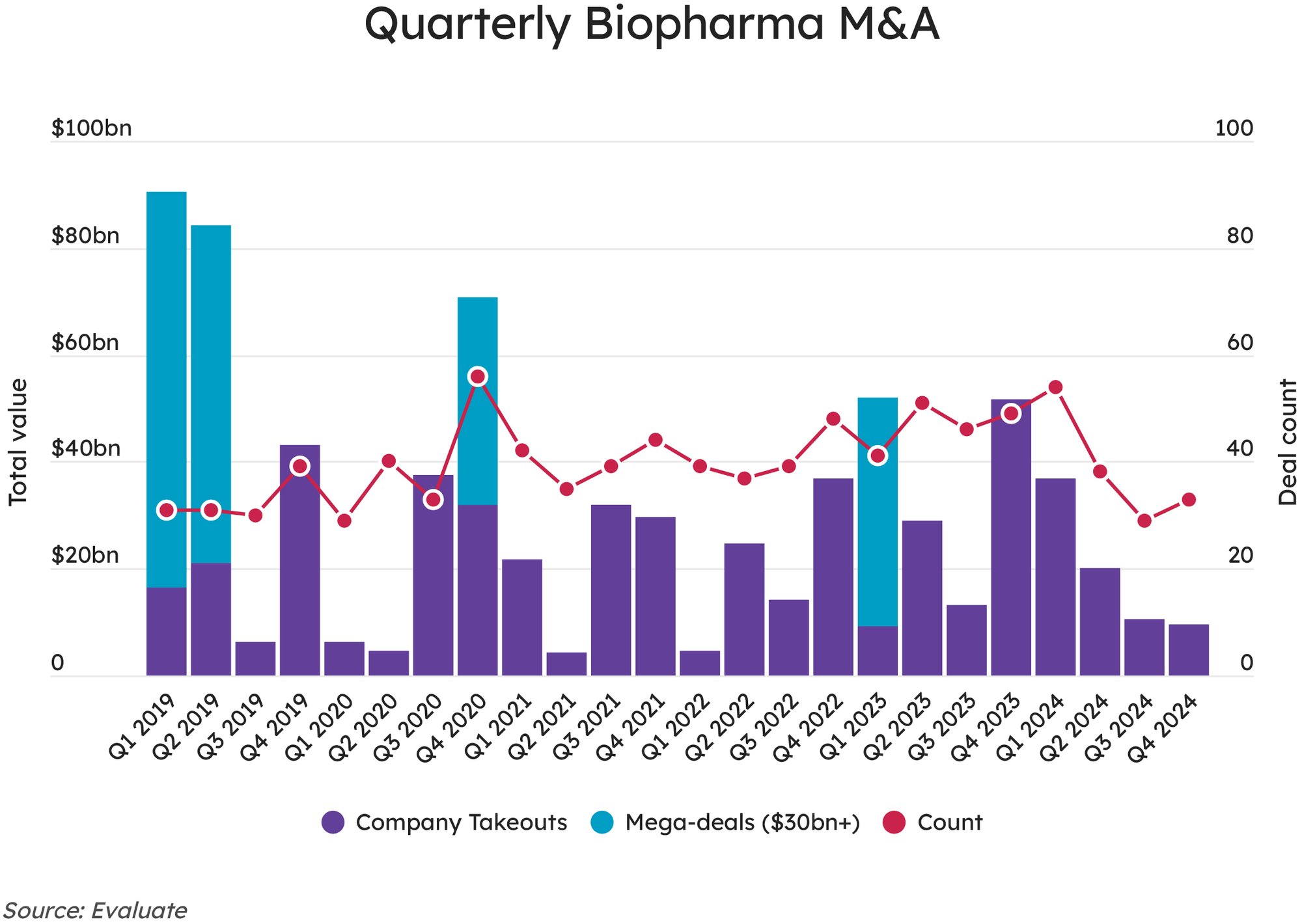

Evaluate data show that the biopharma industry made $9.5bn of acquisitions during the fourth quarter, a third consecutive quarter of decline, although deal volume rose to 33 from Q3’s 29.

