Digital Health

Contribution from Galen Growth

The Digital Health ecosystem finds itself at a pivotal juncture, navigating a transition from exaggerated expectations to pragmatic realities following the exuberance in the period running up to and including 2021. This sector, now over a decade old, has burgeoned into a thriving domain of diverse Digital Health ventures, boasting a staggering 10,000+ private entities, each exhibiting varying degrees of innovation and promise.

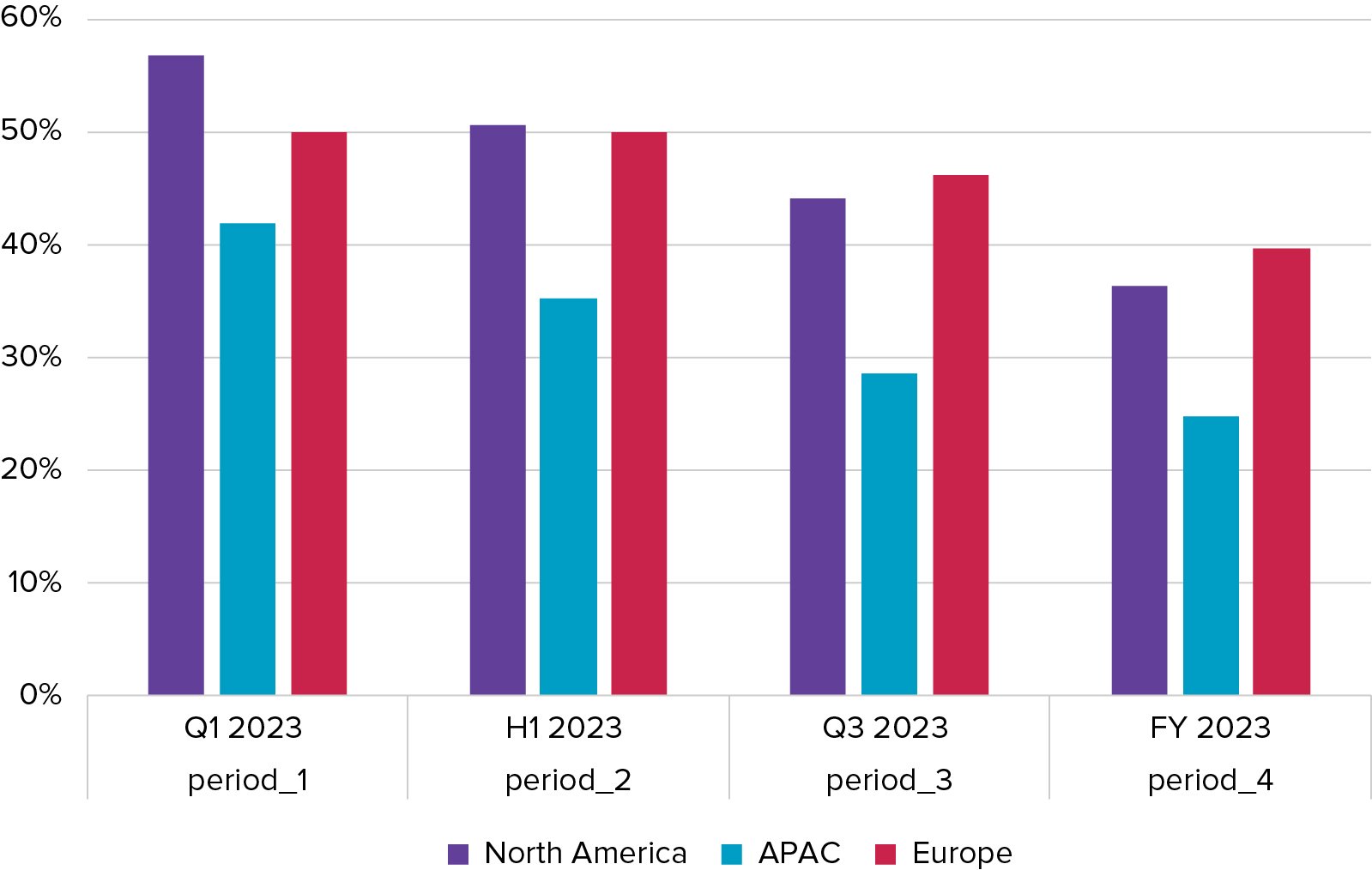

However, this flourishing landscape is presently weathering a challenging funding drought. Recent data reveals that less than 40% of Digital Health ventures managed to secure funding in the past 18 months, marking a significant decline in investor appetite [See chart: Funding Strength].

