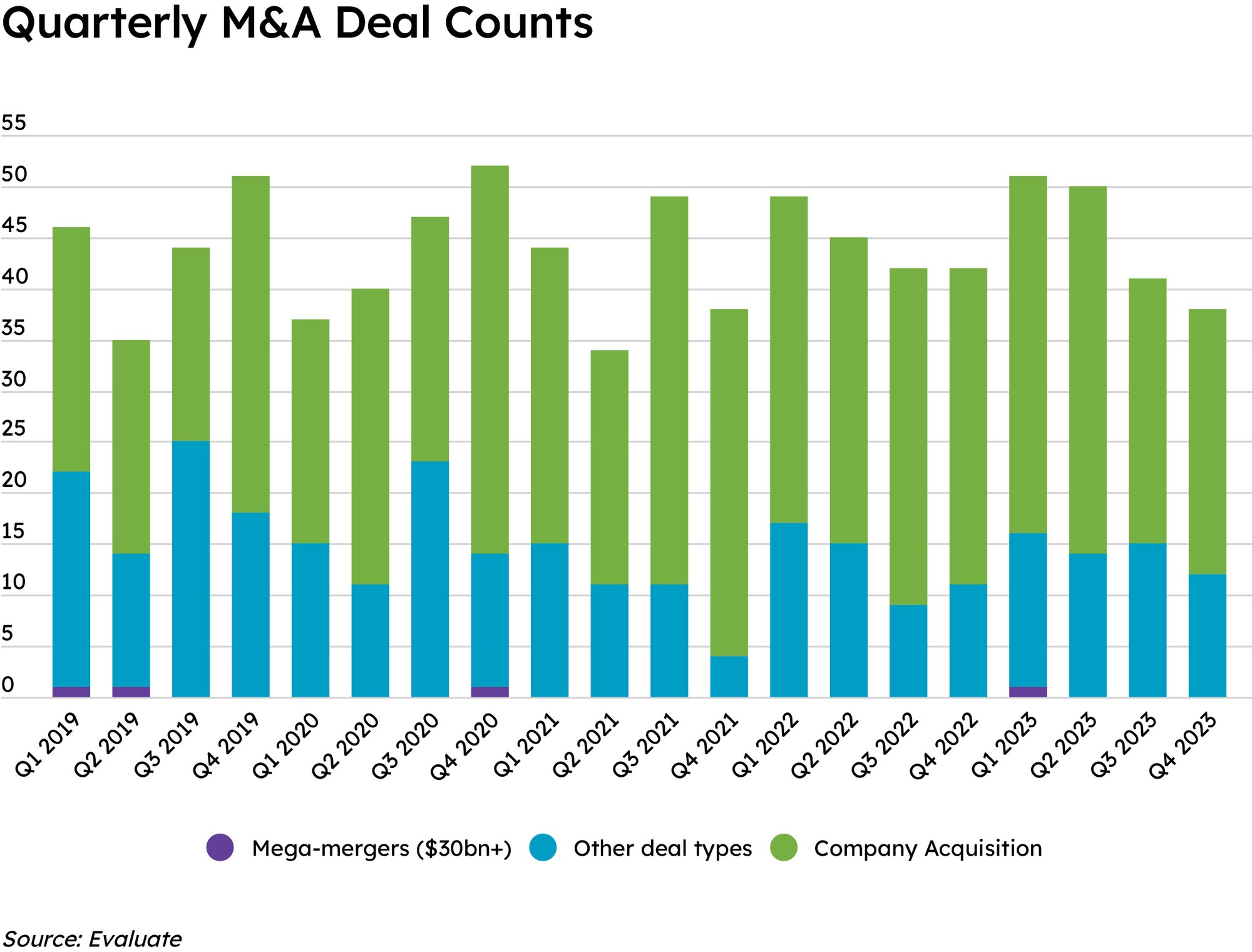

mega-merger. As always, valuation is challenging to assess, because many deal announcements do not provide detailed figures – only 21 of Q4’s 39 included publicly disclosed valuations – and some of the reported valuation information includes milestone payments and sales royalties that may never be realised.