Although 2024 got off to a promising start with a busy first quarter, the fourth quarter marked the third consecutive quarter of declining biopharma merger-and-acquisition valuation. Evaluate reported that there were 33 M&A deals during Q4, up from 29 in the third quarter, but with a total valuation of slightly more than $9.5bn, down substantially from nearly $52.3bn in Q4 2023.

Industry watchers were ready with their explanations of why M&A activity had cratered throughout 2024 when positive conditions appeared in place for such activity – while potential buyers had both cash and need to add pipeline assets to offset coming revenue losses due to patent expirations, macroeconomic uncertainty, especially in the financial markets, and the looming presidential election held down activity as deep-pocketed players awaited a better environment for placing higher-priced bets.

Biopharma M&A is expected to rebound in 2025 and the year got off to a hot start when Johnson & Johnson agreed to buy Intra-Cellular for $14.6bn on 13 January, nearly tripling the price tag of the largest takeout recorded during 2024, Vertex’s $4.9bn purchase of Alpine Immune in April.

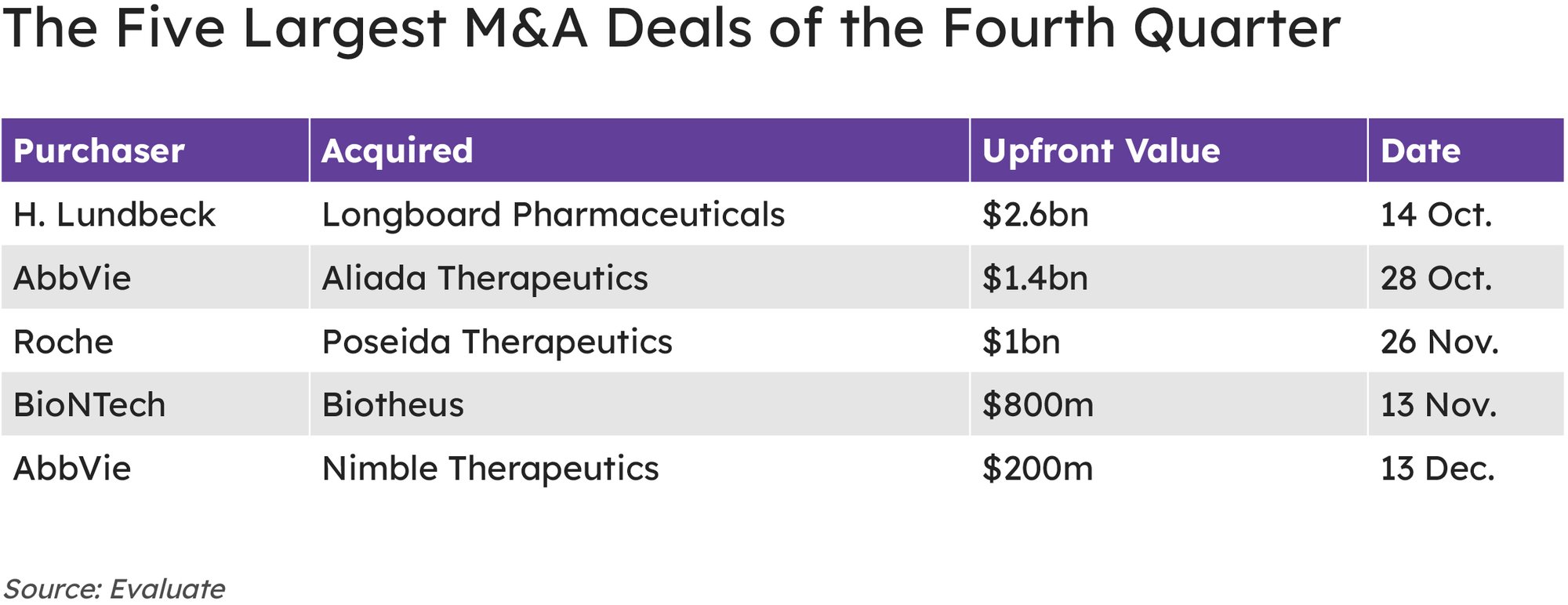

The biopharma sector did not even approach a purchase of that size during Q4, as H. Lundbeck’s $2.6bn acquisition of Longboard Pharmaceuticals ended up the highest-valued deal announced in the final three months of 2024. It was one of just three acquisitions valued at $1bn or higher during Q4.