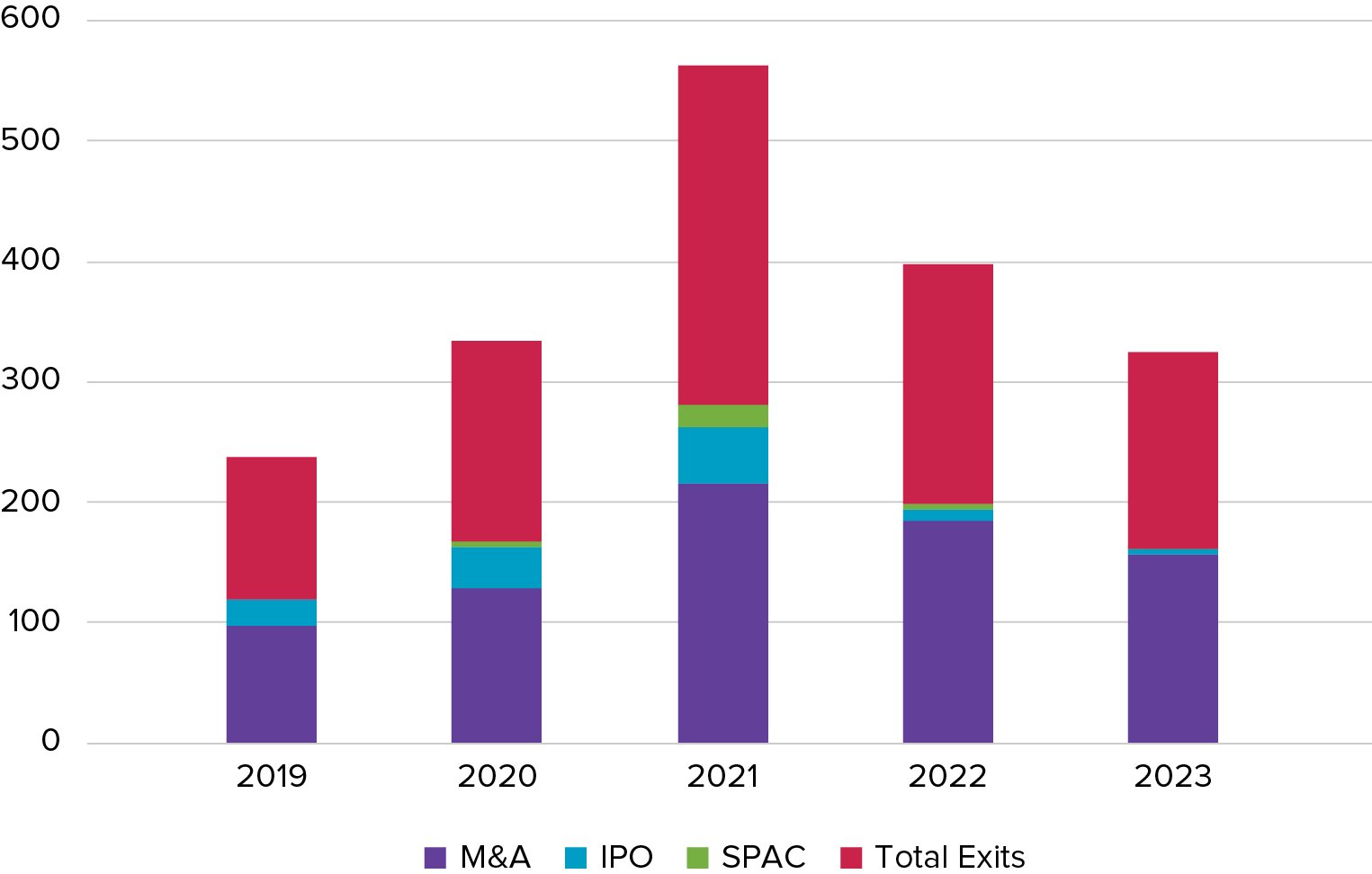

The realm of mergers and acquisitions (M&A) has witnessed a notable deceleration, while initial public offerings (IPOs) and Special Purpose Acquisition Company (SPAC) activities remain scant, especially evident in Europe where the absence of recorded IPOs further underscores the industry's subdued state. [See chart: Global Digital Health Venture Exit History].