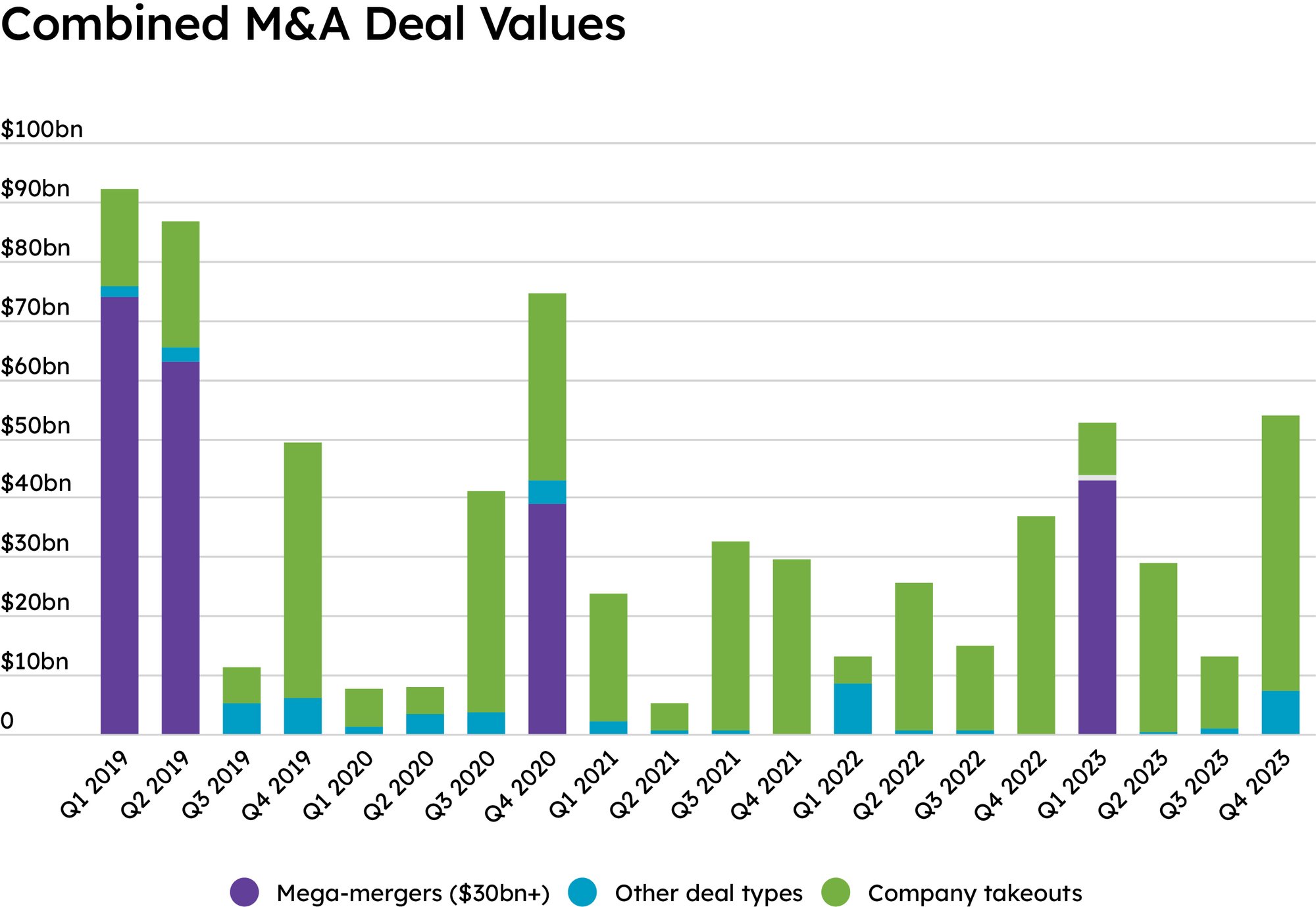

For the quarter, the aggregate value of M&A activity was $58.86bn, up exponentially from the $13.08bn seen in Q3. The Q4 number also doubled the healthy $29bn in aggregate value realised during the second quarter.