The first quarter of 2024 proved an outlier, as the industry made 54 M&A transactions with a total valuation of nearly $37bn. That valuation nearly equaled the slightly less than $40bn in acquisitions recorded over the final nine months of 2024, but Novo Holdings’ $16.5bn acquisition of Catalent – a manufacturing-driven deal expected to benefit Novo Nordisk by addressing its supply issues for semaglutide-containing products such as Ozempic and Wegovy – skewed the Q1 dollar total. The transaction was biopharmaceutical-adjacent, but not strictly a pure-play biopharma deal.

The biopharma sector did not approach the Q1 deal volume or valuation totals during the remainder of 2024, although a relatively healthy 38 takeouts valued at slightly more than $20bn were recorded during the second quarter. In Q3, a clear decline in M&A activity was evident – while there were 29 M&A transactions, total value only reached $10.5bn.

Biopharma M&A is expected to rebound in 2025.

The fourth quarter of 2024 reversed a trend seen in the prior two years, when M&A activity surged during the final three months of the year.

The fourth quarter of 2024 reversed a trend seen in the prior two years, when M&A activity surged during the final three months of the year. In Q4 2023, the biopharma sector made 49 M&A deals valued at more than $52bn, highlighted by a pair of $10bn-plus takeouts, and in 2022, the final quarter’s totals of 48 acquisitions valued at more than $37bn made for the busiest quarter of that year.

Denmark-headquartered Lundbeck made the largest deal of the fourth quarter, agreeing to pay $2.6bn on 14 October to acquire La Jolla, CA-based Longboard, mainly to get its hands on bexicaserin, a next-generation 5-HT2C receptor agonist that is being studied in seizure disorders such as Dravet syndrome (DS), Lennox-Gastaut syndrome (LGS) and other developmental and epileptic encephalopathies (DEEs).

Last September, the candidate entered a Phase III study in Dravet syndrome, an indication it has breakthrough therapy designation for from the US Food and Drug Administration. According to Evaluate Pharma, the drug is on track to launch in late 2028, with a peak revenue projection of $850m in 2030. Lundbeck closed the deal on 2 December, paying $60 per share for the biotech, a 70% premium to Longboard’s 10-day average share price before the deal was announced.

The quarter’s second-largest deal was AbbVie’s $1.4bn buyout of Aliada Therapeutics on 28 October, bringing the North Chicago firm ALIA-1758, a Phase I bispecific antibody candidate for Alzheimer’s disease that targets pyroglutamate amyloid beta (3pE-Aβ), the same target as Lilly’s Kisunla (donanemab), but with potentially better targeting and other advantages. The transaction closed on 11 December.

AbbVie also made the fifth-largest acquisition of Q4, paying $200m on 13 December to acquire Wisconsin-headquartered Nimble Therapeutics, a 2019 spinout from Roche, with a specialized technology to chemically synthesize scaffolded natural and modified macrocyclic peptidomimetics – from a library of photoprotected amino acids – for multiple therapeutic areas. The deal, which includes the potential of earnouts to Nimble shareholders, brought AbbVie the biotech’s platform technology as well as its lead candidate, an oral peptide IL23R inhibitor in preclinical development for psoriasis.

Roche added to its cancer pipeline on 26 November by paying $1bn up front, with up to $500m in earnouts possible, for cell therapy specialist Poseida. The two companies had been partnered since 2019 on developing off-the-shelf chimeric antigen receptor T-cell (CAR-T) therapies, with an initial focus on multiple myeloma. Still not closed, the deal was structured so that shareholders in the San Diego biotech get $9 per share up front and potential to realize up to $4 per share in milestone payments.

Germany’s BioNTech agreed on 13 November to acquire Biotheus, a developer of bispecific antibodies, for $800m up front plus up to $150m in earnouts. BioNTech had licensed the Chinese firm’s BNT327 (also PM8002), one of the most advanced PD-(L)1 x VEGF-A bispecific candidates, in July 2023.

BNT327 itself is yet to enter Phase III, but BioNTech said during a Q3 investor presentation that it planned to initiate a Phase II/III NSCLC trial in non-small cell lung cancer and a Phase III trial in small cell lung cancer by the end of 2024, with a Phase III study in triple-negative breast cancer planned for the following year.