The narrative of this evolving sector has been punctuated by high-profile shutdowns, exemplified by Pear Therapeutics (US), Olive.ai (US), and Babylon (UK).

These entities, despite substantial funding and lofty valuations, faltered due to unrealistic growth assumptions, setting a precedent likely to be echoed by similar shutdowns in 2024.

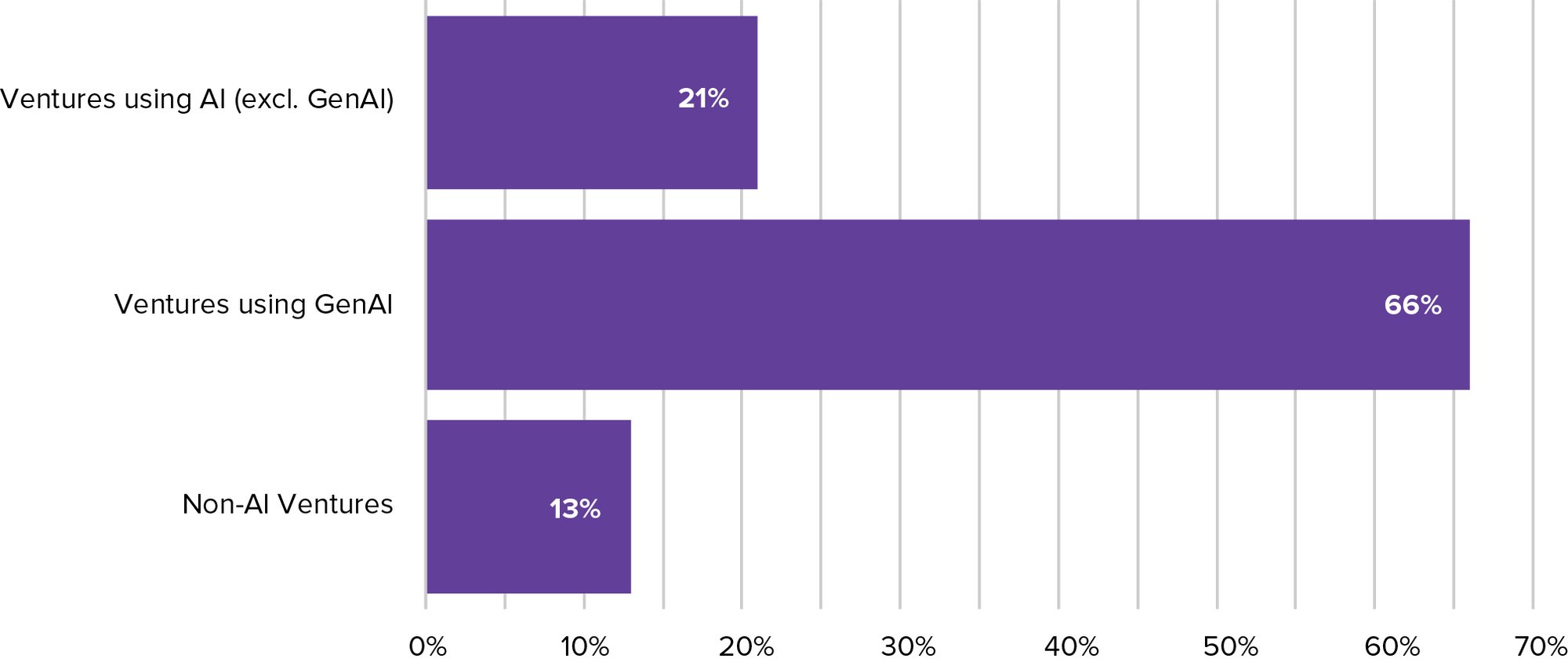

Generative AI aka GenAi also emerged as the focal point for Digital Health in 2023, capturing the collective attention of industry players, investors, innovators, and media alike. Its ascent in sectors, such as biopharma and health systems, demonstrates its dominance as the year's hottest topic in Digital Health innovation. [See chart on next page: Share of Biopharma Digital Health venture partners using AI/Machine Learning and Generative AI]