2023 M&A Activity Finished With A Bang

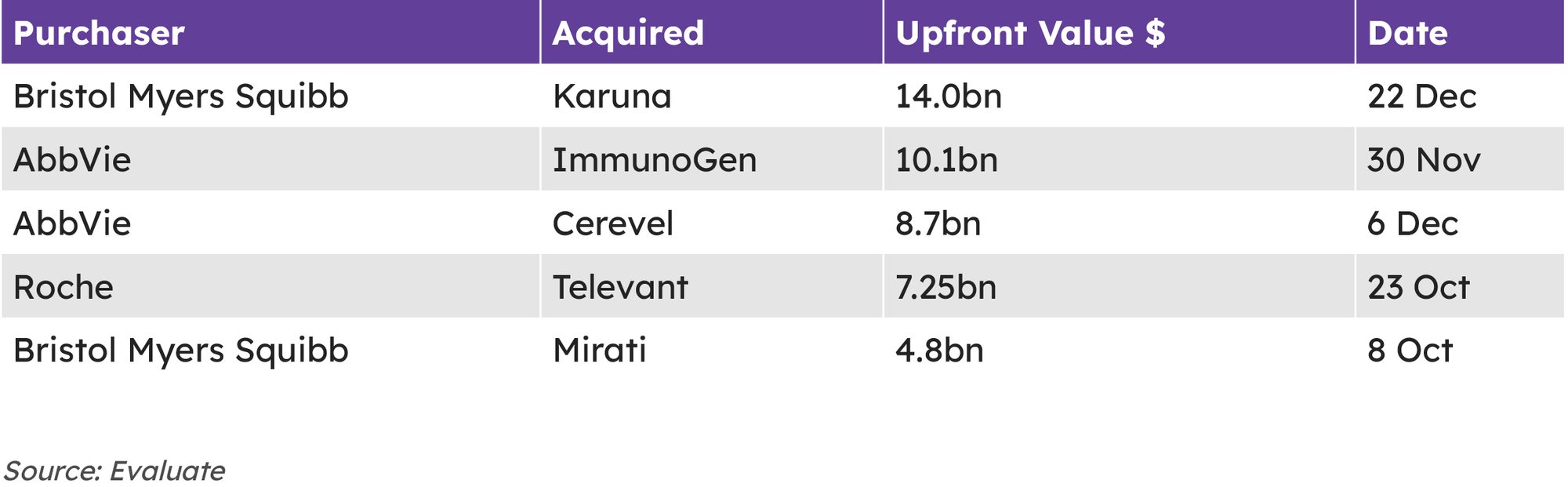

M&A activity picked up as Q4 went on, as December brought 14 transactions, including the largest of the quarter, Bristol Myers Squibb Company’s pre-Christmas splurge of $14bn for Karuna Therapeutics, Inc.. The pharma’s move to expand its neuroscience portfolio, driven by Karuna’s M1/M4 receptor agonist KarXT (xanomeline-trospium), which is under US Food and Drug Administration review for schizophrenia, was the year’s second-largest M&A play, trailing only Pfizer Inc.’s $43bn buyout of Seagen Inc. in March. BMS then closed out the year on 26 December with a $4.1bn bid for the radiopharmaceutical firm RayzeBio, Inc..

Three of 2023’s biggest M&A transactions and two of its $10bn-plus deals occurred toward the end of the year. AbbVie Inc. was quite busy late in the year, paying $10.1bn to acquire ImmunoGen, Inc. and $8.7bn just a week later to pick up Cerevel Therapeutics Holdings, Inc.