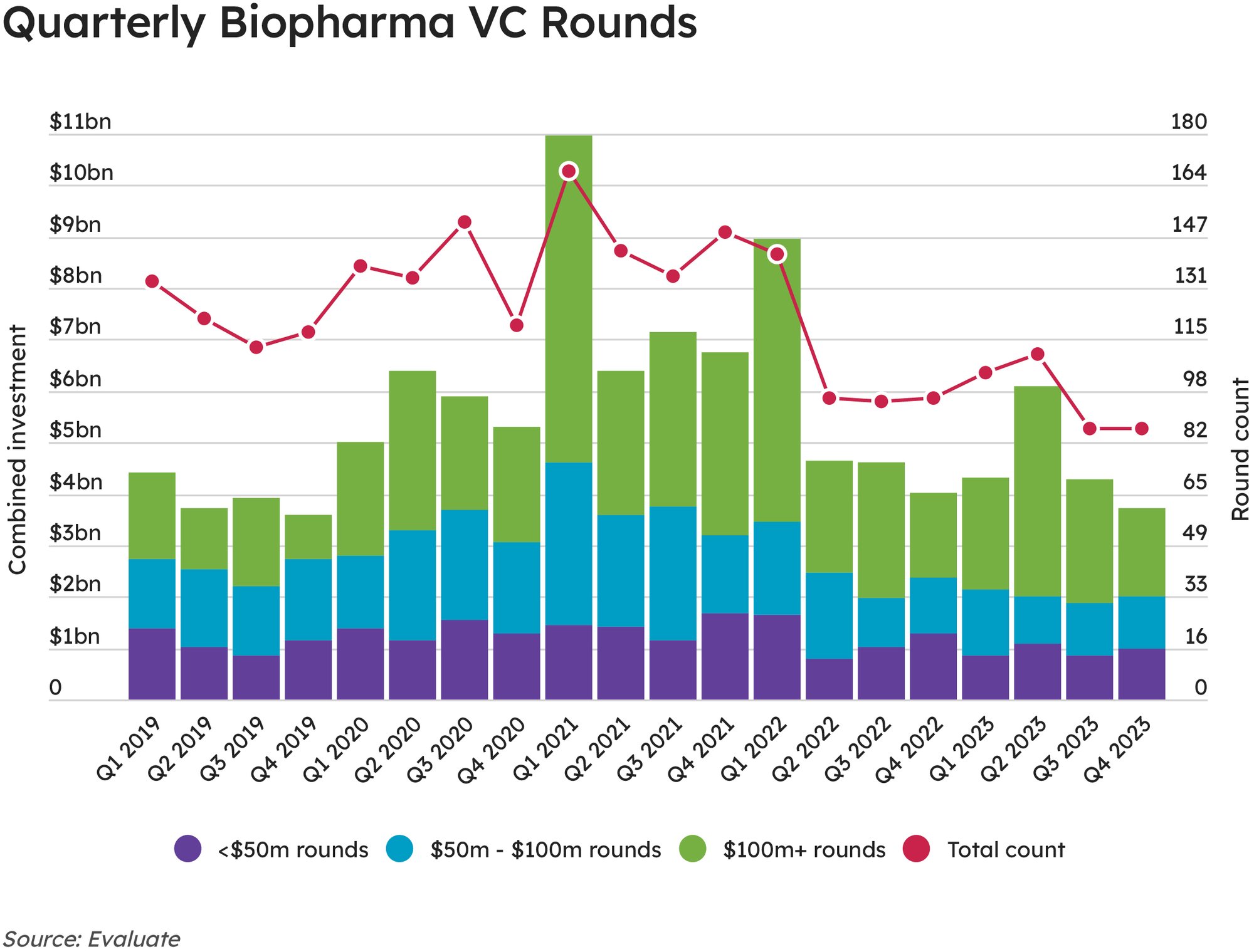

One of the factors impacting venture capital is the ability for drug developers to launch an initial public offering, and such offerings were relatively limited in 2022 and 2023 relative to the record-breaking level seen in 2021. Without that exit option, many VC investors have held off on new investments, choosing to reserve cash for current portfolio companies still waiting for the IPO window to open.

New IPOs have been limited since 2022 because of falling valuations for already public biopharma companies. The Nasdaq Biotechnology Index (NBI) and the closely watched XBI fund are down by more than 6% and 20%, respectively, over the past two years. However, based on a year-end rally due in part to some substantial merger and acquisition activity – the other exit strategy for VC investors – the NBI ended 2023 up 4.1% and the XBI closed out the year with a 7.6% gain.