The pronounced pain points within the healthcare value chain have assumed a pivotal role in shaping priorities and focus within the Digital Health domain. This shift has drawn intensified commitments from pharmaceutical companies, increasingly investing in Digital Health innovation within their research endeavours. Concurrently, health systems are redoubling their efforts in leveraging Digital Health innovation to enhance healthcare delivery, to address their growing capacity and productivity issues.

In summary, the Digital Health ecosystem stands at a critical juncture as it enters 2024, recalibrating its trajectory amid funding challenges, notable setbacks, and a much-needed focused emphasis on addressing core healthcare challenges.

The industry's resilience and adaptability will be tested as it navigates this transition from hype to pragmatic innovation, setting the stage for a dynamic and potentially transformative future.

The pronounced pain points within the healthcare value chain have assumed a pivotal role in shaping priorities and focus within the Digital Health domain.

Percentage of Growth Stage ventures which have raised funding in the last 18 months

Global Digital Health Venture Exit History

Share of Biopharma Digital Health venture partners using AI / Machine Learning and Generative AI

The forecast for the initial half of 2024 in the Digital Health sphere resembles a continuation of the trends witnessed in the preceding year. The landscape remains ensnared within the array of geopolitical uncertainties, with the impending US general election adding a new layer of complexity to the ecosystem's narrative. However, optimism emerges on the horizon as the latter half of the year witnesses a pivotal turning point for the Digital Health sector.

Amidst this landscape of continued volatility, the industry is steadfastly steering towards a trajectory of becoming a faster, better, and more robust ecosystem. Regulations and reimbursement frameworks are gradually taking shape, catalysed by a Health System crisis exacerbated by Healthcare Providers' sluggish adoption of Digital Health innovations. The resultant push from payors to craft Digital Health reimbursement frameworks such as DiGa (Germany) and PECAN (France) stands as a barometer to this evolving paradigm.

Within Digital Health Ventures, the impending expiration of funding runways for many entities looms large, prompting valuations to hit their nadir. Emphasis now squarely rests on forging pathways to profitability, augmenting efforts towards robust proof points such as clinical evidence. The landscape is ripe for continued consolidation, marked by a confluence of M&A activities and business shutdowns. The ideal focus shifts towards constructing Digital Health Platforms that offer value-addition, seamless interoperability, and holistic solutions over disparate point solutions. Biopharma will focus increasingly on Digital Health innovation in drug Research and Development productivity, as it faces a significant patent cliff and pipeline drought. Health Systems will focus on Digital Health innovation to increase capacity and improve productivity, as it faces growing demand, labour shortage and labour costs. The alarming situation in the UK with an NHS waitlist exceeding 8 million people (12% of the population) leading 40+% of UK citizens to self-diagnose as they cannot access healthcare services, is reflective of the status of many other health systems and underscores the urgency for transformative healthcare solutions.

Investors, faced with a constrained value chain characterised by diminished exits and an acute dearth of IPOs, grapple with the challenge of seeking better returns amid a higher cost of capital environment. Valuations, which are finding a bottom, will have a cascading effect on follow-on rounds and multiples on invested capital (MOIC). The venture capital sector, overcrowded due to an influx of new players facilitated by easy access to capital, confronts an inevitable consolidation. This shakeout will however create opportunities, and reshape the landscape, shifting away from short-term, pump-and-exit strategies towards sustainable venture-building approaches.

Despite these multifaceted challenges, 2024 holds promise for discerning investor organisations and forward-thinking entities within the Digital Health sector.

Emphasis now squarely rests on forging pathways to profitability, augmenting efforts towards robust proof points such as clinical evidence.