Bristol Myers Squibb Company agreed to buy Karuna Therapeutics, Inc. for $14bn in late December. Then the big pharma announced its $4.1bn purchase of RayzeBio, Inc. a few days later. This followed similar back-to-back M&A activity by AbbVie Inc. in late November and early December, when it agreed to pay $10.1bn for ImmunoGen, Inc. and $8.7bn for Cerevel Therapeutics Holdings, Inc.

Interest rates are a major factor impacting investment across the board, but the US Federal Reserve has offered some encouragement. After meeting in mid-December, the Federal Open Market Committee forecast that the federal funds rate will drop from a median of 5.4% in 2023 to a median of 4.6% in 2022 with further easing through 2026, as long as inflation continues to rise at a rate of about 2%.

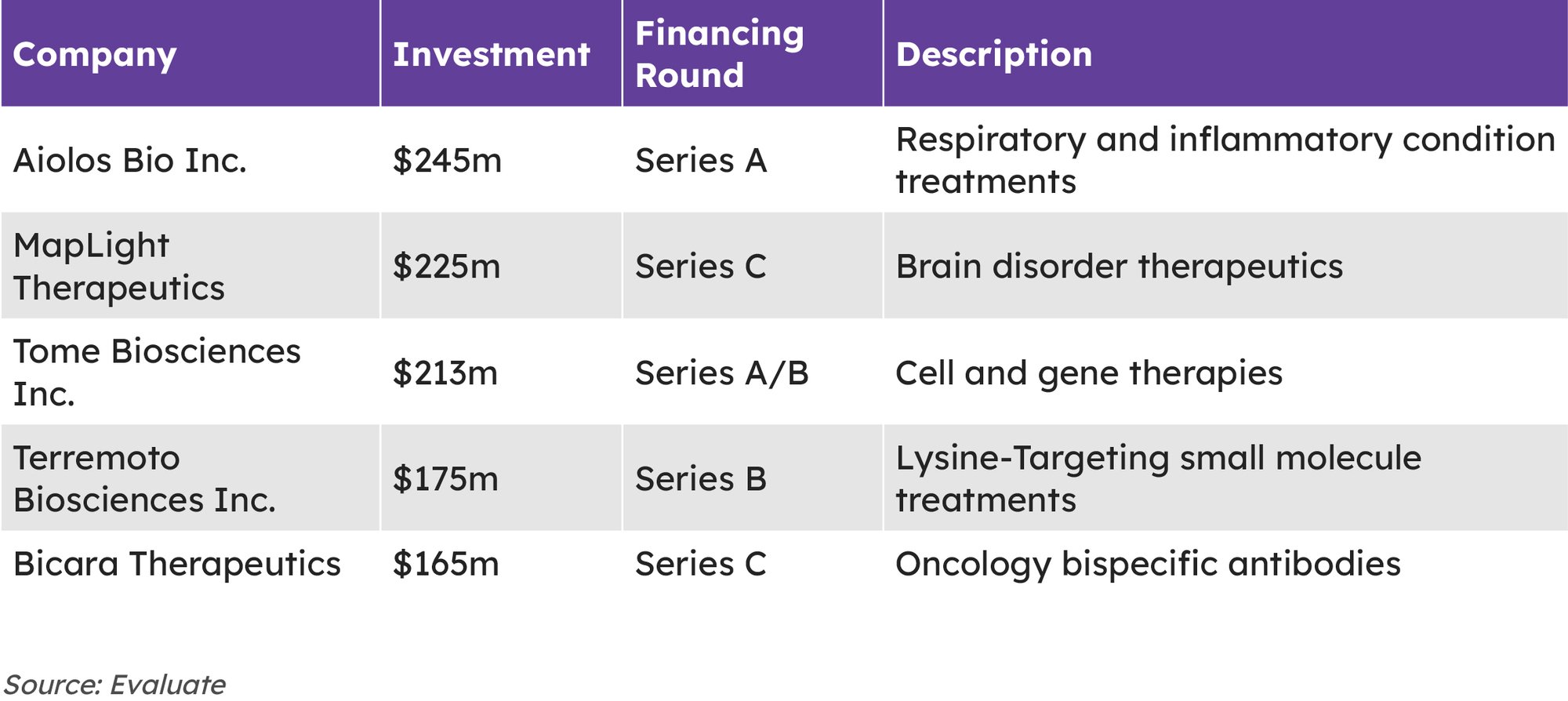

If the pace of M&A continues to be brisk, and if the IPO window opens a little wider